Macro Notes - AI and Productivity

February 17, 2026

We need to talk about AI’s connection to productivity - and what it means for markets. There is growing confusion around whether a 3%+ US growth backdrop is unequivocally bullish, particularly if that growth is driven by concentrated capital expenditure in AI.

Let’s be clear:

- AI will raise the productivity profile for the US economy.

- However, the gains are unlikely to be broadly distributed.

- Instead, there is a very good chance that productivity benefits will accrue to a narrow set of market participants, reinforcing dispersion and exacerbating the current ‘k-shaped’ economy.

Do not take my word for it – just look at the way that markets are behaving.

i.) Despite strong earnings momentum, both the technology and communication services sectors are down year-to-date. Positive capex news appears fully priced, and there is palpable concern around whether AI will disrupt legacy software models.

ii.) That same dynamic also helps to explain the bid in US duration of late. The concentration of growth combined with distributional anxiety dampens broad risk appetite.

The first estimate for US Q4 GDP is due on Friday, and much like the rest of the street, we are expecting a strong number. However, if growth is primarily capex-led and AI concentrated, it reinforces our view that we’re deep into late-cycle phase – which we have called a “fractured expansion.”

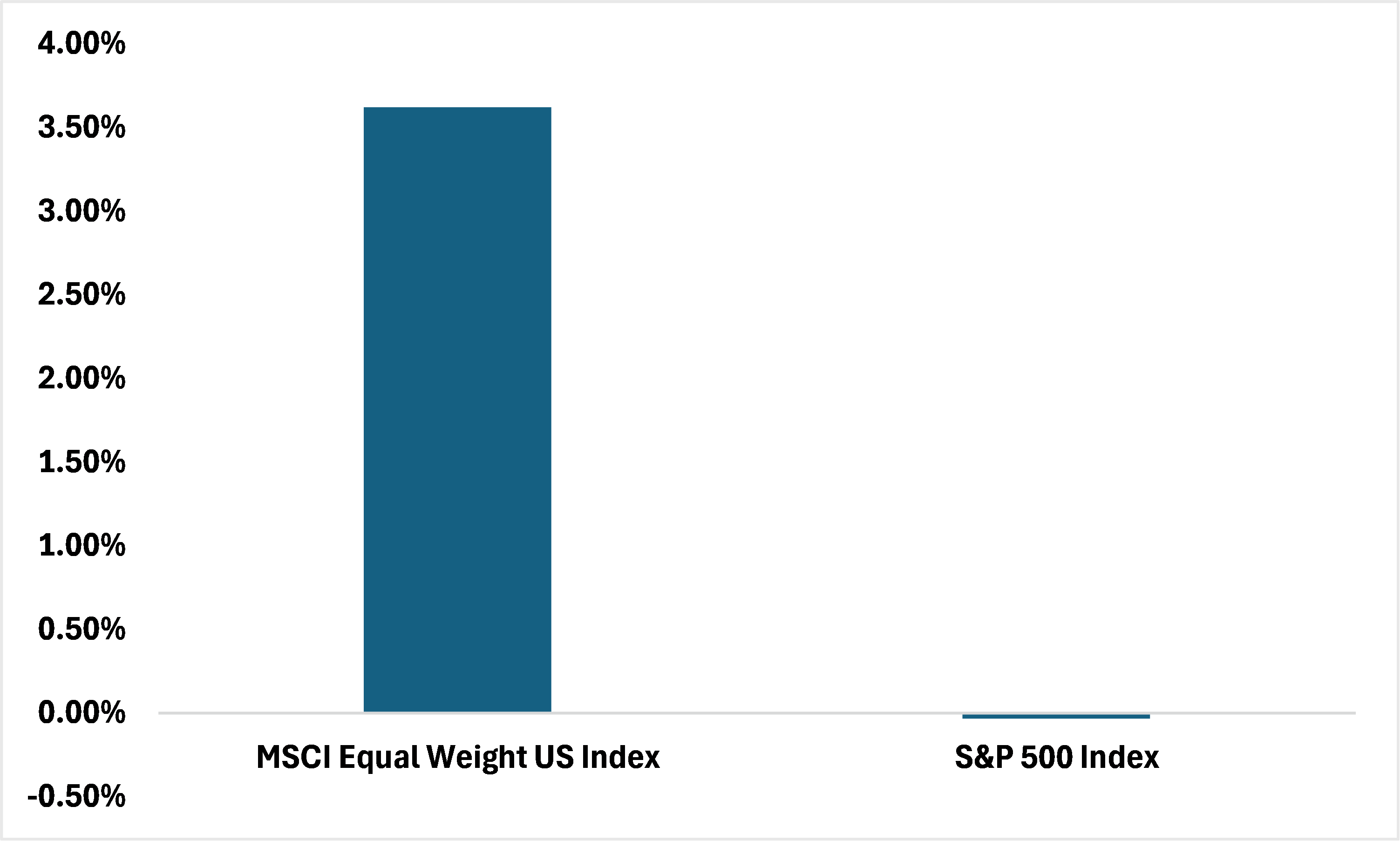

The time to layer back into technology and communications services will come – but not without some measure of multiples disinflation first. For now, we continue to be long US quality (via ZUQ) and prefer equal-weight gauges over market-cap (ZEQL > ZSP).

Chart 1 – Year-to-Date Returns