Macro Notes - The Market is Net Short the Loonie

December 18, 2025

Attempting to forecast the FX market is an exercise in understanding three things:

(i) What the relevant factors are,

(ii) How those factors relate to the dependent variable (the exchange rate),

(iii) How those factors shift over time

For those of you that remember your Stats 101 classes – it’s a multivariate regression, only the relationships between the independent variables and the dependent variable aren’t stable. Indeed, this is what makes the FX market notoriously difficult to call.

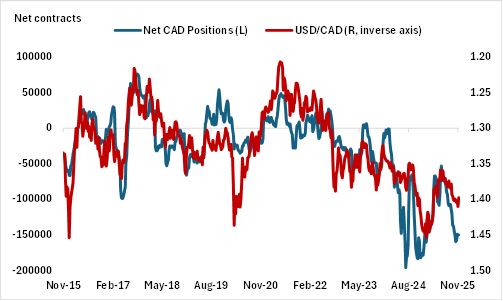

Over the years, one of the more important predictive factors we’ve found is the net length of speculative positioning in the FX futures market. Particularly for non-commercial traders in the CAD market (i.e – those that aren’t hedging for trade/business purposes). We’ve often found that when net positions reach extremes, it becomes an effective contrarian indicator (see Chart 1).

We’ll acknowledge the obvious – that the FX futures market is incredibly small compared to the ‘over the counter’ FX spot, swaps, and options markets. But a major problem is that it’s nigh impossible to generate up-to-date positioning info from the OTC markets. We have to use positioning in the futures market as a proxy. Luckily for us, when positioning gets to extreme levels, it tends to be consistent across the different FX trading instruments (futures, swaps, spot and options). This is particularly true for USD/CAD.

Following the reopening of the US government, the CFTC is back to reporting net positioning. And the latest snapshot we have (as of December 2nd) shows that the market was net short CAD with the length close to extremes. This means that the risks are skewed to an outperforming CAD relative to the USD (or downside in USD/CAD). When taken with other factors (namely, that the BoC is likely done easing, while the Fed may need to be priced for more), there is a strong case to be made for investors in Canada to be hedging their US exposure in the coming months.

However, remember that FX is a fickle beast. Investors are not rewarded for keeping currency risks on the books for extended periods of time. Our preference is to always treat FX hedging tactically for that reason. That means reassessing your hedge/unhedged positions every three months.

Chart – Net Futures Positions Tend to be a Decent Contrarian Indicator for USD/CAD

Source: CFTC, BMO GAM