Weekly Basis Points - Taking Stock of Recent Data and Events

February 23, 2026

Key summary points:

- US data shows solid but uneven momentum: Q4 GDP was stronger than the headline implies once shutdown effects are removed, but inflation progress has stalled with Core PCE stuck near 3% and savings rates falling.

- Thoughts on the IEEPA ruling: The Supreme Court’s IEEPA decision will increase uncertainty at the margin but has limited market impact over the long-term.

- Positioning: We like being defensive in the US, long international equities, and broad commodities. We’re neutral on the USD in the near-term and would use rallies to layer into additional hedges.

We’re going to eschew a thematic write-up this week. Instead, we’re going to provide some quick thoughts on recent data points and market developments and what it means for our framing going forward.

i.) On the US Q4 GDP: Ignore the noise, this was a solid print.

The disappointment from Friday’s reading (+1.4% vs +3.0% expected) was all about the government shutdown in the early part of the quarter. Outside of that, household consumption held up as expected – most notably spending on healthcare – alongside business investment and net exports. With respect to AI, we estimate that proxies contributed about 0.5% to the overall print, which was above the contribution for Q3.

Of course, it’s not the 3% that everyone was expecting. But if you strip out the negative contribution from the government shutdown, growth was still above trend.

ii.) On the US PCE prints: This is becoming a bit of a problem.

Core PCE is now at 3.0% y/y while the PCE deflator is now running at 2.9% y/y – a rate it hasn’t tracked since March 2024.

On top of that, the savings rate continues to drop which is a bit inconsistent with the narratives in the media about delinquencies rising, etc.

iii.) On the US Supreme Court IEEPA ruling: A pick-up in short-term uncertainty is constructive for precious metals, but over the long-term, this isn’t as market relevant as you might think.

The Supreme Court struck down IEEPA because it ruled that the President overstepped by implementing tariffs without congressional authorization – violating the spirit of the Act. However, the ruling didn’t undermine the potential use of other Acts (122, 201, 232, 301, etc) for tariffs. Trump has announced that he will impose a universal 15% tariff under Section 122 – which doesn’t require Congressional approval initially but will once 150 days has passed. What’s more is that the US Trade Rep has announced numerous mandatory investigations as part of the process for tariffs under Section 301.

For Canada, this ruling doesn’t apply to the tariffs that matter – on autos, steel, lumber, etc. However, USMCA-compliant goods are still exempt from the tariffs announced under Section 122. Also, there is a strong case to be made that this does increases Canada’s leverage in upcoming USMCA talks as it won’t be automatic that a 35% tariff will apply if the US elects to withdraw from the agreement.

With respect to the revenues lost from IEEPA – they’re too small to matter in the grand scheme of things. As such, we don’t expect a large enough sell-off in rates to stir the market from this alone.

What do the above mean for our view?

Right now, there’s little reason to shift from our call that the current backdrop is indicative of strong but uneven growth and slow disinflation across several economies.

For the US, there is a bit more concern on the slower progress on the inflation front. That means that the market could continue to push out expectations of the next cut or curb the total amount of expected stimulus. The latter would mean a higher terminal rate and front-end yields – which would also pose risks to the equities market by extension.

The other risk we’re watching is with productivity benefits from AI. The big risk to monitor into Q1 is whether the productivity benefits realized from AI-related investment are concentrated rather than distributed. If it’s the former, then there is a good chance we’re further along the late-cycle phase than we think.

See below for our asset class views, but here is a quick snapshot with a bit more granularity:

- Equities: Stay long international and look to remain a bit defensive/late-stage in the US.

- Fixed income (sovereign): No strong view here as rates should back up in the front-end a bit more.

- Credit: Yield is attractive here and we expect demand to remain strong. Public sector spreads should remain tight as private credit absorbs most of the risk in this space.

- Commodities: Dips in metals will be bought while energy momentum is all about geopolitics rather than fundamentals.

- Currencies: We’re neutral on the USD tactically and bearish strategically. The market is too short the USD right now.

Portfolio Strategy

Macro Regime Call

Current macro regime: ‘Fractured Expansion’ - strong but uneven growth (late cycle) + slow disinflation

Confidence: Medium | Horizon: 3-6 months

Policy regime: Neutral, but easing at the margin (monetary and fiscal)

Market regime: Fragile, but selectively risk supportive

Risks to call:

- Rise in inflation across DM that leads to re-tightening policy reaction functions.

- Benefits from AI-driven productivity are concentrated rather than distributed.

Notes for this week

a.) Oil markets: There is a lot of focus on oil prices right now given the situation between the US and Iran. Our own thinking on this is that there is a fair bit of two-way risk here that will keep traders busy (geopolitical risk premium is doing a lot of the driving when it comes to oil prices right now). For longer-term investors – the fundamentals for the energy sector are still too iffy.

b.) In terms of key data points this week…

- Canada Dec GDP + Q4 GDP (Friday): There is a very good chance that the Q4 print comes in slightly negative – which would be below the 0% that the BoC penciled in as a projection in its January MPR. Household consumption wasn’t that strong in Q4 and residential investment was also likely a net drag. However, if there is an indication that weakness is spilling into Q1 2026 (pay attention to the January flash estimate), then watch for CAD swaps to start pricing in additional BoC cuts more forcefully.

- Trump’s State of the Union Address is on Tuesday night. Traditionally, this is a great spot for the President to lay out the agenda for the coming year – but we already know what Trump is thinking on trade, tariffs, and the economy from prior comments anyway.

- US Consumer confidence for January is out on Tuesday morning. Despite a solid track for the economy and earnings, confidence continues to plummet amongst households. This tension is playing out in the market as well.

- Nvidia earnings are out on Wednesday. This has become an important event for the macro over time given how concentrated US markets have become.

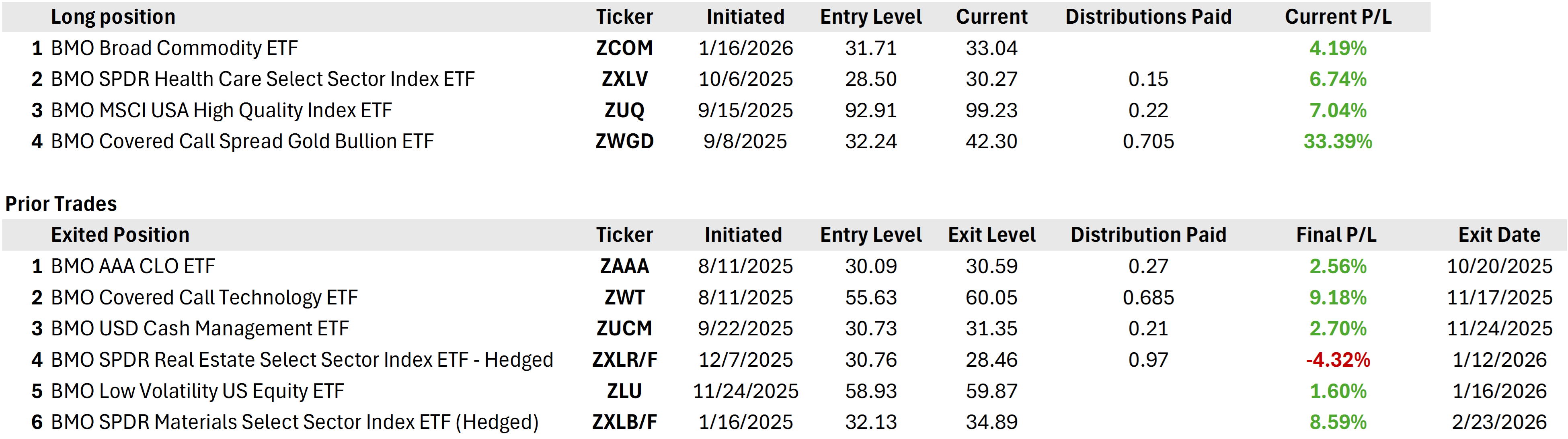

Book of Trades

We’re taking profit on our long ZXLB/F position for a gain of +8.59%. We initiated the trade on January 16th.

Asset views:

|

Equities |

Overweight Earnings remains solid, but broader participation remains the play for now. In the US, we like value and equal weight strategies as tactical plays for now with a preference for quality over the long-term. |

|

Fixed Income |

Underweight We prefer spread product exposure (IG credit) to sovereign fixed income. |

|

Alternatives |

Overweight A more fractured trade backdrop lead to front-loading of commodity demand from importers. We still see upside for energy and metals for now. As a region, this should benefit Latin America. |

|

Currency: |

Neutral We are neutral on the US dollar in the near-term (1−2 months), and bearish over the long-term. Increased hedging activity on foreign USD exposure is the primary reason for our long-term view. |