Deepen fixed income diversification, unlock yield potential: A CLO ETF primer

Broadly diversified across many different industries and anchored by high-rated tranches, collateralized loan obligations (CLOs) offer advantages over other fixed income securities. Folding them into an efficient ETF structure has just lowered the barrier to the investment opportunity they present.

May 28, 2025

There is a popular notion that diversification is the only free lunch in investing. To use an insurance concept, spreading the risk avoids unsavoury consequences that may result from more concentrated portfolios.

Although investing generally applies diversification across asset classes, there is a particular need to apply within asset classes, as well. Sector, capitalization and regional diversification are commonly sought in equities. By contrast, fixed income diversification has a tendency be much more staid, toggling between the binary choices of government and Investment Grade (IG) corporate bonds.

Broader diversification into High Yield (HY) or Emerging Market (EM) bonds can often offer significant spread over government bonds, enriching fixed income allocations with additional yield. More over, capital allocators are now able to diversify even more broadly through collateralized loan obligations, or CLOs, a compelling asset category that provides attractive risk/return profiles to broaden diversification and add more yield to portfolios while maintaining a liquidity budget to ensure flexibility in ever-changing markets.

BMO Global Asset Management listed the BMO AAA CLO ETF (ticker: ZAAA) on 2 May 2025, demonstrating its leadership in bringing innovative solutions to investors. Very competitively priced at 20 basis points (bps), ZAAA provides the transparency, liquidity and scalability offered within an ETF to assets that would otherwise be difficult for many managers to access.

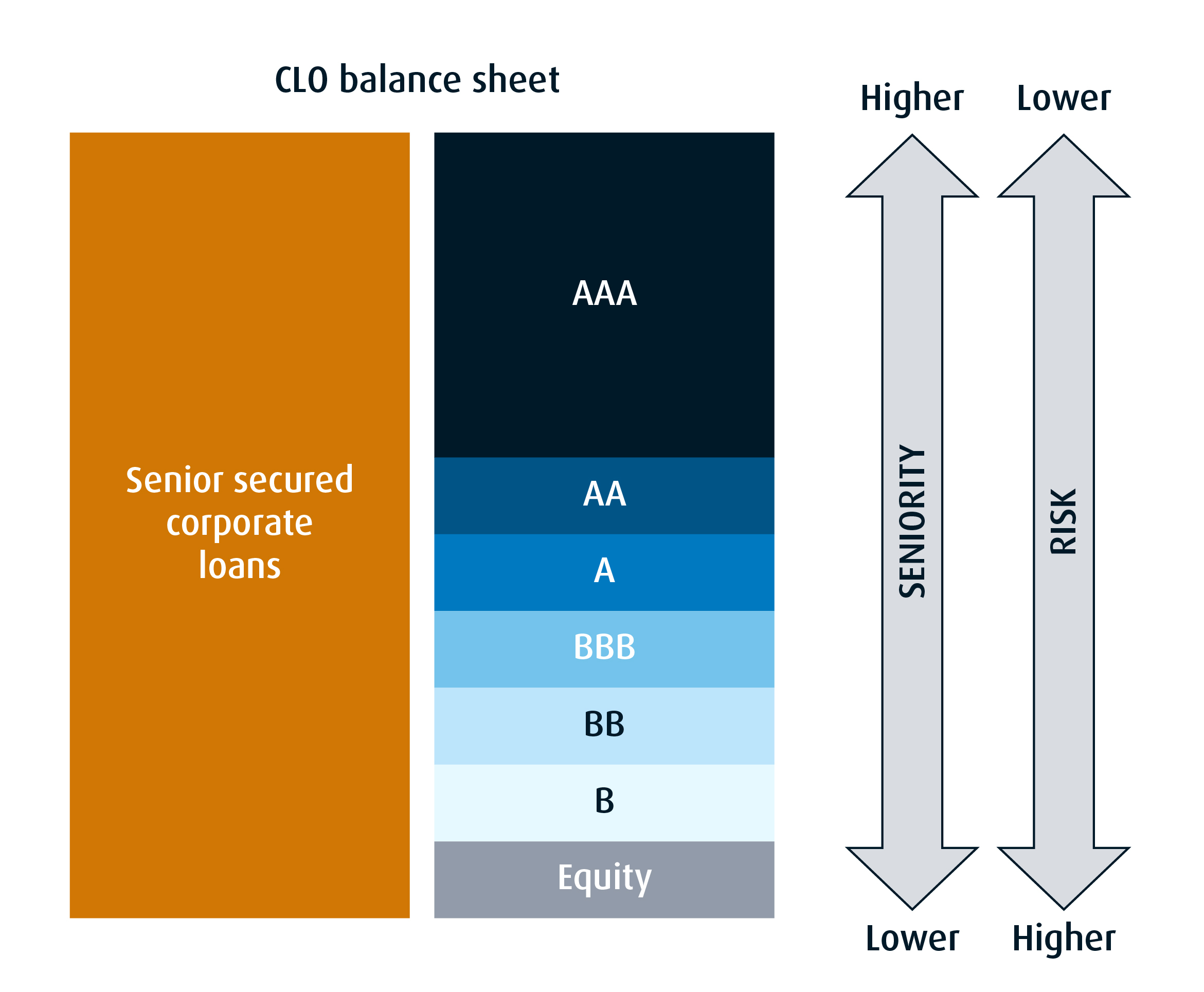

CLOs are an interesting structure, representing a broadly diversified set of loans across many different industries. Loans are rated in tranches, ranging from AAA, the most senior with first payment priority and the greatest insulation from losses, down to B, which provides the highest total return but must bear the greatest risk of loss.

Of perhaps particular interest to many investors, unlike traditional bonds, CLOs pay a floating rate that rises and falls across interest rate cycles, ensuring investors receive interest payments attuned to monetary changes over time.

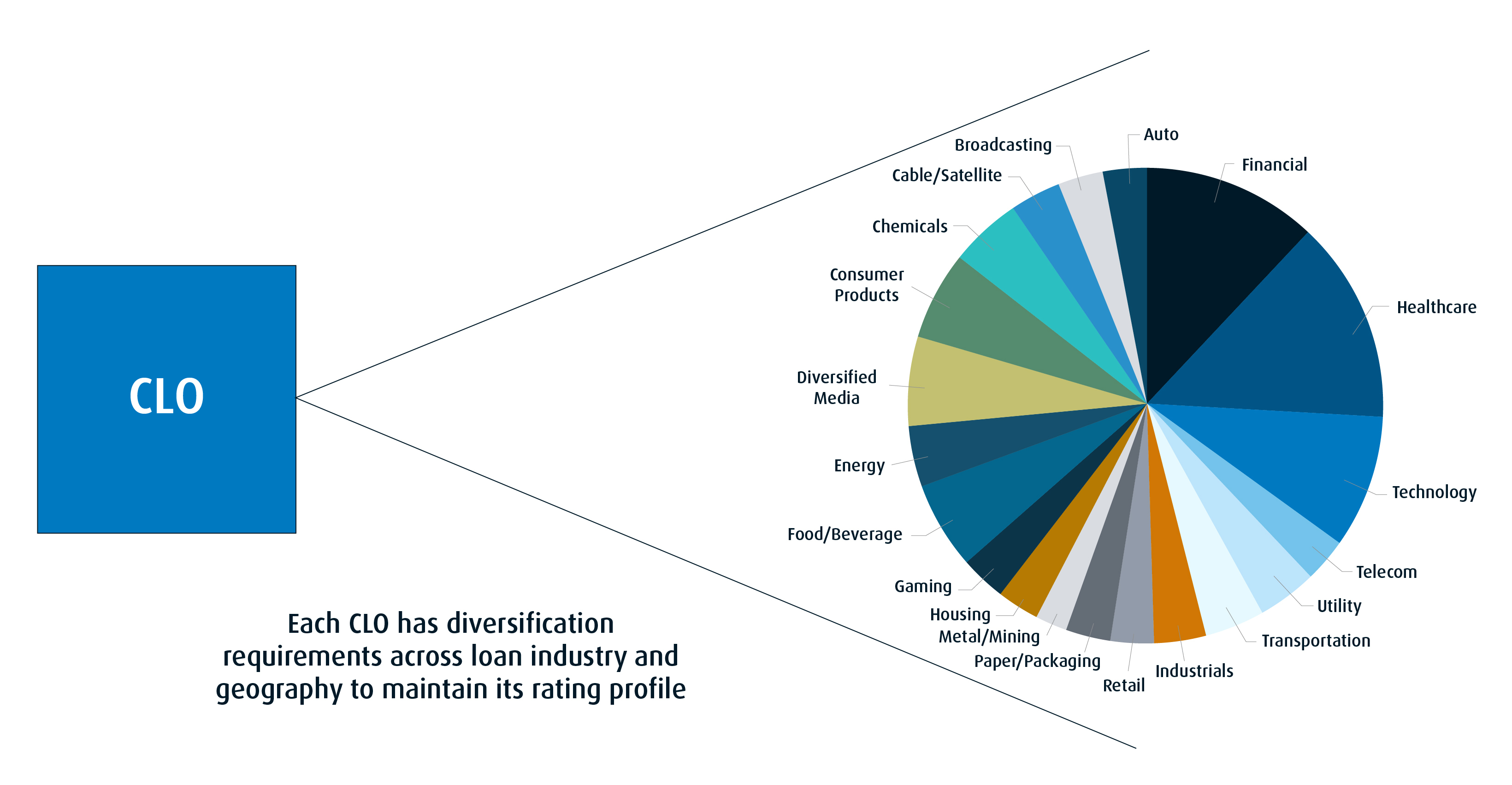

CLO managers strive to maintain broad diversification to enhance their ratings. In fact, the various Nationally Recognized Statistical Rating Organizations like Moody’s, A.M. Best, Fitch and S&P use three core collateral quality tests to help investors:

- Weighted Average Rating Factor, or WARF, establishes a minimum rating for inclusion in the CLO;

- Weighted Average Spread, or WAS, establishes a minimum spread required above a base rate;

- Diversity test, which requires a CLO to maintain industry breadth and to minimize single issuer risk (see below).

CLO diversification

Because CLOs are actively managed and because diversification and spread insulation are part of the rating process, historical losses in CLOs have been less severe than in the IG bond market:

As the table below illustrates, across the credit spectrum (AAA-B), default rates among CLO assets compare favourably against corporate debt.

CLOs vs. corporate debt comparison

Original rating category |

CLO |

Corporate |

|

5-year |

10-year |

||

AAA |

0.00% |

0.42% |

0.83% |

AA |

0.03% |

0.41% |

0.96% |

A |

0.15% |

0.64% |

1.65% |

BBB |

0.30% |

1.79% |

3.93% |

BB |

1.26% |

7.26% |

13.35% |

B |

3.36% |

17.48% |

24.79% |

Source: Standard & Poor’s/BMO Global Asset Management, as of April 30, 2025.

In short, ZAAA helps investment counsellors and multi-family offices broaden their fixed income allocations. The combination of floating rates, higher yields low default history compared to corporate bonds and broad industry diversification offer a compelling value proposition. More, when blended with the liquidity and scalability offered within an ETF format, accessibility is no longer a significant obstacle, greatly enhancing the appeal of CLOs within the manager’s overall fixed income portfolio construction.

Many investment counsellors and multi-family offices have deep expertise and conviction in equities but lack equal resources in fixed income. Instruments like ZAAA (AAA-rated CLO), in addition to vehicles such as the BMO High Yield US Corporate Bond Hedged to CAD Index ETF (ticker: ZHY), BMO Floating Rate High Yield ETF (ticker: ZFH) and BMO Emerging Markets Bond Hedged to CAD Index ETF (ticker: ZEF) (EM sovereign bonds, debt-to-GDP weighted), provide liquidity and a deep data set to model risk and return for clients.

These transparent and liquid listings enable counsellors to make sound macroeconomic evaluations to enhance portfolios and, hopefully, earn a larger share of wallet.

Disclaimers:

For Advisor and institutional use.

This article is for information purposes only. The information contained herein is not, and should not be construed as investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

The viewpoints expressed by the Portfolio Manager’s represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent simplified prospectus.

CLOs are floating- or fixed-rate debt securities issued in different tranches, with varying degrees of risk, by trusts or other special purpose vehicles (“CLO Issuers”) and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The BMO ETF pursues its investment objective by investing, under normal circumstances, at least 85% of its net assets in CLOs that, at the time of purchase, are rated AAA or the equivalent by a nationally recognized statistical rating organization.

AAA herein refers to the order of payments, should there be any defaults, and does not represent the ratings of the underlying loans within the CLO. If there are loan defaults or the CLO Issuer’s collateral otherwise underperforms, scheduled payments to senior tranches take precedence over those of mezzanine tranches (a tranche or tranches subordinated to the senior tranche), and scheduled payments to mezzanine tranches take precedence over those to subordinated/equity tranches. The riskiest portion is the “Equity” tranche, which bears the first losses and is expected to bear all or the bulk of defaults from the corporate loans held by the CLO Issuer serves to protect the other, more senior tranches from default.

The portfolio holdings are subject to change without notice and only represent a small percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

Commissions, management fees and expenses all may be associated with investments in exchange traded funds. Please read the ETF Facts or simplified prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s simplified prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., which is an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.