Macro Notes - Is Gold Failing the Safe Haven Test

March 12, 2026

Before we begin, starting today, we will be hosting a live macro and positioning Q&A for advisors. Tues – Thurs, 4:00 – 4:30 p.m. ET. Please click on the following link if you’d like to join. Add to calendar.

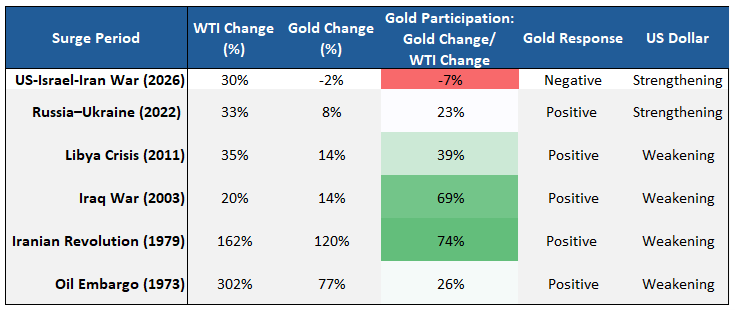

Gold has historically served as a defensive asset during prior geopolitical crises. However, in the current conflict, we haven’t seen that same behaviour. Despite a sharp surge in oil prices (30%), gold has fallen roughly 2% since the conflict began (as of yesterday) – an outlier when compared to other oil shocks in recent decades (Table 1).

A few possible reasons why include:

- Near-term exhaustion. Spot prices are already up 20% on a year-to-date basis after rising by over 60% in 2025. Suffice to say that longs are already quite extended.

- Cross-asset positioning. Investors have been keen to close out USD shorts and UST longs further out the curve. Both work against extending spot gold moving higher in the immediate term.

Do we think this lasts? Probably not.

If inflation risks are to the upside from here, then the utility of holding gold as a diversification tool in portfolios should increase. The reason being - higher inflation regimes usually correspond to an uptick in the correlation between broad equity indices and bonds. Bonds are a poor diversification instrument during those periods.

Additionally, the geopolitical risk premium should continue to benefit broad commodities – especially gold. As a neutral ‘non-sovereign’ reserve asset, the central bank bid isn’t likely to recede anytime soon.

Finally, falling real interest rates will increase the allure of a non-yielding inflation hedge like gold over time.

We expect dips in gold to be well supported from here. Only a break below $4800/oz would lead us to consider a change in that view.

Table 1: Gold vs Oil Dynamics in Geopolitical Crises