Macro Notes - Higher Yields could be a Problem for P/E Multiples

December 19, 2025

*Before we begin, this will be our last edition of ‘Macro Notes’ for this year. We’d like to thank our readers for allowing us to be a part of their investment process this year, and we wish everyone happy holidays. Macro Notes will return in mid-January and the Weekly Basis Points will be back on January 12th*

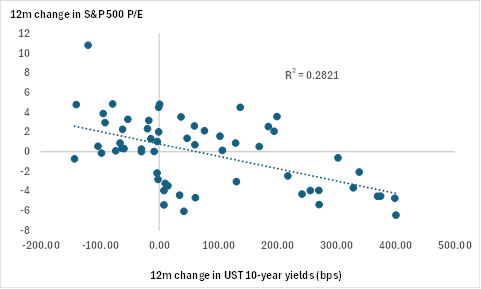

Into next year, we’re optimistic when it comes to broad risk assets. However, we’ll concede that this view is complicated by potential weakness in the long end of the curve. Put simply, an increase in long end US yields could be a headwind for S&P 500 multiples (price-to-earnings, in particular).

Over the past several years, there has been a noticeable inverse relationship between the change in P/E and 10-year yields (see chart below). Why has this inverse relationship held? That’s because during periods of low yields (in 2020 and 2021), investors tend to move further out the risk spectrum. Conversely, when yields are rising, investors tend to be a bit more cautious about equity market valuations.

What this means is that higher long-end yields will put much more onus on earnings resilience to drive S&P 500 returns in 2026. And to be sure, that is what we are banking on for our call next year.

Chart – Changes in Long-End Yields Matter for Equity Multiples