Macro Notes - A New Era for Japanese Equities

December 16, 2025

We’ve never been fans of the Bank of Japan’s ETF buying program.

For those that need a quick refresher, the BoJ began buying equity ETFs (that tracked the domestic equity market) back in 2010. These purchases were expanded in 2013 and passively run until the program was halted in March 2024.

At the time, there were three reasons why the BoJ initiated/expanded these purchases:

- To prevent “excessive” declines in domestic equities (their words, not mine).

- To increase household confidence and stimulate consumption to combat deflation.

- Interest rates were already at zero (and slightly negative). Further purchases of Japanese government bonds (JGBs) would have done little, and ETF purchases were seen as the next lever.

However, things got complicated once conditions in the Japanese economy improved by enough such that inflation began shifting above target. The Bank of Japan had to start normalizing policy – which meant rate hikes and reducing the size of its balance sheet.

But unlike the bond purchases, ETFs don’t passively roll off the balance sheet. That means that the BoJ has to actively sell its ETF holdings(!) – and in September it announced that this process was going to begin (likely in January).

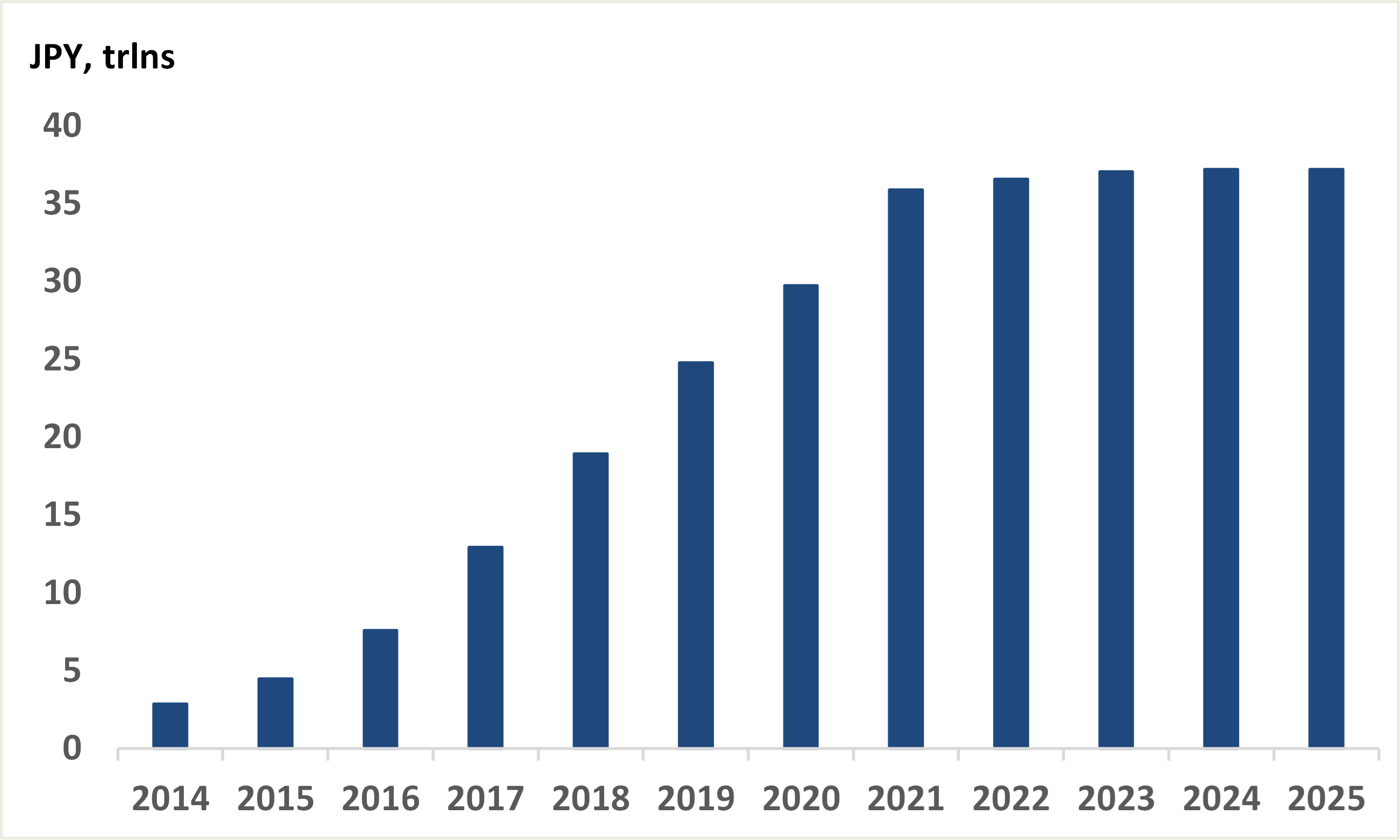

We cannot stress how important a distinction it is between a central bank letting a bond mature and actively selling an ETF. The latter carries a far stronger bearish signal for markets to internalize. Compounding the issue is the size of the BoJ’s footprint in the domestic equity market. As of end-September, the BoJ’s ETF portfolio had a market value of JPY83trln (or US$534bln). That means that the BoJ is the single largest holder of Japanese equities with about 7% of the total market cap.

It’s estimated that it’ll take the BoJ well over 100 years to completely divest itself of ETFs. But even small annual sales from the largest equity buyer could easily lead to increased chop as investors grapple with the new reality.

Two takeaways here:

- All told, this is a new era for Japanese equities that could mean a valuation reset and higher equity risk premiums.

- This is why we’re eschewing Japan-specific ideas and focusing on broader EAFE (via ZEA).

Chart – Book Value of BoJ Equity ETF Holdings Over Time