Weekly Basis Points - SpaceX: Too Large for the Rules

June 07, 2026

Summary points:

- SpaceX may be too large to ignore for some index providers — but structural rules keep it out of the S&P 500, delaying one of the most powerful sources of passive “buy-and-hold” demand.

- A $1.7T IPO with ~4% float creates a perfect setup for volatility, where even small shifts in demand can drive outsized price moves.

- The result: more two-way price action and noisier price discovery, as retail and active flows dominate until passive inclusion becomes viable.

This Friday, SpaceX is set to debut as one of the largest companies in the world. And yet, structural constraints will mean it may be shut out of the most important equity index in the world – the S&P 500.

Of course, this is not your typical mega-cap IPO. For one, there is the issue of size. At a targeted valuation of US$1.77trln, SpaceX is already a top 10 US company with a higher market capitalization than Meta Platforms (Facebook) and Tesla.

Second, the initial float size is incredibly small relative to its market cap. For instance, its IPO is expected to raise at least US$75 billion, which amounts to an extremely low float of 4.2% of total shares. That would violate pre-existing rules for many index providers.

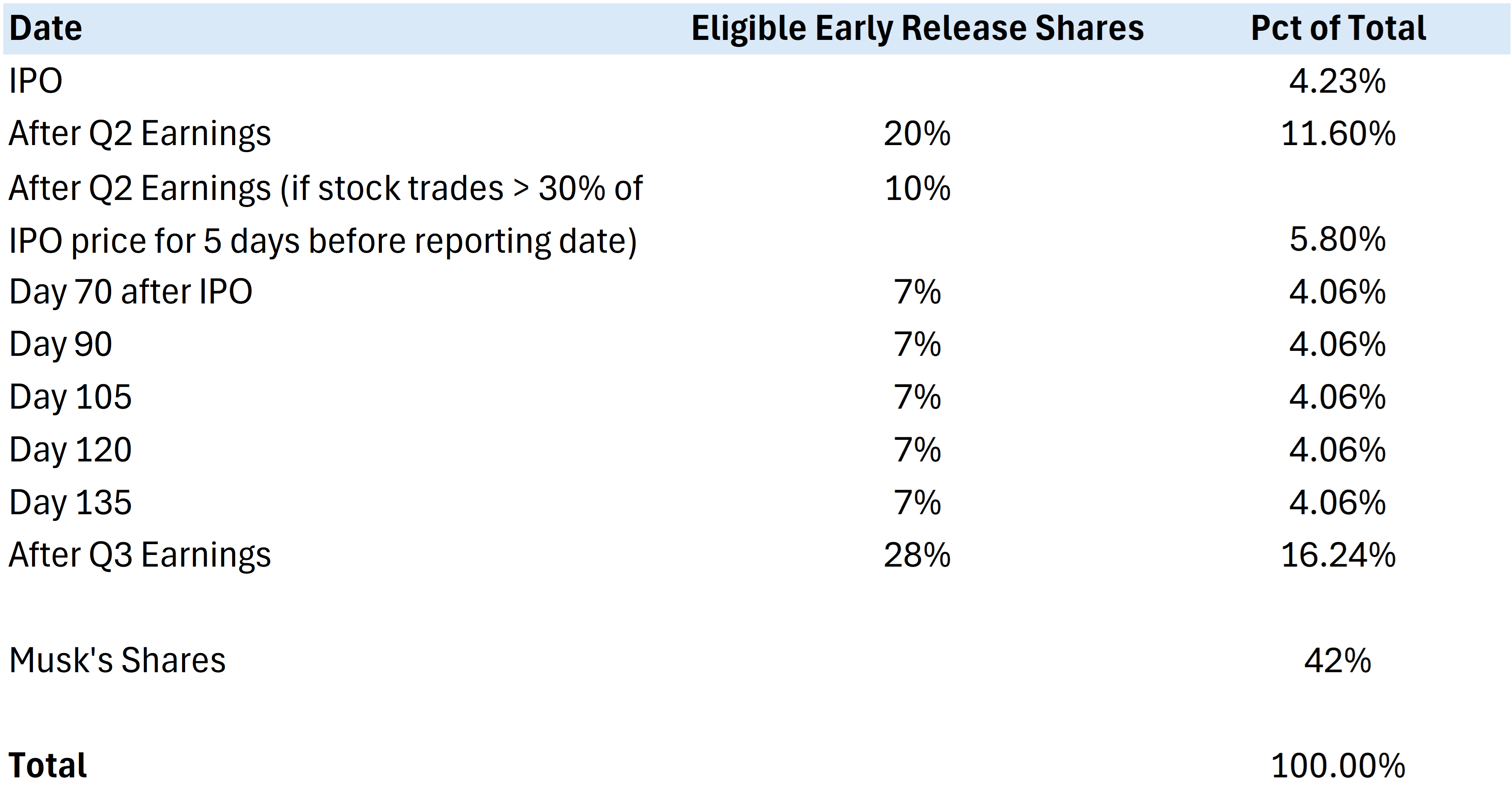

Complicating things is that the staggered manner of its share releases is also very complicated. All pre-IPO shares will be subject to a 180-day lockup – with the exception of founder shares and a select group of significant investors (who are subject to a 366-day lockup). All of the 180-day lockups and some of the 366-day lockups could classify for ‘early release’ depending on price/time milestones as shown in Table 1.

Table 1 – SpaceX Lockup Release Timeline and Key Supply Events

Third, the company had negative earnings in its most recent quarter and for fiscal year 2025. That’s at odds with inclusion rules for a particular index provider (S&P Dow Jones Indices). Indeed, there is already concern out there that by allowing an unprofitable company onto indices would violate the spirit of capital allocation to profitable public enterprises that index providers adhere to.

But for many index providers, SpaceX is “too large to ignore”. If the primary goal of an index provider is to represent and measure the performance of a specific market or sector, not including SpaceX would mean a divide between the benchmark index and the investible market. That’s why a few of them have introduced rule changes recently to fast-track inclusion of mega-cap names. To summarize a few of them:

- Nasdaq: Large companies will be eligible for index inclusion after the 15th day of trading. The 10% minimum float rule is replaced by a float adjustment factor that is capped at 3x for floats that are less than 33.3% of market capitalization.

- FTSE Russell: Large companies to be eligible after the 5th day of trading. The index weight is to be determined by float shares.

- CRSP: Large companies are eligible to be added after 5 days of trading.

However, the major index provider that has announced that it won’t be changing its existing rules is the S&P Dow Jones Indices (or S&P DJI). That means that there will be no change for eligibility criteria including financial viability screens (SpaceX has to turn a profit over four quarters), seasoning period (at least 12 months of trading history on an exchange) and on minimum investible weight factor (at least 10% of the company’s shares must be freely tradable public float). This is a big deal because it’ll affect potential inclusion into notable indices such as the S&P 500.

According to the current rules, SpaceX wouldn’t qualify for S&P 500 inclusion until at least June 2027 (assuming its profitable by then). And that matters given the amount of the assets that are indexed to the S&P 500 was estimated to be around US$13trln at end-2024 (think ETFs, mutual funds, other exchange traded products and institutional mandates). We don’t have an estimate for end-2025 yet, but some rough back-of-the-envelope math implies that number is in the US$15-16trln range.

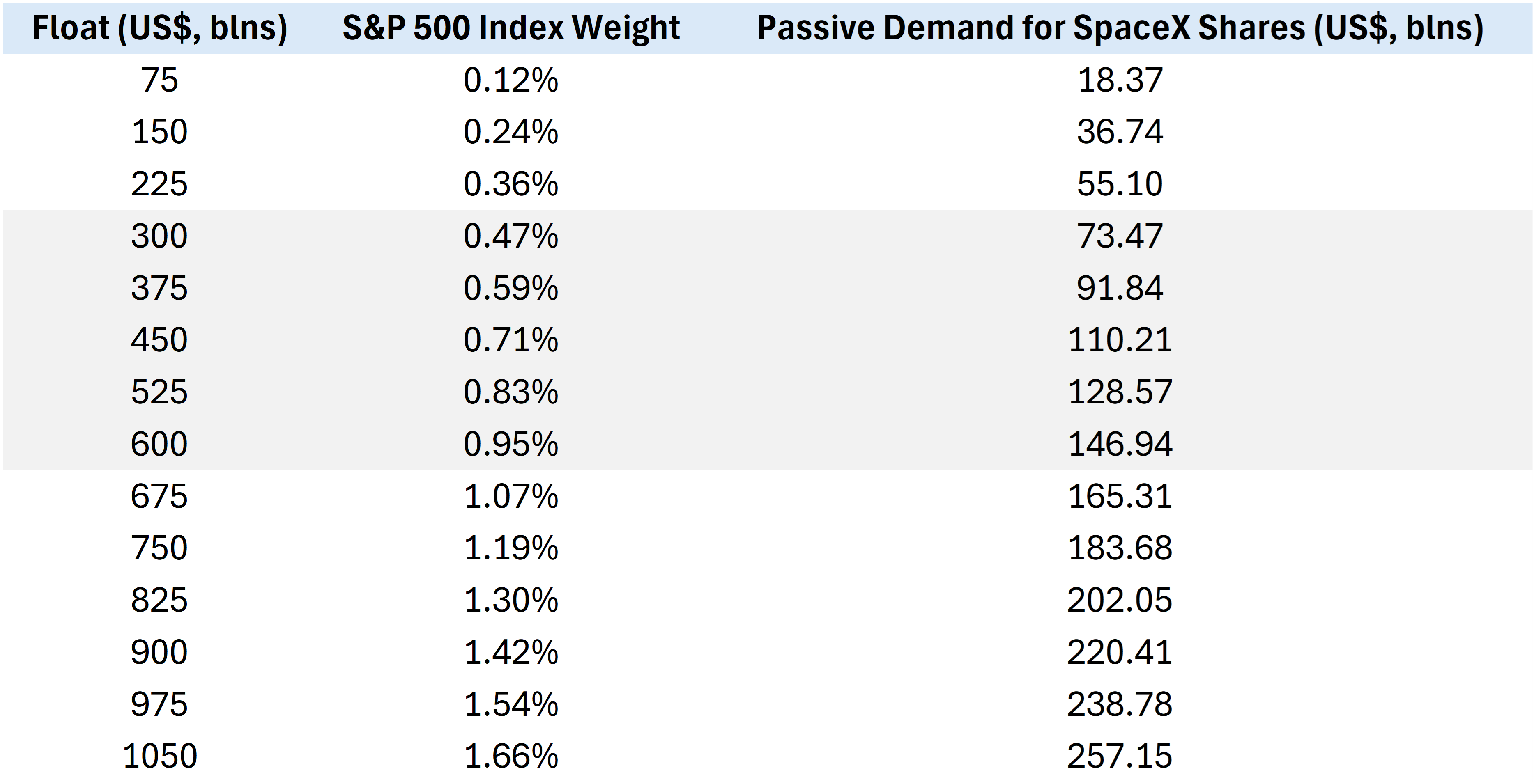

We’ve constructed Table 2 that shows how much inclusion could impact SpaceX shares over time. Since the S&P 500 weighs by the ‘float adjusted’ market cap, that is the key variable that we’d need to account for. Remember that as lockups expire and more shares enter the float, the index weight will change as well. As an example from Table 2, assuming that this gauge reaches US$900bln over the coming six months, that implies SpaceX would have benefitted from US$220bln in ‘forced demand’ from passive index trackers. That type of demand would be an easy stabilizer to post-IPO or lockup release price volatility.

Table 2 – Estimated S&P 500 Index Weights and Passive Demand for SpaceX Had it Been Included

**Shaded region indicates base case range for next 12 months

Source: BMO GAM

What are the implications for this?

- First, a thin float will already mean that a small shift in demand (post-IPO) could impact prices more easily. For now, the Nasdaq-tracking ETFs are the most immediate and meaningful ‘forced buy’ catalysts.

- Second, the lack of guaranteed inclusion into the S&P 500 will mean more two-way volatility – especially during lockup expiration dates between September and December. For instance, there is more room in the shareholder base for retail and speculative buyers as opposed to ‘mechanical buy and holds’ (passive index trackers) – which makes price discovery noisier.

- Third, this will still impact ETFs that track the S&P 500 (like ZSP and ZUE). For instance, index rebalancing to include SpaceX in the Nasdaq 100 and MSCI US indices also means some ‘forced selling’ of shares (especially Mag7). That pressure could also migrate to pressure on the S&P 500 – not least since Mag7 shares account for a meaningful weight in that index. All told, this means that ZSP and ZUE investors might not be as insulated as they think from SpaceX-related rebalancing effects – even without direct inclusion in the S&P 500.

And on a final note, this will change the calculus for future mega-cap IPOs from here. The SpaceX experience will inform how companies like Anthropic and OpenAI structure their IPOs going forward. Both firms are loss-making but will likely debut at valuations that place them in the top 10 US company territory. However, both will also face the same S&P DJI eligibility constraints that are keeping SpaceX out of the index. If inclusion in the S&P 500 is a strategic objective, that could mean a focus on accelerating the path to profitability ahead of the IPO or structuring the initial offering with a larger float. Failure to do so could mean the loss of the stabilization bid – which is worth tens of billions in demand.

Portfolio Strategy

The nonfarms print wasn’t too kind for broad risk last Friday. The S&P 500 finished the week lower for the first time since March, while US yields pushed higher (the 2s10s curve bear flattened). At the same time, the USD strengthened aggressively on a trade-weighted basis – pushing USD/CAD to the 1.3950 area.

The stronger USD also wreaked havoc on our commodities positions, with gold effectively wiping out all year-to-date gains.

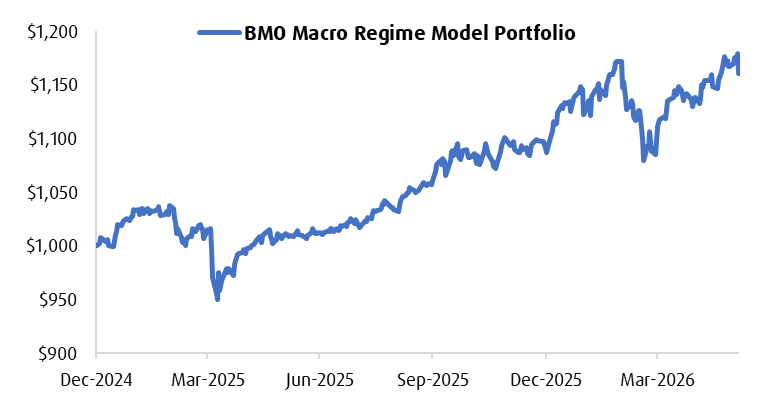

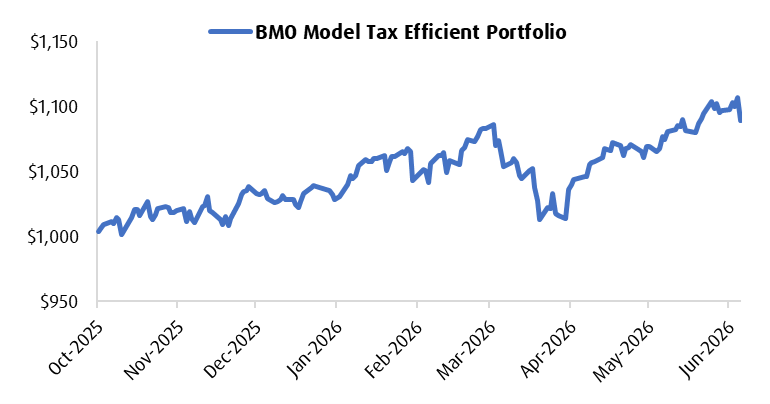

The May nonfarms print implies that the transition in macro regime from reflation to mild stagflation will take some time to play out. Our Macro Regime portfolio model is still up 6.77% year-to-date while the Tax Efficient model portfolio is up 5.94% over that same time span.

Chart 1 – BMO Macro Regime Model Performance

Chart 2 – BMO Tax Efficient Portfolio

Source: BMO GAM

a.) BoC Thoughts: The May edition of the labour force survey was substantially strong – with the Canadian economy adding close to 88,000 jobs on the month while the unemployment rate dropped to 6.6%. Having said that, there are some notable caveats to the print:

- We were long overdue for a rebound in full-time jobs (which increased +154k on the month). This is largely mean reversion at work.

- The most recent core CPI prints (for April) came in on the soft side of expectations while oil prices have moved lower over the past few weeks.

- Hours worked are only slightly positive on a year-over-year basis – which tells us that real activity is likely muted as well over that time frame.

While the number tells us that recession talks are premature, we’d still expect the BoC to stick to a more cautious and neutral tone. That will mark a departure from the tone in April (remember Macklem’s comment about consecutive hikes being in play if oil remained elevated?), which should mean some support for the front-end of the CAD curve (yields moving lower). It should also mean that USD/CAD moves higher.

b.) US CPI: The contribution from gasoline prices should be the main driver for the headline but watch for passthrough to other categories in the core basket (including airfares). Additionally, we could see uptick in the price for AI-related items due to shortages.

The street is expecting the headline to come in at +0.5% m/m (or +4.2% y/y) while the core is expected to come in at 0.3% m/m (or +2.9% y/y). Indeed, those prints should amplify price action seen following the release of last Friday’s nonfarms figures – with more tightening priced into the USD OIS curve for this year.

c.) SpaceX IPO: Friday is the big day.

We covered the topic in the lead article above – but watch for inclusion into key indices over the coming weeks:

- CRSP: June 19

- FTSE Russell: June 19

- MSCI USA: Around June 26-29

- Nasdaq 100: July 2-6

- S&P 500: Possibly June 2027

d.) Other data to watch for:

- China: CPI/PPI for May (Tuesday eve)

- Eurozone: ECB decision on Thursday (a rate hike is a done deal at this point, watch for guidance on path forward)

- US: PPI (May) + Initial jobless claims (both on Thursday), Michigan surveys (Friday)

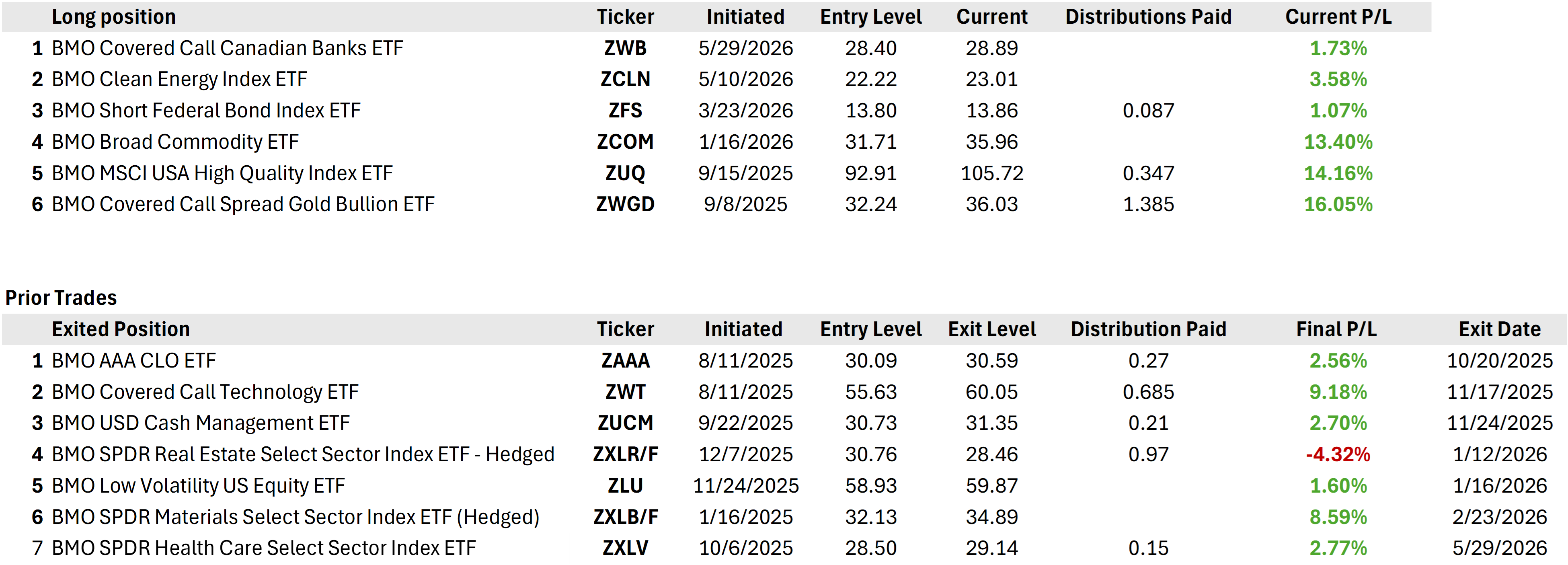

e.) Book of Trades

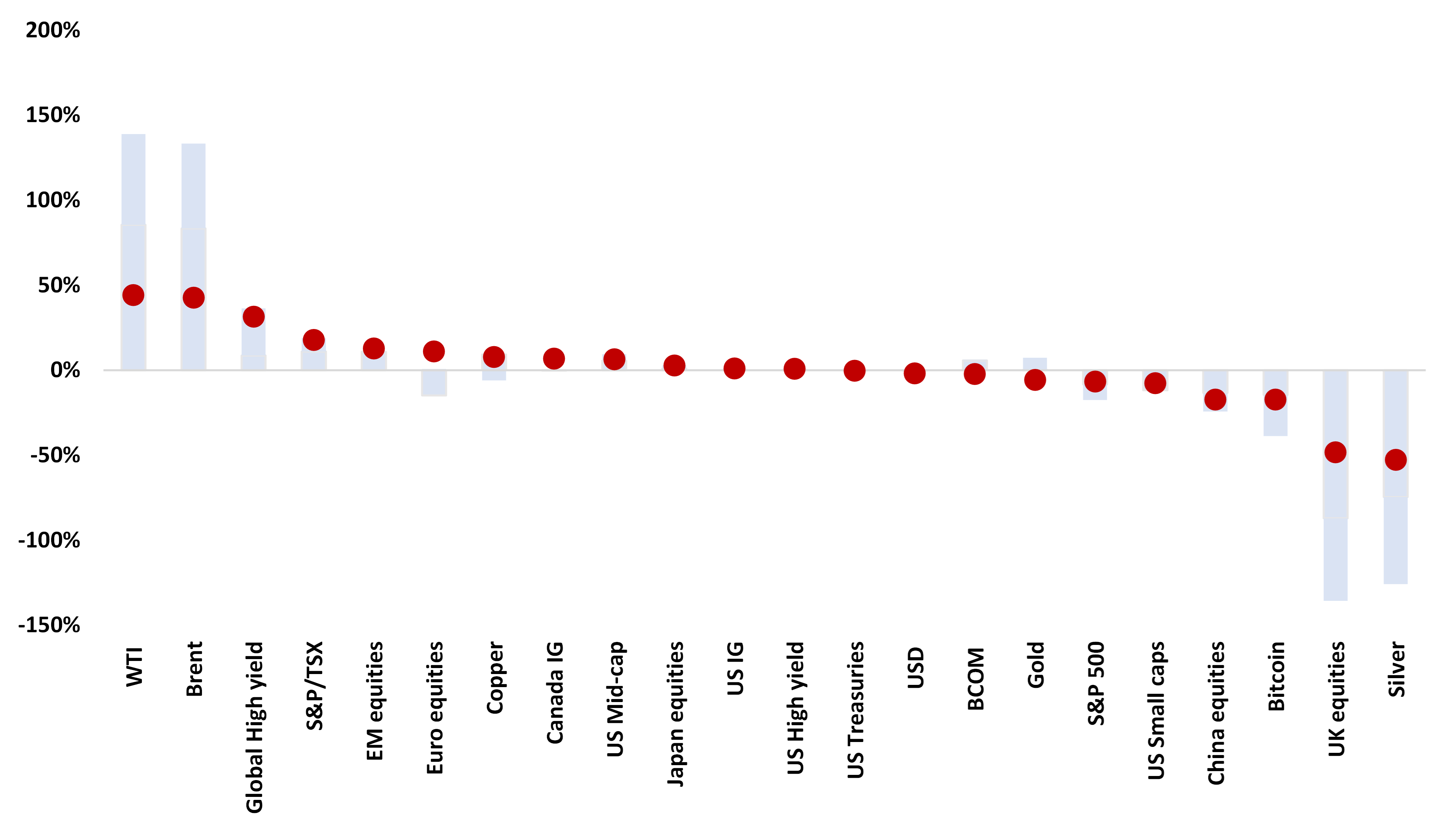

f.) Asset Performance (Year-to-Date)

Source: BMO GAM, Bloomberg