Macro Notes - Why a Cap on Credit Card Interest Could be a Macro Risk

January 13, 2026

Let’s pause and recap the announcements that have from the White House since the new year began:

i.) A proposed ban on institutional investors purchasing single-family homes.

ii.) An order to GSE’s (Fannie Mae and Freddie Mac) to purchase US$200bln in agency MBS – which should (in theory) bring down mortgage rates.

iii.) Attempts to force defense firms to increase capex and production by preventing them from paying dividends or conducting share buybacks.

iv.) Launching a criminal investigation into the Fed Chair Jerome Powell.

v.) Transferring 30-50mln bbl of Venezuelan crude to the US custody.

vi.) Rolling out plans to cap credit card interest rates at 10% (effective January 20th).

Welcome to 2026, folks. And to think, we’re only 13 days in.

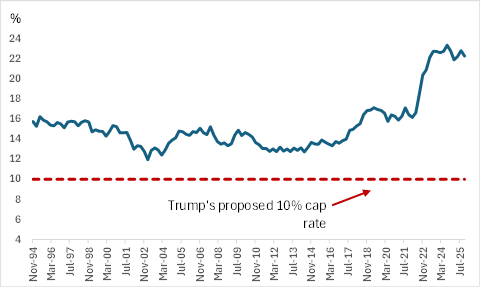

For today, we’re going to focus in on point vi). President Trump is now calling for a one-year cap on the interest rates for credit cards at 10% (effective January 20th). That’s down from an average 22.3% annualized percentage rate that commercial bank issuers charge as of November – according to data published by the Federal Reserve (Chart 1).

The president makes the argument that Americans are being “ripped off” by ultra-high interest rates charged on credit cards and frames the cap as one way to restore affordability.

But that looks past several of the reasons why credit cards have higher interest rates in the first place. For instance, consider the following:

- Credit loans are unsecured and loss heavy.

- Borrowers often have variable repayment patterns.

- The revolving ‘option’ embedded in a credit loan often means that borrowers increase balances when finances are at their worst.

- There are large costs for infrastructure (fraud protection, rewards programs, transaction processing, etc).

- A reliance on risk-based pricing (subprime borrowers are less likely to pay, which means that rates are usually more punitive for this segment).

The above isn’t an exhaustive list, but they all contribute to the higher cost to issue credit cards. If we assume a 6.8% return – that still implies that the cost stack is closer to 15% for most credit card issuers. By extension, that means that an interest cap set at 10% is way too low. To make things economical, issuers will either need to scale back on rewards/benefits, or more likely, they’ll cut back on credit lending. This results in de facto credit tightening that might actually end up curtailing household spending when the economy needs it most.

If there’s a market-related lesson from history you need to remember, it’s that rallies don’t end (or bubbles don’t pop) until financial conditions tighten by enough. Credit availability has now become an important macro risk to monitor for us all.

Chart 1 – Commercial Bank Interest Rate on Credit Card Plans