Macro Notes - What Venezuela Means for Canada and Markets

January 04, 2026

Admittedly, we weren’t planning on re-starting our Macro Notes publication until next week. However, we also didn’t have the US attacking Venezuela and extraditing its President by force on the geopolitical bingo card for January either. This is an extraordinary development given the potential implications at play for the markets.

We’re not going to comment on the politics and legality of what happened over the weekend. Instead, we’re going to focus on the clearest conduit to the markets – the implications for the commodities market and what this means for Canada going forward. We’ll start with the latter.

What does all this mean for the Canadian oil sector?

The heavy crude produced in Venezuela’s Orinico belt has the exact same makeup as the grade produced in Alberta. Venezuela also benefits from its proximity to tidewater whereas the Albertan oil sands have to be routed through BC to reach the Pacific and there have been considerable roadblocks to pipeline development.

However – the outlook isn’t as cloudy for Canada as some would lead you to believe.

i.) There are still meaningful hurdles to get Venezuelan production back up to its potential. It’s estimated that it will cost over US$100 billion to get the necessary infrastructure upgrades for Venezuela to return to the 3-4mln bbl/d range (where it was in the late-90s) from 1mln bbl/d now. But the country also has a long history of political volatility, worker strikes and violent crime that may hinder private investment and confidence.

ii.) If production does come back and sanctions are lifted – it will most easily flow to the US Gulf Coast refineries and likely outcompete whatever Canadian crude is consumed there.

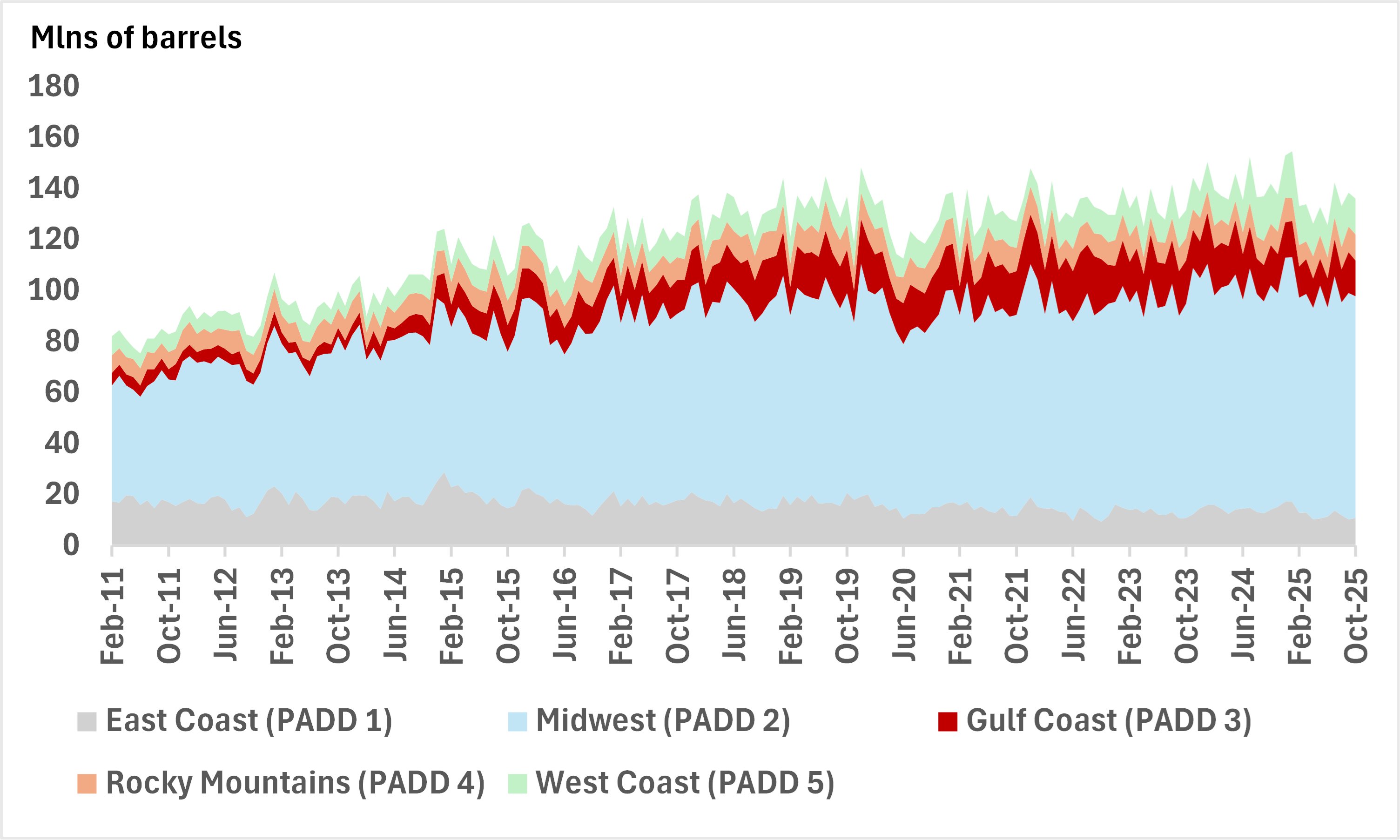

The thing is - the majority of Canadian crude exported is consumed in the US Midwest (see Charts 1 and 2). Only a small amount of Canadian crude actually makes it to the US Gulf Coast.

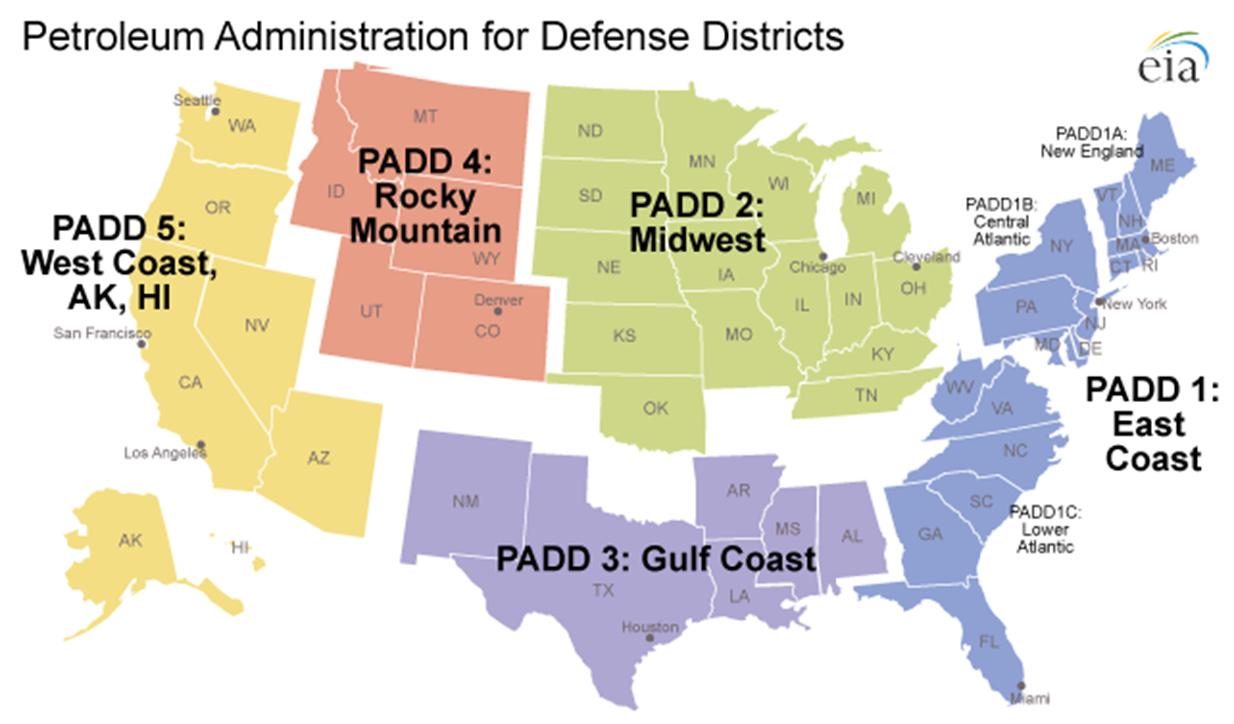

iii.) The pipelines that link Canadian supply to the American refineries flow from north to south. Retooling them to flow from south to north would cost tens of billions of US dollars and wouldn’t make much economic sense. It’s unlikely that Venezuelan crude oil will end up in the US region where Canadian crude is consumed (PADD 2).

If anything, this is likely to be an accelerant for Canada to diversify away from the US when it comes to sourcing energy demand.

For markets…

- The risks to crude prices are to the downside over the medium-term. That is because Venezuela has been effectively shut out of the crude market for years already, and the attack over the weekend make it more likely that production will come back at some point.

- This is likely to add another leg to the gold rally. We cannot look past the ‘signal effect’ of the US attacking a country and then signalling additional military action could take place against other countries. That is likely to increase efforts by foreign central banks to buy gold for reasons ranging from geopolitical hedging to sanctions resilience or de-dollarization.

- This could also mean demand for certain softs (coffee) could increase as well given that a substantial portion of global supply is produced in Colombia and Mexico.

- Stepping back a bit more – there is likely to be even more pressure on countries to spend more on defense and infrastructure going forward.

On a side note – Happy New Year to everyone!

Chart 1 – US Petroleum Administration for Defense Districts (PADD) Regions

Chart 2 - Canadian Crude Exports to the US by Region