Why AAA CLO ETFs Have Remained Resilient in 2026

An ability to earn incremental income through senior, floating rate exposures has been a powerful tailwind for CLO ETFs through a volatile market this year.

Despite heightened volatility across global markets in early 2026, collateralized loan obligation (CLO) ETFs have continued to attract strong investor demand. Year‑to‑date inflows have approached $6 billion,1 a notable outcome given widespread concerns around private credit quality, software-sector weakness, and ongoing geopolitical uncertainty. This resilience stands in contrast to softer flows across several adjacent asset classes and highlights the evolving role of CLO ETFs within modern fixed‑income portfolios.

Three primary factors help explain why CLO ETF demand has remained robust:

- The persistence of high base interest rates,

- a pronounced investor preference for senior-quality exposure,

- and competitive total return performance relative to other income-oriented assets.

High Base Rates Continue to Support CLO Demand

Entering 2026, the market consensus anticipated multiple Federal Reserve (Fed) rate cuts following signs of cooling inflation in late 2025. While headline CPI data had declined meaningfully by year-end, inflation pressures proved more persistent in early 2026, driven in part by higher energy prices and a still-tight labour market. As a result, the Fed has remained on hold, keeping policy rates in a restrictive range.

This environment has been particularly supportive for floating-rate assets such as CLOs. With 3‑month SOFR2 remaining near the mid‑3% range, yields on AAA-rated CLO tranches embedded within ETFs have remained attractive on an absolute basis. For many investors, this has translated into a meaningful yield pickup versus traditional money market funds, whose returns tend to track closer to the Fed’s policy rate itself.

Crucially, this yield advantage has arrived without requiring investors to move materially down the credit spectrum. In a market where rate volatility remains elevated and duration risk is a concern, the ability to earn incremental income3 through senior, floating‑rate exposure has been a powerful tailwind for CLO ETFs.

A Structural Tilt Toward AAA Quality

A second driver of resilient flows has been the strong bias toward high‑quality exposure within the CLO ETF universe. Approximately 90% of U.S. CLO ETF assets are concentrated in AAA-rated tranches,4 positioning the category squarely within the “up‑in‑quality” trade that has characterized fixed‑income allocation decisions this year.

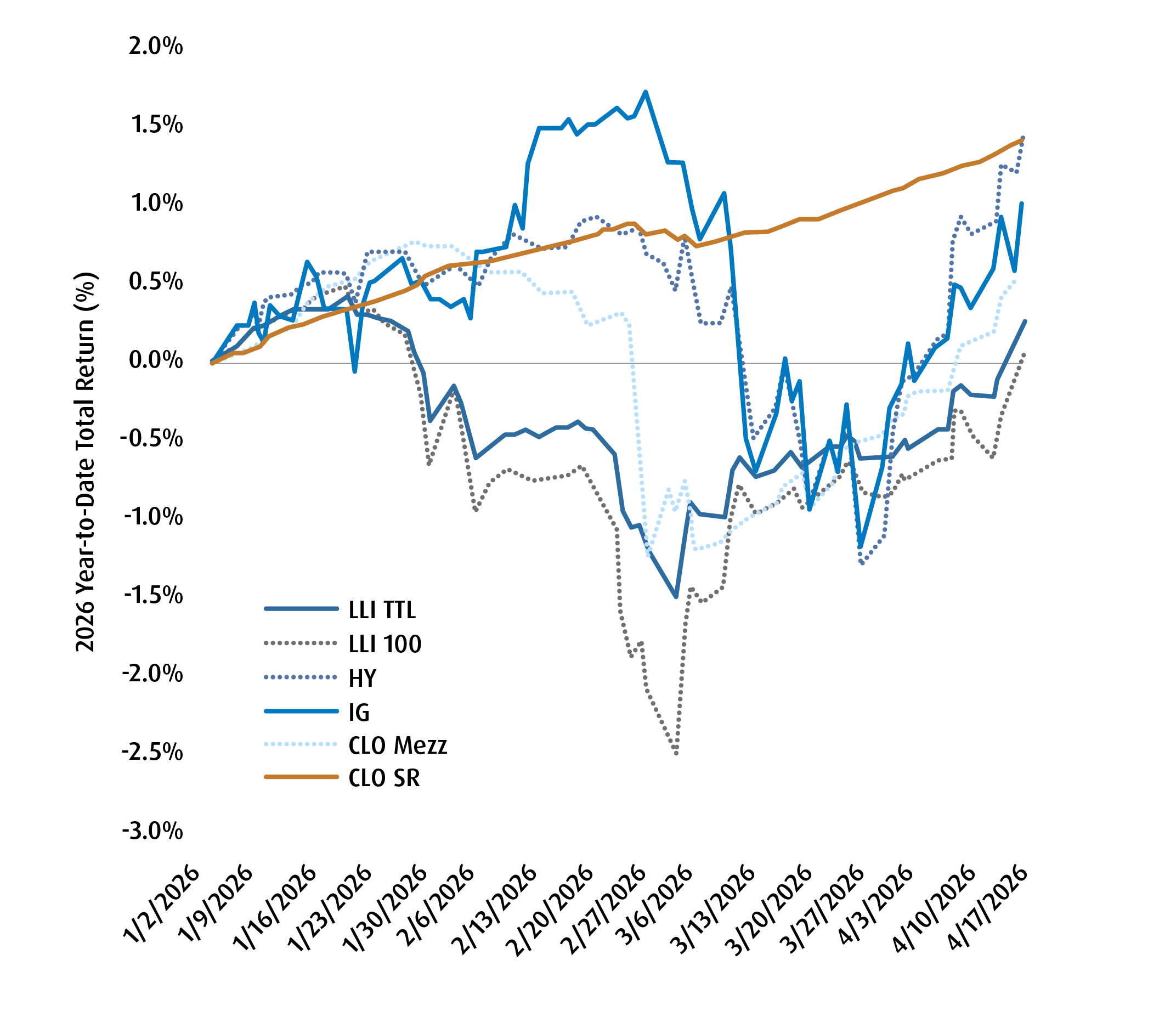

This preference has been reinforced by broader market behaviour. Across leveraged loans and high yield bonds, higher‑quality segments have consistently outperformed lower‑rated counterparts in 2026.

Relative Returns Year-to-Date

AAA CLO exposure has served as a way for investors to remain engaged with credit markets while mitigating downside risk.

This quality bias has been visible not only in ETF flows but also in underlying CLO market dynamics. Senior tranches have exhibited greater spread stability in the primary market and stronger price resilience in secondary trading. These characteristics have reinforced investor confidence in CLO ETFs as a relatively defensive credit allocation during a period of elevated macro uncertainty.

Competitive Total Return Performance

CLO ETFs have also delivered compelling results from a total return perspective. Through the early part of 2026, among fixed income categories, CLO ETFs that focus on AAA-rated securities, such as the BMO GAM AAA CLO ETF (ZAAA), have been among the top-performing major fixed‑income ETF categories.

CLO ETF returns have compared favorably not only on an absolute basis but also relative to flows. When measured as year‑to‑date inflows relative to fund size, CLO ETFs rank among the strongest across a broad universe spanning equities, government bonds, loans, and corporate credit. This suggests that the category remains underpenetrated and continues to attract incremental allocations from investors still building exposure.

A Market Still Early in Its Evolution

Another important contextual factor is the relative youth of the CLO ETF market.

While CLO issuance itself has been a core feature of structured credit markets for decades, CLO ETFs only began to see meaningful inflows starting in 2022, following the Fed’s pivot toward tighter monetary policy.

As a result, the asset class is still in an expansion phase compared with more mature categories such as equities, Treasuries, or corporate bonds. This helps explain why flows have remained positive even amid periods of broader risk aversion. For many investors, CLO ETFs represent a relatively new solution for accessing floating‑rate credit with daily liquidity and transparent pricing.

Performance (%)

| Fund Name | Ticker | Year-to-Date | 1-Month | 3-Month | 6-Month | 1-Year | 3-Year | 5-Year | 10-Year | Since Inception | Inception Date |

| BMO AAA CLO ETF (Hedged Units) |

ZAAA.F | 0.82% | 0.49% | 0.53% | 1.32% | 3.32% | — | — | — | 3.24% | 2025-04-30 |

| BMO AAA CLO ETF | ZAAA | 0.35% | -1.71% | 0.72% | -0.99% | 3.66% | — | — | — | 3.20% | 2025-04-30 |

| BMO AAA CLO ETF (USD Units) |

ZAAA.U | 1.40% | 0.66% | 0.97% | 2.23% | 5.19% | — | — | — | 5.12% | 2025-04-30 |

Source: BMO Global Asset Management, Bloomberg, as of April 30, 2026. Past performance is not indicative of future results.

1 ETF Trends, VettaFi, April 23, 2026.

2 The forward-looking, three-month interest rate estimate.

3 Total distribution per unit for tax purpose: The exact tax treatment of the distributions for a calendar year is calculated after the BMO Funds’ tax year-end. As a result, investors will receive an official tax statement from their broker detailing the type of income they have to report for tax purposes for the entire year and not for each distribution. Please note that before the tax treatment is calculated there is no guarantee on what proportion of potentially generated cash flow will be income, capital gains or dividends.

4 ETF Express, September, 2025.

Disclaimers

Advisor Use Only.

This article is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

The viewpoints expressed represent an assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

CLOs are floating- or fixed-rate debt securities issued in different tranches, with varying degrees of risk, by trusts or other special purpose vehicles (“CLO Issuers”) and backed by an underlying portfolio consisting primarily of below investment-grade corporate loans. The BMO AAA CLO ETF pursues its investment objective by investing, under normal circumstances, at least 85% of its net assets in CLOs that, at the time of purchase, are rated AAA or the equivalent by a nationally recognized statistical rating organization. The BMO BBB CLO ETF pursues its investment objective by investing, under normal circumstances, at least 75% of its net assets in CLOs that are BBB-rated at the time of purchase.

AAA herein refers to the order of payments, should there be any defaults, and does not represent the ratings of the underlying loans within the CLO. If there are loan defaults or the CLO Issuer’s collateral otherwise underperforms, scheduled payments to senior tranches take precedence over those of mezzanine tranches (a tranche or tranches subordinated to the senior tranche; e.g., AAA tranches are the most senior, while BBB tranches are mezzanine-level), and scheduled payments to mezzanine tranches take precedence over those to subordinated/equity tranches. The riskiest portion is the “Equity” tranche, which bears the first losses and is expected to bear all or the bulk of defaults from the corporate loans held by the CLO Issuer serves to protect the other, more senior tranches from default.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., an investment fund manager, a portfolio manager, and a separate legal entity from Bank of Montreal.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

This article may contain links to other sites that BMO Global Asset Management (BMO GAM) does not own or operate. Any content from or links to a third-party website are not reviewed or endorsed by BMO GAM. Investors use any external websites or third-party content at their own risk. Accordingly, BMO GAM disclaims any responsibility for them.