Weekly Basis Points - A Market Led by the Few = An Opportunity for the Many

February 02, 2026

- US equity markets are highly concentrated, with a handful of mega‑caps driving most of the S&P 500’s returns and risk.

- This concentration makes the index more fragile, as even small disappointments from the largest names can disproportionately move the market.

- Equal‑weight US indices offer a compelling alternative, benefiting from broader earnings momentum, sector rotation, and a shift toward wider market participation heading into 2026.

It wouldn’t be Groundhog Day without a mention of how concentrated US equity markets have become. And that’s exactly what we’re focusing on this week — along with a potential solution for clients who remain concerned about these risks.

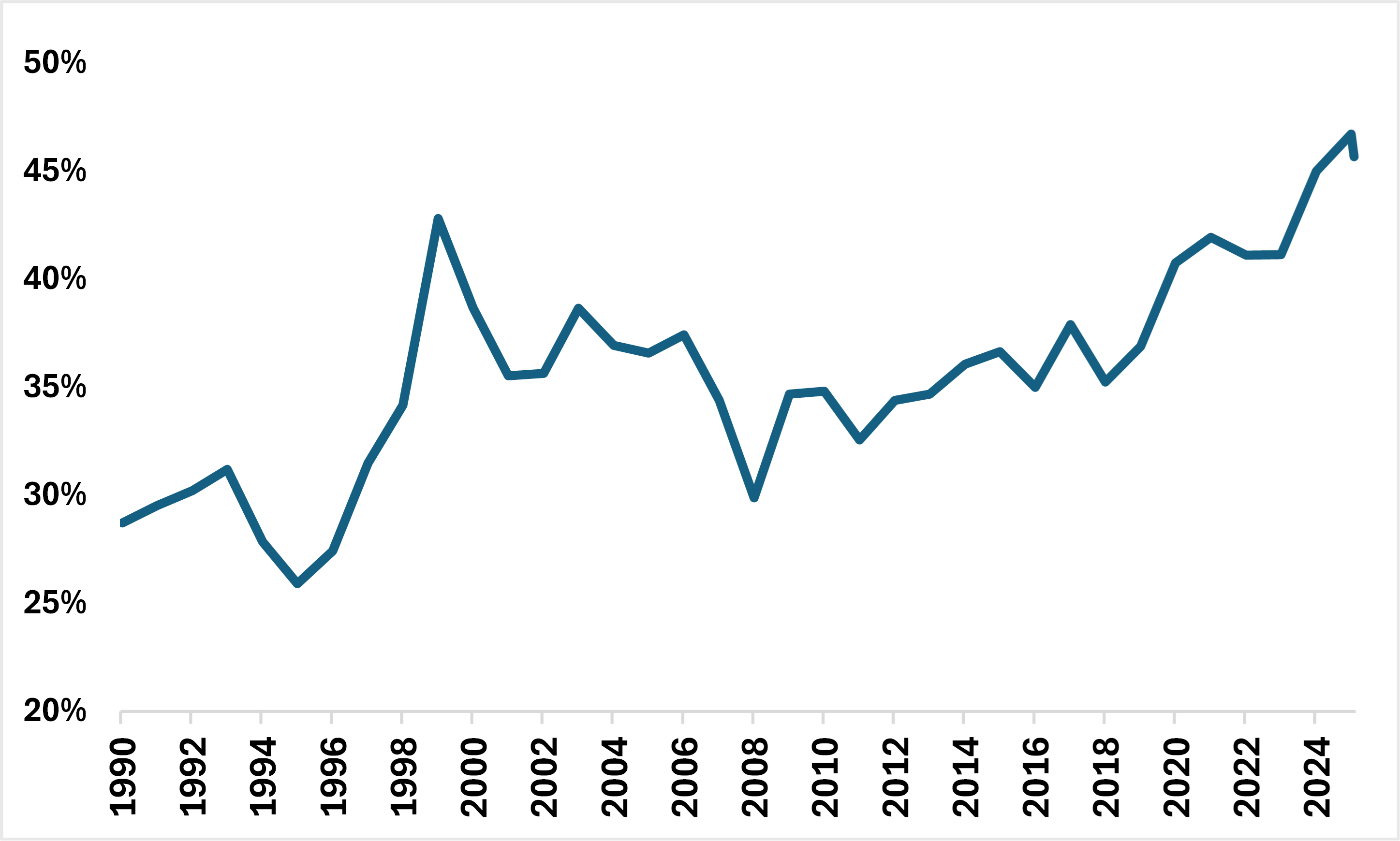

Market concentration has been doing much of the heavy lifting for some time now. As shown in Chart 1, the combined weight of the top two sectors in the S&P 500 has climbed to over 45% — the highest level since the early 2000s. Today, technology and communications firms dominate the index, and if we dig deeper, the “Mag 7” have accounted for between 40 – 60% of the S&P 500’s total returns since 2022.

Chart 1 – S&P 500: Contribution weights of the top two sectors since 1990

Given these figures, it’s fair to say the S&P 500 is no longer a broad market index. Instead, it’s become a handful of mega-cap stocks with an index attached.

The unhappy byproduct of this, of course, is that risks have become concentrated as well. Take last week’s earnings releases, especially Microsoft’s. Despite beating expectations on both earnings and revenue, the stock sold off afterward. Many attributed the reaction to rising AI‑related capital expenditures and the lack of a clear path to long-run profitability from those investments. With so much optimism already priced in, markets are now rewarding growth with lower risk — not increased spending and uncertainty. How else do we explain another potential quarter of double-digit earnings growth and only a +1.4% year-to-date return for the S&P 500?

This is one reason — among many — why we see greater potential in equal‑weighted US equity indices versus market‑cap‑weighted ones. A long position in equal weight is effectively a bet that the average stock will do just fine, rather than a reliance on a small group of names needing to remain perfect. And as AI‑related technologies diffuse into other sectors, there’s a strong case for broader earnings momentum compared with what we’ve seen in recent years. That should support a rotation in market leadership away from tech and communications.

Are there other ways to play a “broadening out” of leadership in US equities? Sure. Some may look at small/mid cap indices potentially. However, what concerns us about long positions in small/mid caps is that it wouldn’t be consistent with where we are in the US macro cycle. We’d expect smalls/mids to outperform in the initial phases of a recovery after a slowdown – not in the late stages (which is where we’d surmise we are right now). The appeal of equal weight gauges is that they are less dependent on the phase of the cycle and more of a pure play on concentration risk.

From a sector standpoint, a shift toward equal weight also increases exposure to areas we are constructive on — such as materials and healthcare — while reducing overweight exposure to tech and consumer discretionary.

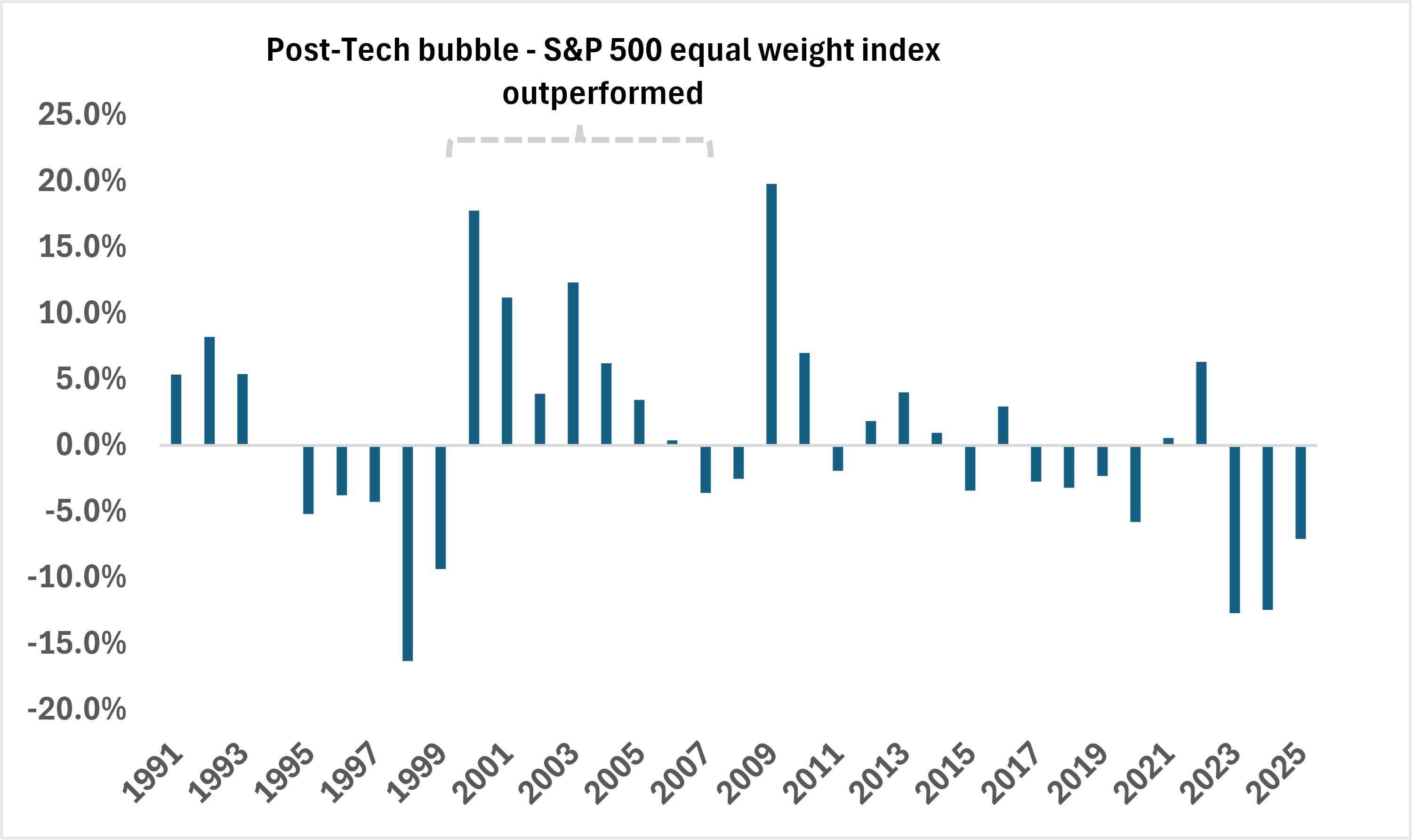

In terms of historical precedent, Chart 2 helps frame expectations. In the years following the tech bubble, earnings momentum broadened, market leadership expanded, and US equal‑weight indices outperformed. All of this aligns well with a key theme we’ve highlighted in our recent work: broader participation and leadership in US equities in 2026.

Chart 2 – S&P 500: Equal weight index returns – Market cap weighted

Portfolio Strategy

i.) President Trump has nominated former Fed board member Kevin Warsh to lead the institution once Chair Powell’s term ends in May. Once he’s approved by the Senate, he’s expected to take Stephen Miran’s seat at FOMC meetings going forward.

There are a few things to understand about this pick:

- Out of the many candidates who were in the running, Warsh is one of the few that we’d say is “orthodox enough” for the role.

- He’s firmly in the “AI is a disinflationary force” camp as well. In growth accounting terms, this means that he sees AI helping to expand potential growth (or ‘y-star’) by enough that incoming growth shouldn’t be inflationary. He’s likely to lean on that to drive the narrative for lower rates.

- Many have picked up on his prior comments pushing for a smaller Fed balance sheet and interpreted this to mean he’s hawkish. But that’s not the case – in an ample reserves regime, you can shrink the balance sheet (via passive QT) while still cutting rates. The only constraint here would be volatility in the repo markets (i.e – the plumbing would be disrupted materially).

It’s unlikely that Warsh will push for the Fed to trim its balance sheet. Doing so would likely bring him into conflict with the Trump administration’s objectives. Having said that, he is likely to push for cuts – which means that his views aren’t likely to shift whatever is priced into the OIS curve by much.

ii.) Gold and silver remain under a fair bit of pressure to start the week. While both trades remain crowded, we’d expect some degree of consolidation in the coming sessions. The same is also true for the USD.

We don’t think the selection of Warsh to run the Fed is as hawkish as the market does (and ergo, not as supportive for the USD). Also, among the reasons to be constructive on metals this year was the unpredictable geopolitical backdrop and that hasn’t changed much over the past week.

iii.) There’s a fair bit of meaningful data this week. We’re closely monitoring the following:

In the US: ISM manufacturing (Mon), JOLTS (Tues), ISM services (Wed), Claims data (Thurs) and Nonfarm payrolls (Fri).

For payrolls, we’re placing more of an emphasis on the unemployment rate and labor force participation rate as opposed to the headline.

Also, the US Treasury will be releasing its quarterly refunding statement and related auction schedules. These are important releases that give us a feel for projected bill/note issuance sizes and timing. The general feel is that the Treasury will maintain auction sizes and keep relying on bill issuance to meet cash needs.

In Canada: BoC Governor Macklem speaks on Thursday, Labour force survey (Fri).

iv.) Central bank meetings this week:

- In Australia, there are a fair amount of forecasters that expect the RBA to hike policy rates by 25bps Monday evening.

- On Thursday, both the ECB and the BoE are expected to keep policy rates on hold.

- Meanwhile, in India, the RBI is also expected to maintain its policy repurchase rate at 5.25% this Thursday.

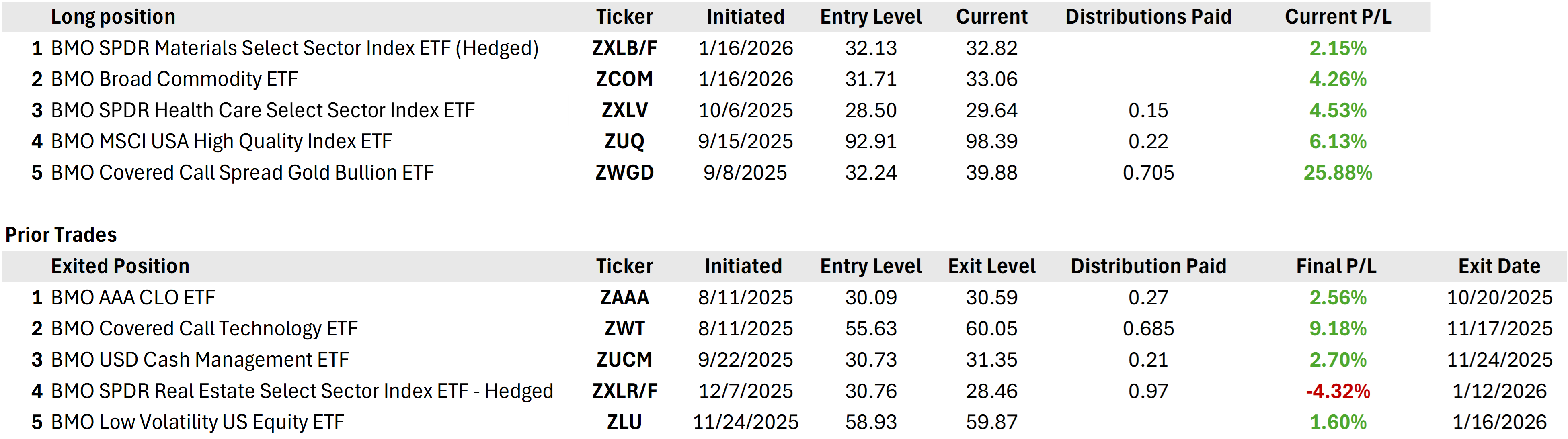

Book of Trades

Balanced Portfolio

Current Weight |

Benchmark |

||

Fixed Income |

20% |

30% |

Underweight |

|

5% |

15% |

|

|

15% |

15% |

|

Equities |

64% |

60% |

Overweight |

|

25% |

25% |

|

|

18% |

25% |

|

|

21% |

10% |

|

Alts/Hybrids |

16% |

10% |

Overweight |

Asset Class |

View |

Notes |

Equities |

Slightly bullish |

|

Fixed Income |

Slightly bearish |

|

Alternatives |

Bullish |

|

FX |

Slight bearish USD |

|