Macro Notes - The “Takaichi Trade” and the Soft JPY Bias

January 20, 2026

In Japan, the “Takaichi trade” is built on a simple premise: a decisive lower‑house win for the incumbent PM (Sanae Takaichi) and her party (the Liberal Democratic Party of Japan) will mean pro-growth, pro-stimulus economic policies that would unlock larger fiscal packages. However, that might complicate matters for the Bank of Japan (BoJ) and continue to reinforce a weaker JPY trend. At its core, this is a story of fiscal dominance rather than political optimism.

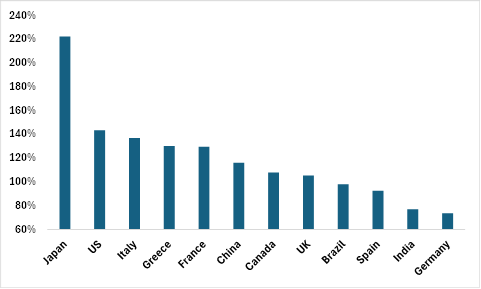

A key anchor of this view is the expectation that the BoJ will remain cautious under PM Takaichi. Her agenda prioritizes deficit-financed spending to support defense and industrial policy. With public debt already elevated, and fiscal issuance likely to rise, aggressive BoJ tightening risks higher debt-servicing costs and renewing JGB volatility. As a result, even with inflation firm, we expect that normalization is likely to be slow and conditional - implying greater scope for a weaker currency.

With USD/JPY pushing towards 160.00 (multi-year highs), authorities have stepped up threats to intervene. Markets continue to interpret these comments as attempts to smooth volatility rather than alter direction (or ‘jawboning’).

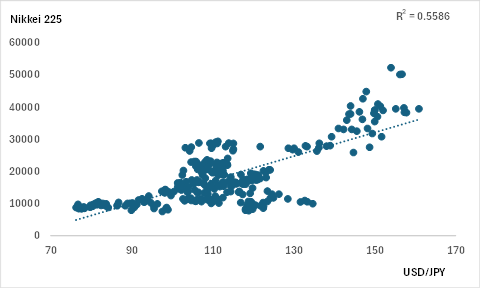

At the same time, Japanese equities have strengthened as the JPY has softened. Over the long-term, we know this relationship is important given the heavy focus of a lot of Japanese firms on overseas markets – either through trade or foreign revenues.

With fiscal policy expected to remain expansionary, and the BoJ inclined to move slowly, the macro backdrop continues to favor softer JPY. For investors that are bullish on Japan, this points to staying hedged on the currency risk. Vehicles like ZJPN/F remain well‑positioned to benefit in this environment.

Chart 1 – Sovereign Debt/GDP for Select Countries

Chart 2 – Nikkei 225 and USD/JPY Relationship Over Time