Weekly Basis Points - A Framework for Currency Hedging

March 15, 2026

- The decision to hedge currency risks or remain unhedged should be driven by two factors: your currency view and the correlation between the foreign asset and its currency. Negative correlations (e.g., US equities vs USD) typically favour staying unhedged to reduce volatility, while positive correlations (e.g., US Treasuries vs USD) usually favour hedging.

- Correlation — not just returns — determines the volatility impact of currency exposure. Currency can either stabilize or amplify portfolio volatility depending on how it moves relative to the underlying asset, making hedging a portfolio‑construction choice that should be revisited quarterly.

- The macro backdrop is turning more fragile as Middle East tensions lift oil prices, central banks hold steady, and risks shift toward stagflation. In this environment, the preferred stance is overweight equities (quality/defensives), overweight commodities, and underweight fixed income.

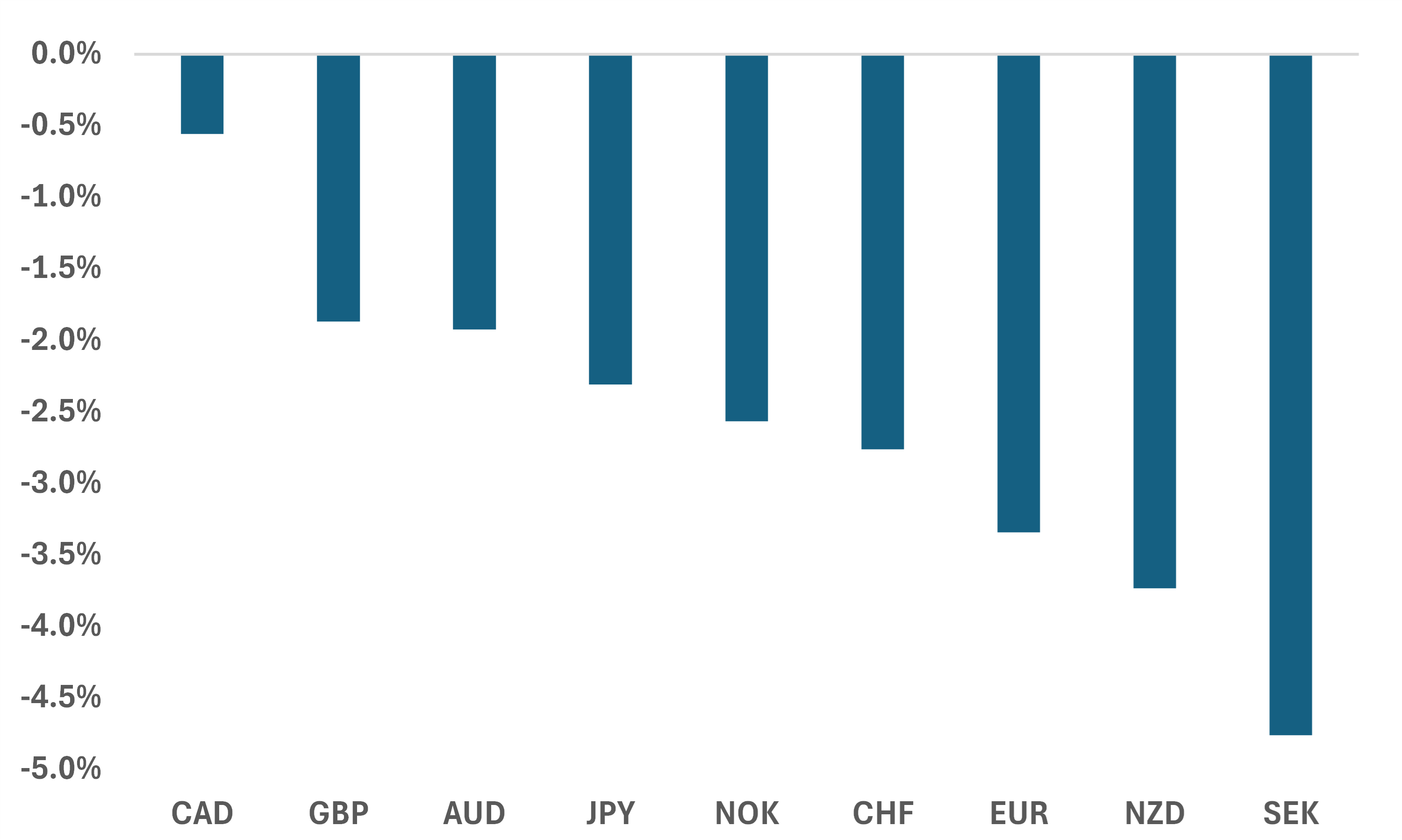

With geopolitical risk heightened since the start of the US/Israel/Iran conflict, the Canadian dollar has held up relatively well against the USD compared with many G‑10 currencies (Chart 1). But with the Bank of Canada maintaining a data‑dependent stance, USD/CAD still carries meaningful two‑way risk. For Canadian investors, this makes the classic “hedged or unhedged?” question more important — and more complicated — than usual.

Chart 1 – G-10 currency performance vs USD since the conflict began

Source: BMO GAM, Bloomberg

Indeed, Canadian investors should remember that currency returns can contribute or detract from overall portfolio performance in a meaningful way. In our minds, the decision to hedge FX risk (either partially or fully) comes down to the following:

- An investor’s view of the underlying currency pair. This will typically depend on several factors that often do not have stable relationships with the currency pair itself – making the exercise difficult.

- Whether the currency pair has traditionally been positively or negatively correlated with the underlying asset.

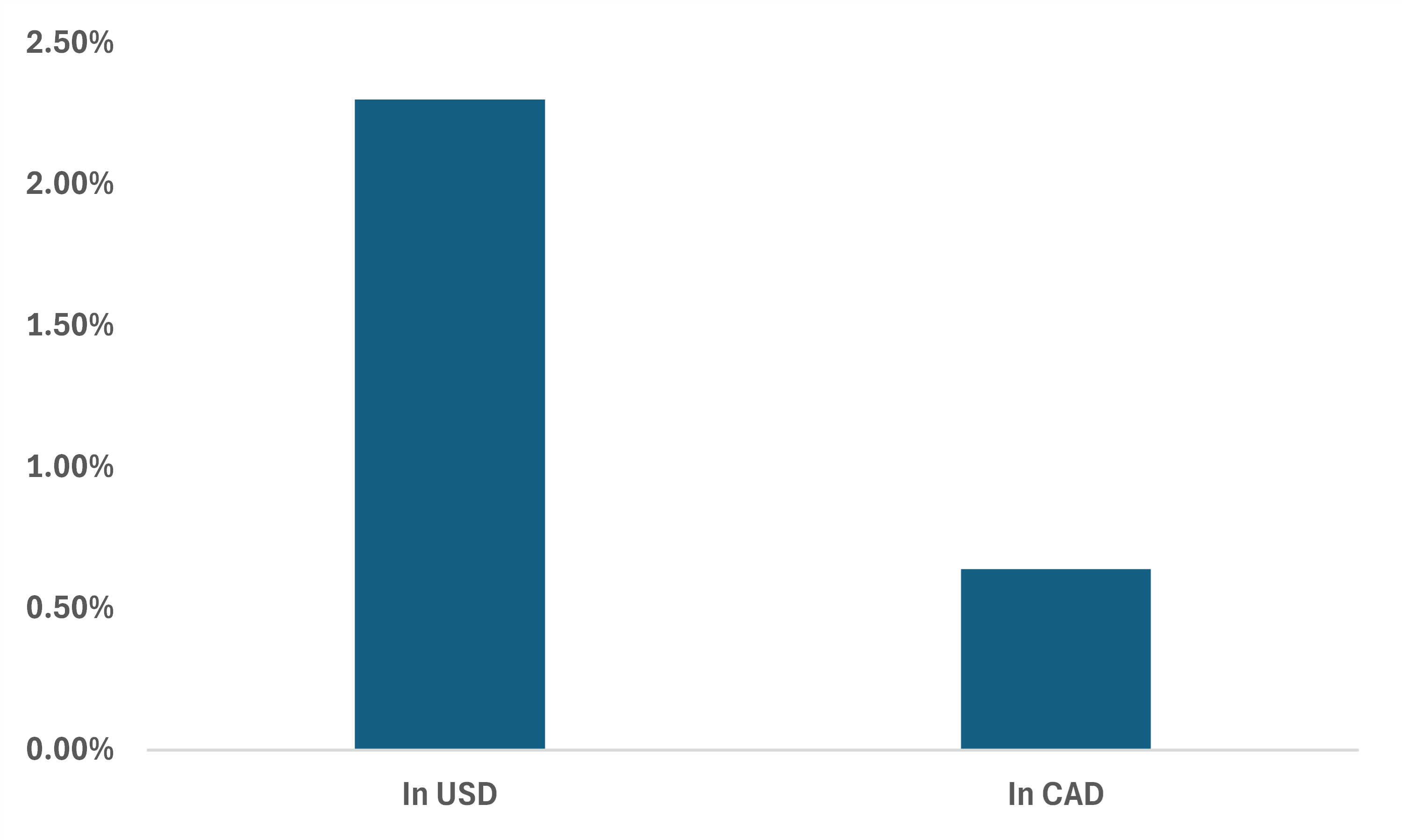

To demonstrate this, let’s look at Chart 2 which compares the total return for the S&P 500 in USD and CAD terms for Q4 of last year. In USD terms, the index was up 2.3% but since that period also corresponded to an outperforming loonie (USD/CAD moved lower by 1.4%), the index underperformed in CAD terms (0.64%). In this scenario, a Canadian investor who had elected to hedge their FX risk for Q4 would have been in the optimal position.

Chart 2 – S&P 500 total return for Q4 2025

However, focusing on returns masks something else that’s important to consider - volatility. Indeed, volatility is an important consideration in the ‘hedged versus unhedged’ decision given that it can mitigate compounding benefits for returns over time. Many investors assume hedging should always lower volatility because it removes currency fluctuations. In reality, the overall volatility of the exposure depends on how currency moves interact with the returns of the underlying.

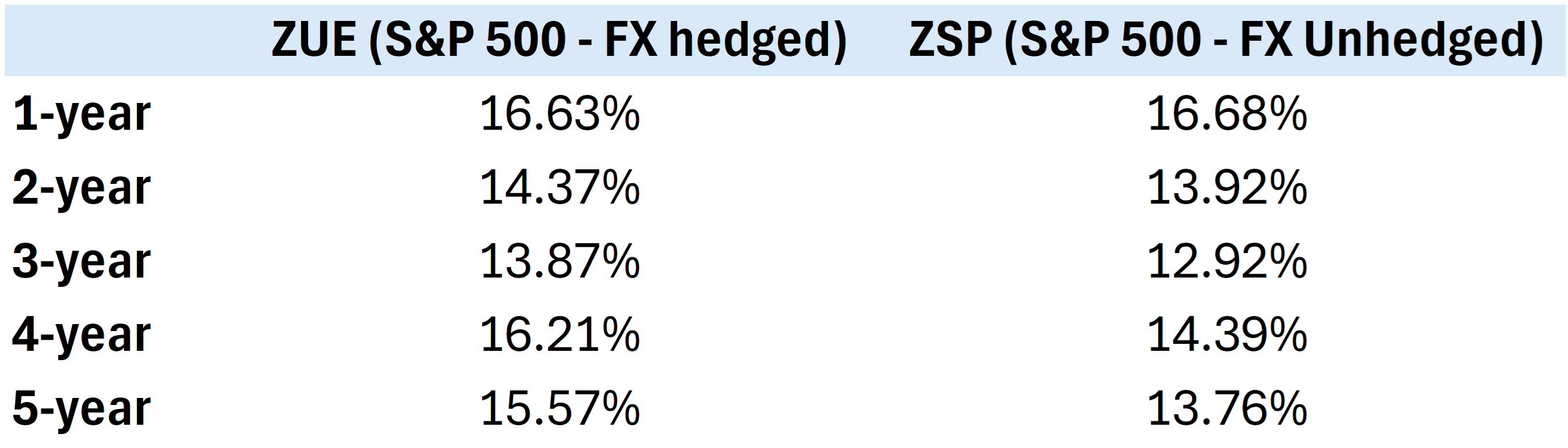

For instance, when a Canadian investor holds an unhedged US equity tracking ETF, they are effectively long both the US equity market and the USD. If USD performance is negatively correlated with US equities, that currency exposure can act as a stabilizer, lowering overall volatility at the margin. Since the S&P 500 is often negatively correlated with the USD, an unhedged ETF (for example - ZSP) can exhibit lower realized volatility than its hedged counterpart (ZUE), even if returns differ across periods (Table 1).

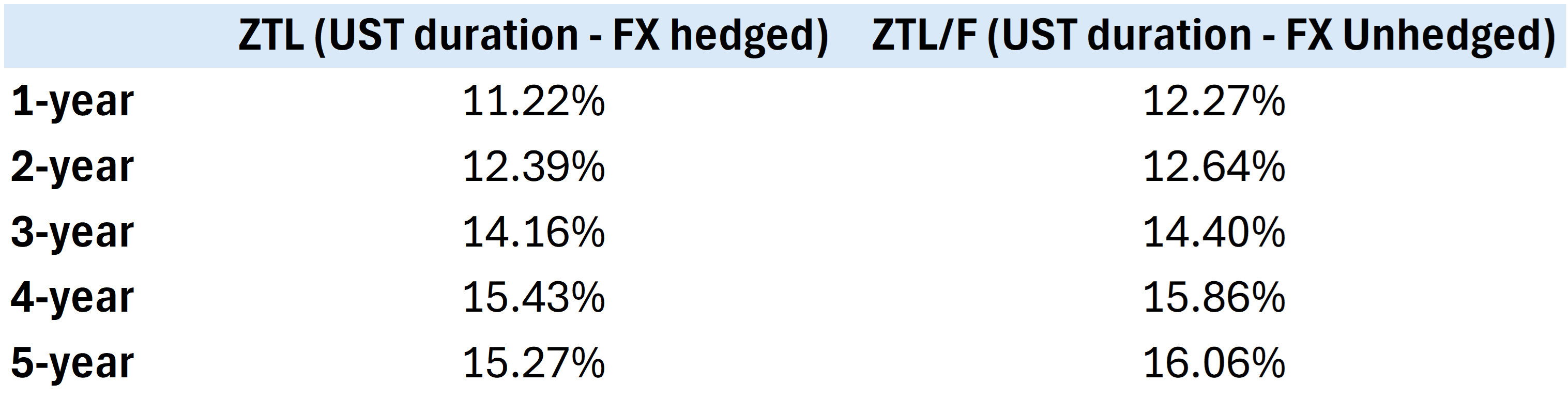

However, this very different when the underlying exposure is positively correlated to the US dollar. For instance, US treasuries tend to move with the US dollar during periods of risk aversion (positive correlation). To mitigate overall volatility, Canadians investing in US treasuries are better off hedging their exposure more often than not (see Table 2).

Table 1 – Average 90-day volatility comparison between hedged and unhedged US equity exposures

Table 2 – Average 90-day volatility comparison between hedged and unhedged US bond exposures

A Simple Rule to Follow…

As a rule, for any ETF that tracks a foreign market, if the basket of underlying securities is:

a) If the underlying asset is negatively correlated with the currency → unhedged lowers volatility.

b) If the underlying is positively correlated with the currency → hedged lowers volatility.

This rule can shift as correlation regimes evolve. If, for instance, the USD becomes positively correlated with equities due to a USD‑specific shock, hedging might become more attractive — assuming CAD isn’t underperforming at the same time.

All told, the above provides a framework for hedging decisions for our readers when it comes to investing outside of the Canadian market. To reiterate, when it comes to FX hedging, investors should:

- Start with a currency view.

- Assess the asset – currency correlation.

- Review the hedge stance on a quarterly basis as regimes and market conditions evolve.

This framework provides a durable approach to managing currency exposure in client portfolios.

Macro Regime Call

Current macro regime: ‘Fractured Expansion’ - strong but uneven growth (late cycle) + slow disinflation

Confidence: Medium | Horizon: 3-6 months

Policy regime: Neutral, but easing at the margin (monetary and fiscal)

Market regime: Fragile

Risks to call:

- Duration of the conflict and its impact on energy markets.

- Rise in inflation across DM that leads to re-tightening policy reaction functions.

- Benefits from AI-driven productivity are concentrated rather than distributed.

Portfolio Strategy

a.) Middle-East conflict: The key development over the weekend is that the Trump administration is now looking for assistance (from NATO, China) to re-starting shipping activity through Hormuz.

This speaks to the lack of options available to the US at this point. Other than a coordinated naval escort, the quickest path to get shipping activity back to normal is a ceasefire agreement that will almost assuredly guarantee Iranian sovereignty (backed by Russia and China). Right now, the US likely views this as untenable – which means oil prices keep rallying.

By extension, that means broad risk remains under pressure and bond yields push higher.

b.) Central bank decisions: Both the Bank of Canada and the Federal Reserve will finish deliberating on Wednesday.

Neither central bank is expected to adjust its policy and administered rates this week. However, we will be keeping an eye on how both frame higher oil prices from here. If there’s more concern about the degree of demand destruction from higher fuel prices, then we’ll be even more confident in our call that the macro regime is shifting from a reflationary backdrop to something more nefarious (stagflation).

Other than that…

- The RBA is expected to hike rates by 25bps on Monday night

- The ECB, BoE, SNB, and the Riksbank will announce decisions on Thursday and all of them are expected to stay on hold.

c.) Key data: Canada CPI (Feb) out on Monday morning.

Even ahead of the Middle East conflict, energy prices were firming – which is likely to drive the m/m print closer to 0.6%. However, the degree of economic slack is ample which means that the BoC isn’t likely to be perturbed by upside inflation risks at this point.

d.) Macro regime: We’re making the following changes to our regime call.

- First, we’re updating the market call to be fragile without the qualifier that it is ‘selectively risk supportive’.

- Second, we’re adding another risk to our call. Indeed, the duration of the Middle East conflict and its impact on energy markets is something that could easily lead to a quicker transition to ‘stagflation’ from the current regime that we’re in (‘fractured expansion’ + slow disinflation).

In our current playbook, we are slightly overweight equities (with a focus on US quality + defensives), overweight commodities (our preferred diversification play) and underweight fixed income.

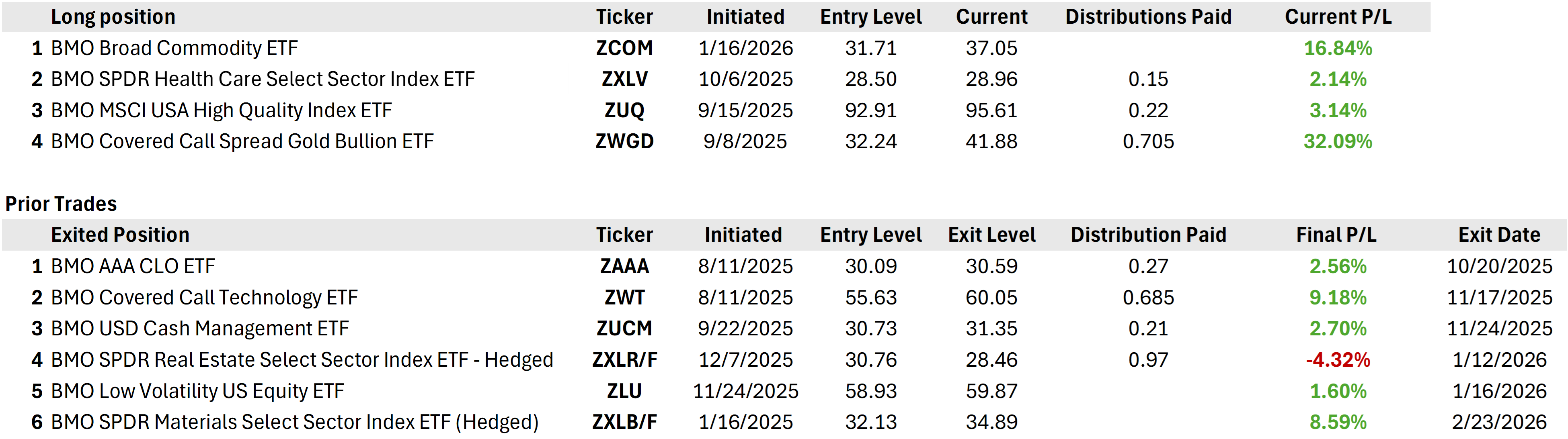

Book of Trades