Macro Notes - Where Does Gold Go From Here?

January 27, 2026

You may have heard that gold prices topped US$5000 per ounce for the first time in history earlier this week. Correspondingly, we’ve also seen massive bid interest for other precious metals (silver, platinum, palladium) as well – implying this is a macro driven trade as opposed to gold only.

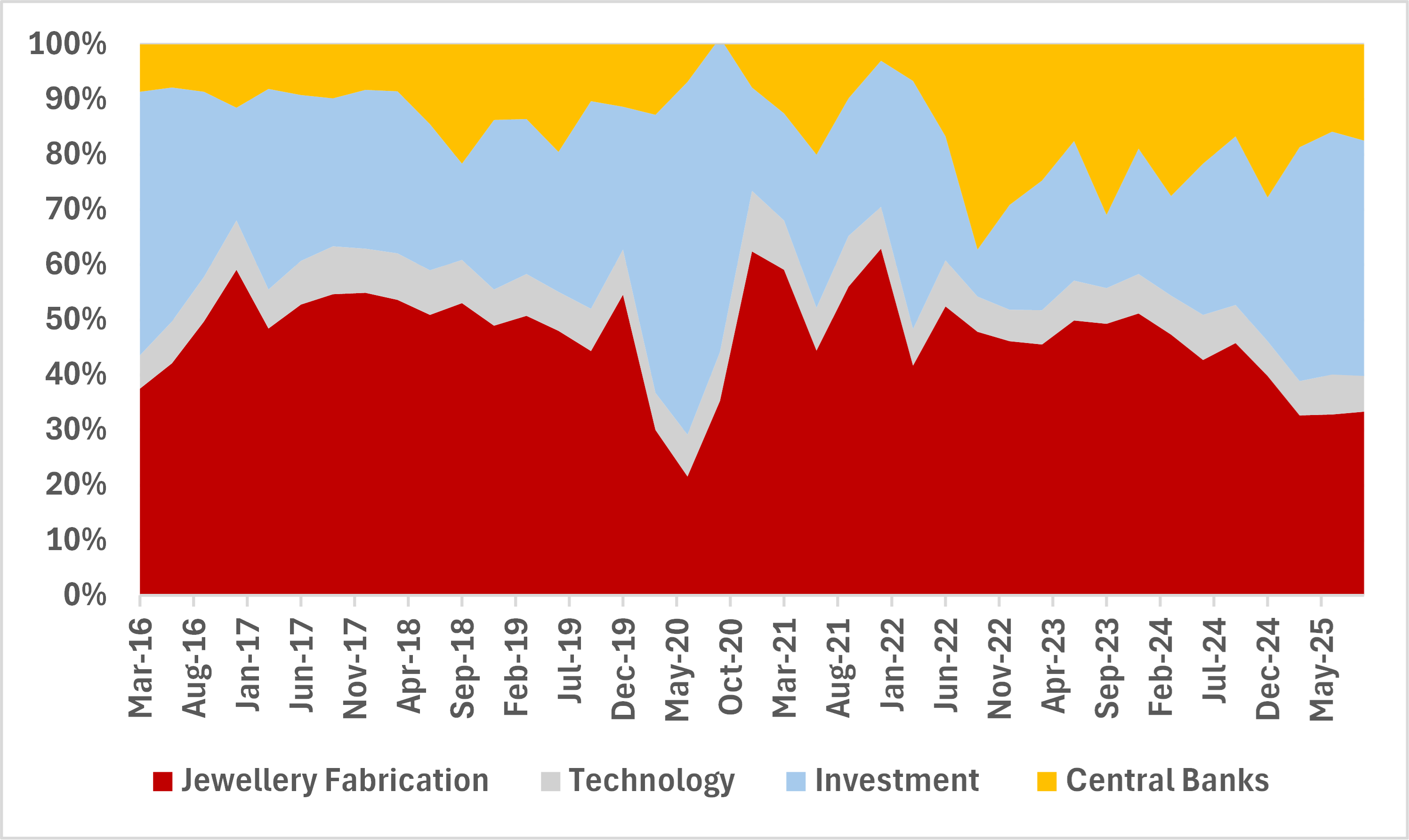

Chart 1 breaks down the percentage of total demand by segment for gold on a quarterly basis. What is important to take note of is that the decline in demand from jewellery fabrication over the past few years has been offset by pick-ups in central bank and investment flows.

We’ll make the following points on this transition in demand:

- Central banks have been ramping up gold buying since early 2022. Given the timing (the start of the Russia/Ukraine war and the freezing of Russian offshore assets), we’d venture to say that foreign central banks have become more sensitive to holding USD assets outside of their countries. The unpredictability of the current geopolitical backdrop has likely escalated this further.

- Investment flows have increased substantially (both at the retail and institutional levels). There is a fair bit of demand elasticity here as well – when prices rise, so too does demand. This could also reflect general angst about fixed income as a diversifier given the massive increase in sovereign supply and the rise in global term premiums. Precious metals offer more as diversification instruments in those environments.

Is there general concern about the nature of the rally so far? Yes. But if you’re an investor that is looking to liquidate your gold holdings – what are you going to buy? Stocks are pretty expensive, (especially in the US) while the risks are tilted towards higher yields in the developed world. On top of everything, it feels like we’re actually in the midst of a regime change (the ‘post Bretton Woods’ regime that has held since the early ‘70s feels like its run its course). Metals – especially precious metals – are the release valve in that sort of environment.

Given the unpredictability of the geopolitical backdrop and how overweight central banks are when it comes to USTs, our own sense is that dips in gold, silver and other precious metals will continue to be bought. That won’t change until we see a more meaningful correction in stocks/bonds or if things switch back to being ‘normal’ in terms of international trade and geopolitics.

It doesn’t feel like we’re close to either at this point. As such, we’re staying long gold via ZWGD.

Chart 1 – Percentage of Total Gold Demand by Segment

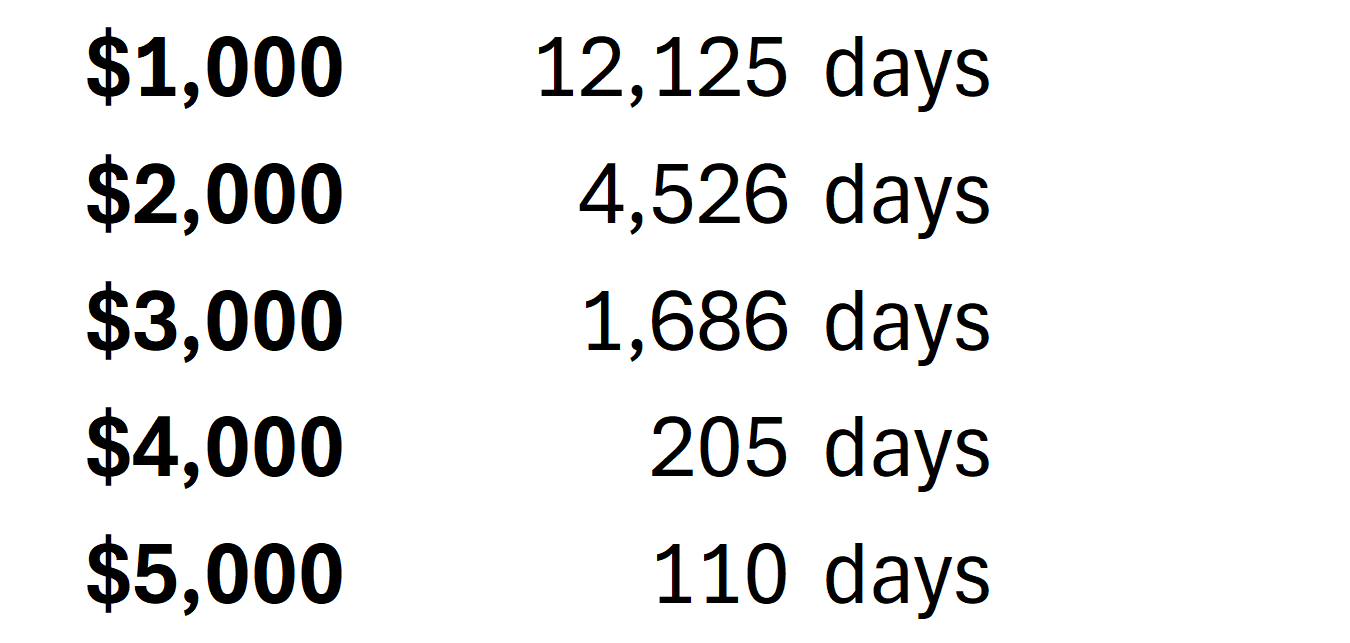

Table 1 – How long it took Gold to reach milestone levels (since start of 1975)