Weekly Basis Points - Iran Conflict: Six Points to Make

March 01, 2026

Summary points:

- Energy market disruption: Strait of Hormuz traffic has collapsed, insurers have pulled coverage, and oil majors have halted operations — setting up the potential for a multi‑week supply shock.

- If crude holds near $95 – 100, inflation risks rise: Sustained price increases could add ~0.7 – 1.3 ppts to US/Canada CPI, limiting room for rate cuts and pushing breakevens and long yields higher.

- Portfolio impact favours real assets: Energy, materials, and commodity‑linked regions (Canada, LatAm) should outperform, while transportation, consumer discretionary, and major oil importers face headwinds.

1.) Here is what we know so far…

- The US and Israel have launched attacks against Iran with one of the implied objectives being a regime change. So far, the attacks have been aerial, with no boots on the ground just yet.

- Among the casualties so far, Iran’s supreme leader Ayatollah Khamanei as well as other leaders from the Revolutionary Guard. Iran has responded to the strikes by targeting other US allies in the region. Meanwhile, Trump has indicated that he is willing to talk to the new Iranian leadership.

- Activity through the Strait of Hormuz is basically nil at this point. Shipping insurers have cancelled current policies have raised coverage prices by over 50% in response to developments over the weekend.

- Oil majors and trading houses have also suspended ship operations in the region. Several Middle East ports have closed due to damage.

2.) Key questions we need the answers to…

We’re going to keep our comments focused on what the conflict will mean for the economy and markets. That’s not to say that we should look past the human costs, but as market strategists, those are beyond the scope of what we can speak on here.

a.) What happens to leadership in Iran now? With Khamanei and other senior leaders gone, there is now a leadership vacuum in Iran. Prior experience (Iraq, Libya, Egypt) tells us that the most likely outcome in the short-term is instability – which seldom works out to a ‘western-friendly’ democracy over the long-term.

b.) How long will this conflict go on for? Trump casually threw out an estimate of four weeks, but regime changes are rarely clean and orderly. What’s more is that the removal of Khamanei doesn’t automatically guarantee a ‘Venezuela-esque’ situation whereby the new leadership is eager to work with the US.

Nevertheless, the longer this conflict goes on for, the longer that activity through Hormuz will be slowed considerably. That is important given that over 20% of the world’s petroleum supply and a considerable portion of LNG flow through the strait. Additionally, it means that insurance premiums will remain elevated – and will pass through to end-user costs/inflation.

Without a quick end to this conflict, the potential for a meaningful energy shock is there. That matters for non-energy commodities as well given that transport costs should rise as well.

3.) What does this mean for the energy markets? There are several historical parallels we can use to frame what could come next.

i.) The 1973 oil embargo: Given that Iran is now isolated geopolitically in the Middle East, we don’t think this comparison makes sense. That episode required coordination from other OPEC members while US production was less than half of what it is today. Instead, OPEC+ is going to coordinate by increasing production to alleviate price pressures.

ii.) The Iranian Revolution of 1979: Total production of Iranian petroleum went from 5,600−5,800 Mb/d to 1,380−1,662 Mb/d after the revolution. Meanwhile, oil prices rose by 162% over 1979/80 and was a direct cause for the global recession around that time.

The key here was that price increases were sustained as few other producers could increase output as an offset to lost Iranian production. That’s a bit different from where we are today.

iii.) The Iraq War of 2003: Oil prices rose initially – but then fell towards the end of that spring. The reason being that production and supply channels were not meaningfully impaired by the conflict.

iv.) Libya’s collapse in 2011: The civil war in Libya began in early 2011 and the country remains in crisis to this day. As Libyan production dropped in 2011, energy prices rose from $95 to over $125 in the months that followed. Production has recovered since then, but not to the levels from before the civil war.

Our own view is that the current market setup is somewhere between ii) and iv). That still portends to a shift higher in crude prices in the near-term, but we expect that production increases from OPEC+ and non-OPEC countries will cap rallies. If the conflict extends to a few months, it’s likely that prices could easily breach $95-100 per barrel for Brent crude. That would represent a 60-67% rally from the January lows.

4.) What would that mean for the US/Canadian economies? The easy answer here is that a sustained rise in oil/commodity prices will increase input costs for firms. Given the existing pressure on margins from tariffs, the increase in commodity prices will likely be passed on to end-consumers.

If oil prices move to $100 and stay there for the coming quarters…

- The contribution to headline US CPI (from indirect and direct channels) is likely to be 0.7% to 1.0% over the next 12 months. That would take CPI uncomfortably close to 4% y/y with core CPI likely to follow if oil prices don’t fall after a few months.

- The impact on Canadian CPI is expected to be slightly higher (0.9-1.3%) which would take headline CPI close to 3.5%.

In both cases, the Fed and the BoC are less likely to ease further this year. That would especially be the case if inflation expectations were impacted.

5.) What does this mean for broader markets? A sustained increase in crude oil prices will have implications for broad markets.

Rates: In such a scenario, we’d expect fixed income to remain slightly on the defensive for both the US and Canada. At the front-end, markets will pare expectations for easing this year (see point 4 above). In the long end, we’d expect to see inflation breakevens extend higher.

Using the relationship from 2011 (during the Libyan civil war), a move to $95-100 oil would imply a ballpark estimate for US 10yr breakevens to rally by 16.5bps. Assuming no change in 10-year real rates, that would mean US 10s move to 4.17%. Using the same approach, we come up with an equilibrium estimate for CAD 10s of 3.30%. Again, these are equilibrium estimates not point-level targets.

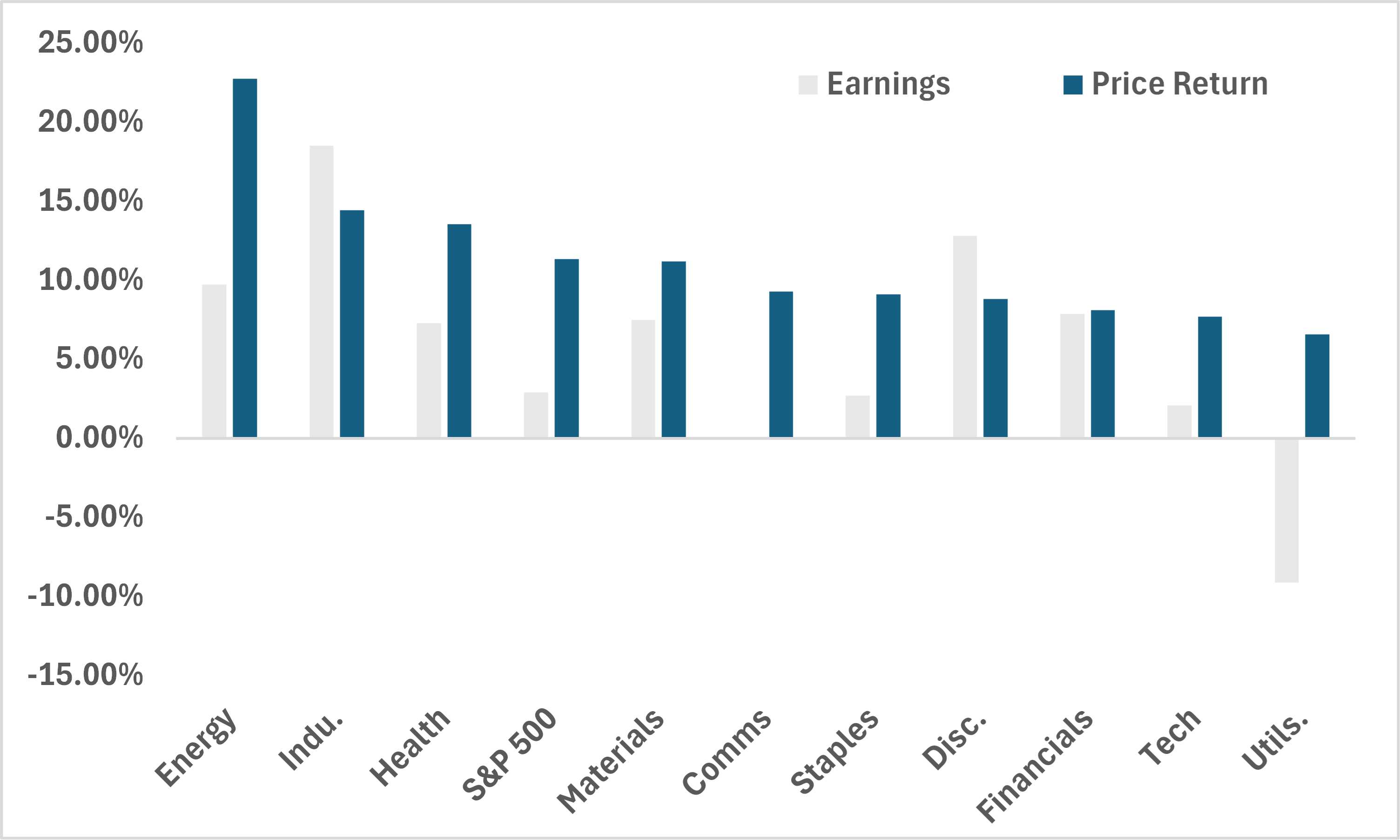

Equities: By sector, energy should continue to perform given the geopolitical premium (the early 2011 experience backs this up – see Chart 1). Within the sector, it’s the integrated majors and upstream producers that should do well given the high beta to oil prices. Materials should also benefit as transport costs for other commodities are likely to be passed on.

On the other hand, expect industrials (especially airlines) and consumer discretionary to lag. The latter has already underperformed year-to-date as well.

Chart 1 – Change in sector performance and earnings during 2011 Libya conflict

Source: Bloomberg, BMO GAM

By region, there’s a strong case to be made that commodity exporters like Canada and Latam should do well for a few reasons. For one, commodity exporters benefit from increased revenues whenever prices rise. Second, this weekend’s actions are likely to lead to further outflows from the US to relatively ‘underweight’ markets. For instance, energy and materials account for 38% of the weight for the TSX, 28% for the MSCI Latam Index, and only around 5% for the S&P 500.

Among the underperformers, watch for petroleum importers (India, South Korea and Japan) to be adversely impacted.

Commodities: As we type this, Asian markets are just starting to open and most commodities are up. Gold and silver are both up by over 1.5% while prompt Brent and WTI are up by over 8% from Friday’s close.

We expect base metals (notably aluminum) and agriculture (fertilizer) prices to remain bid as well. Closure of the Strait impacts both commodity groups materially.

FX: Currently, the USD is bid on haven appeal. Expect major oil exporters (NOK, CAD) to remain low beta while the JPY, EUR and INR remain vulnerable going forward.

6.) Final thoughts: There are a lot of unknowns right now and the situation is changing by the hour.

For us, the key unknown is whether this conflict will extend beyond a month and what that means for the shipping through the Strait of Hormuz. All of the above estimates are predicated on a conflict that lasts beyond a month with shipping through the Strait remaining contained.

We’re expecting some near-term defensiveness in risk assets as the initial shock is priced in. But we’re still of the mind that investors should remain invested – especially in commodity-sensitive areas. We are not changing our macro regime call for now but do acknowledge that this weekend’s events could truncate the time we’re in it.

Below are ETFs to consider as we navigate through this time:

- ZCOM

- ZGLD and ZWGD

- ZMT

Portfolio Strategy

a.) US nonfarms: Outside of the situation in the Middle East, this week’s release of US nonfarms (for February) will be the most meaningful input into markets. The January number was very constructive, but highly concentrated on health care jobs. For us, continued progress on the unemployment rate is the most important output to watch for in the report.

b.) Eurozone date: It’s a big for data on the other side of the Atlantic. The first estimate for February CPI is out on Tuesday morning while business sentiment data (PMIs) will be released on Wednesday.

c.) SaaS: Alongside the many other things to watch for, there is still a degree of fragility in the software space. However, pay attention to how the market treats the news over the weekend that the Trump administration has signed a deal with OpenAI to use its models in the US defense agency’s classified network (with “safeguards”). This comes after a recent spat between the White House and Anthropic.

Book of Trades

Asset views:

Equities |

Overweight Earnings remains solid, but broader participation remains the play for now. In the US, we like value and equal weight strategies as tactical plays for now with a preference for quality over the long-term. |

Fixed Income |

Underweight We prefer spread product exposure (IG credit) to sovereign fixed income. |

Alternatives |

Overweight A more fractured trade backdrop lead to front-loading of commodity demand from importers. We still see upside for energy and metals for now. As a region, this should benefit Latin America. |

Currency: |

Neutral We are neutral on the US dollar in the near-term (1−2 months), and bearish over the long-term. Increased hedging activity on foreign USD exposure is the primary reason for our long-term view. |