Weekly Basis Points - The Front-End of the Curve is Losing its Mind

March 22, 2026

- Global central banks are signaling caution on rising energy prices, but their willingness to “look through” the shock assumes a short, temporary disruption in the Strait of Hormuz — an assumption that now looks increasingly fragile.

- Markets have rapidly repriced front‑end rates, with several central banks expected to hike; however, the Bank of Canada’s repricing looks excessive given Canada’s softer growth backdrop, rising slack, and weaker inflation passthrough dynamics.

- The BoC can likely wait out the oil shock, implying the CAD front end has overshot; this creates tactical value in going long short‑ and mid‑term federal bond exposures such as ZPS, ZFS, ZAG, and ZDB, with a long ZFS position added.

Nearly all the major developed market central banks had the chance to speak last week on how they are framing the rise in energy prices. All of them said the same thing – that higher crude prices meant near-term risks had risen (to the upside for inflation and to the downside for growth). Additionally, the common theme was that central banks are likely to ‘look past’ the rise in energy prices for now, but that is contingent on how long the flow of crude oil and liquified natural gas supplies remain disrupted in the Strait of Hormuz.

That last point is salient, because it implies that central banks are still expecting disruption to be temporary and the conflict in the Middle East to be a short one. But as the focus of the conflict expands from ‘how long Hormuz will be shut’ to ‘how much critical damage has been done to infrastructure in the region’, it’s becoming harder to envisage a short-term disruption as the base case scenario. The implication here is that higher energy prices should creep in to forward-looking expectations for inflation in the private sector and lead to a change in spending/investment plans – something that no central bank should be quick to look past.

This is the most proximate reason for why we’ve seen the front-end of the yield curve come under enormous pressure over the past week. As the risks of ‘stickier’ inflation rise, markets have been quick to reprice expectations for the central bank. In many cases, that means that the odds of rate hikes increase (the ECB, BoE, BoJ and notably, the BoC), while in other cases it means that prior rate cuts are priced out (the Fed).

However, for some central banks, we do take umbrage with how the market is interpreting things. That is particularly true for the Bank of Canada.

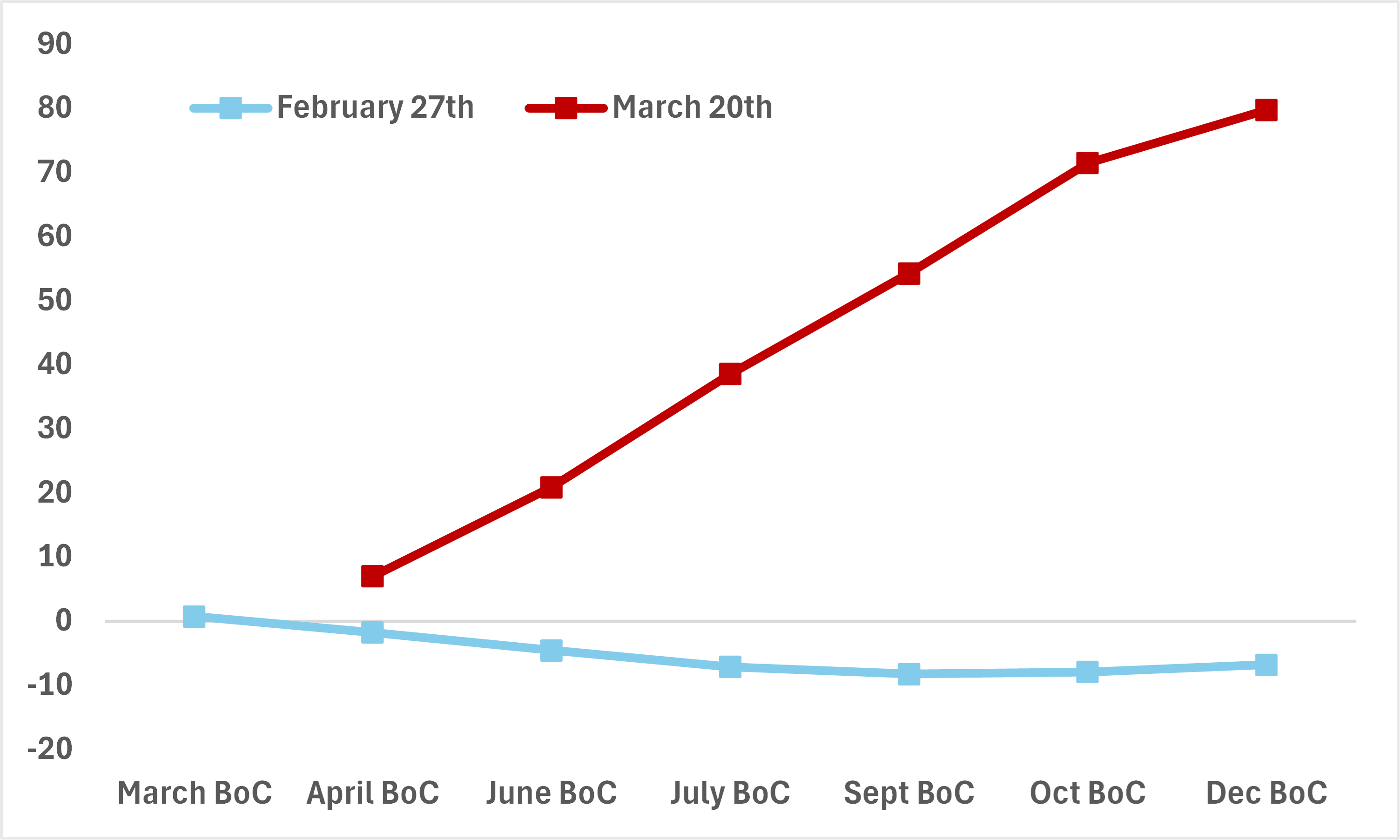

As of the end of last week, the CAD swaps market now expects the Bank to have tightened by 36bps as of the July meeting with two more to follow before the year is out (roughly 80bps is priced by the end of 2026). As a result, the 2-year GoC yield has risen by 27bps over the past week and 67bps since the conflict began. Chart 1 shows the amount of cumulative tightening priced in for the BoC by meeting for the rest of 2026 compared to where we were at the end of February.

Chart 1 – Markets have pivoted to pricing hikes for the BoC since the start of the Middle East conflict

Source: BMO GAM, Bloomberg

This feels awfully aggressive, and in normal times we’d understand. But these are not normal times for the Canadian economy. The trade war with the US is an integral reason why the domestic unemployment rate has risen and why economic slack has opened up. That colours the energy price-to-inflation passthrough a bit different from prior supply shocks. For example, if finances are under strain, it’s more likely that households will cut back on all types of spending and for firms to pass on higher input costs. That makes the higher energy price story more acute for growth risks as opposed to inflation over the medium-term. This is a point that BoC Senior Deputy Governor Rogers specifically made at the post-meeting press conference last Wednesday.

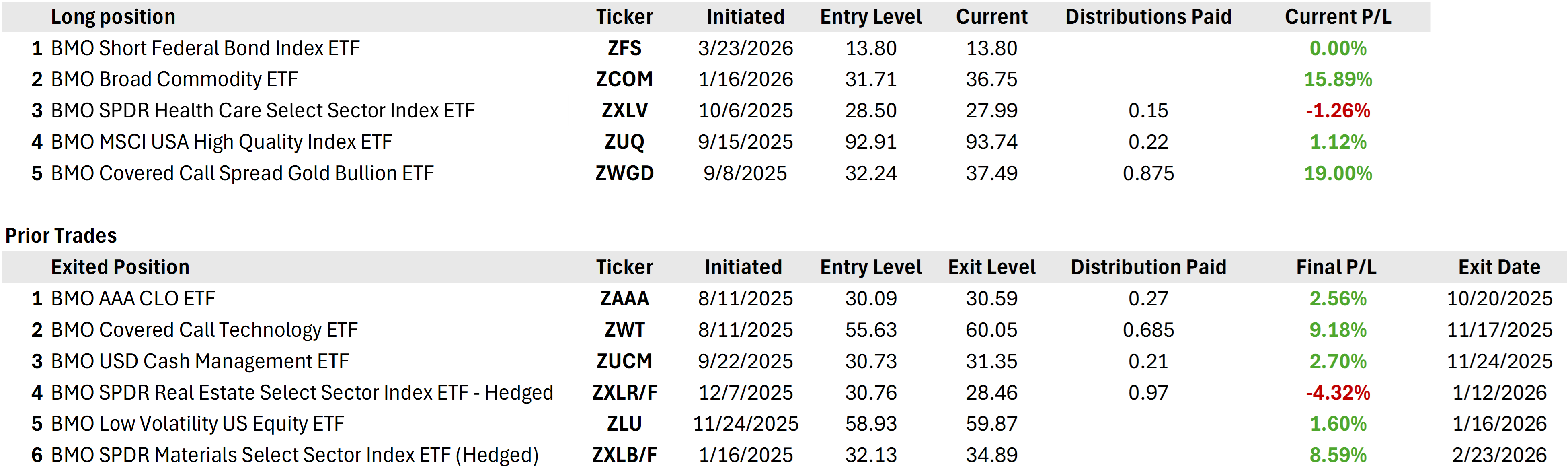

What does this mean? In simple terms, the BoC can probably afford to wait out this oil shock for longer than other central banks. By extension, the market has run too far in the front-end of the curve and that there is value in going long products that track that part of the CAD curve. That suggests scope for products like short and mid-term federal bond ETFs (ZPS, ZFS) as well as ZAG and ZDB to outperform tactically. We will be adding a long ZFS position in our ‘Book of Trades’ below.

Portfolio Stategy

a.) Thoughts on the Middle East: Over the weekend, President Trump threatened to ‘obliterate’ Iran’s power plants if the Strait of Hormuz was not opened by early Monday. In response, Iran has threatened to attack all other energy-related infrastructure in the region – including desalination facilities used by other Gulf countries. This would mark a significant escalation, and one that threatens to draw in other Middle Eastern countries into the conflict.

Our take: Without a coordinated effort to escort tankers through the Strait – there are only two realistic options left:

- A negotiated ceasefire

- US/Israeli boots on the ground

The first option would be ideal but is extremely unlikely at this point. The second option represents an escalation and a potential quagmire that wouldn’t solve the problem of Hormuz or damaged infrastructure anyway.

Nevertheless, a prolonged conflict doesn’t suit either side. A complete closure of Hormuz would mean no revenues for the Iranian regime, while higher oil prices will eventually mean political pressure on Trump back in the US. If you press us for an answer, this is why we expect both sides to eventually come together for talks, though we may have to go through further escalation before we get there.

b.) Gold, silver and base metals: There’s been a lot of head scratching over why exactly we’ve seen metals come under pressure. There are three ways that we’re framing this:

- Whenever a shock event happens, big shops tend to de-risk first and ask questions later. Long metals has been the consensus trade for months now and part of last week’s move likely reflects position rebalancing.

- While the risks to inflation are higher, commodity markets might be paying more tribute to the downside risks to global growth from here. That would especially be the case for base metals.

- There are palpable concerns that countries like Qatar, Kuwait, Saudi Arabia and the UAE may look to sell non-US dollar reserve holdings (including gold) to plug revenue gaps.

Having said the above, we think precious metals are a “buy the dip” story for now. The risks of a regime switch to ‘mild stagflation’ is becoming clearer – and commodities (especially gold) tend to outperform during those regimes.

c.) The week ahead: It’s a far less busier week than last week. Nevertheless, keep an eye on sentiment surveys as they roll in this week for signals as to how households/firms across the developed world are thinking about risks from higher costs from here.

Indeed, this week, we’ll get updated composite PMIs from several large economies (the first readings for March) as well as consumer confidence surveys from countries that are particularly exposed to the events in the Middle East (Germany, South Korea).

d.) Book of Trades: As stated above, we are initiating a long position in ZFS to our tactical ‘Book of Trades’.

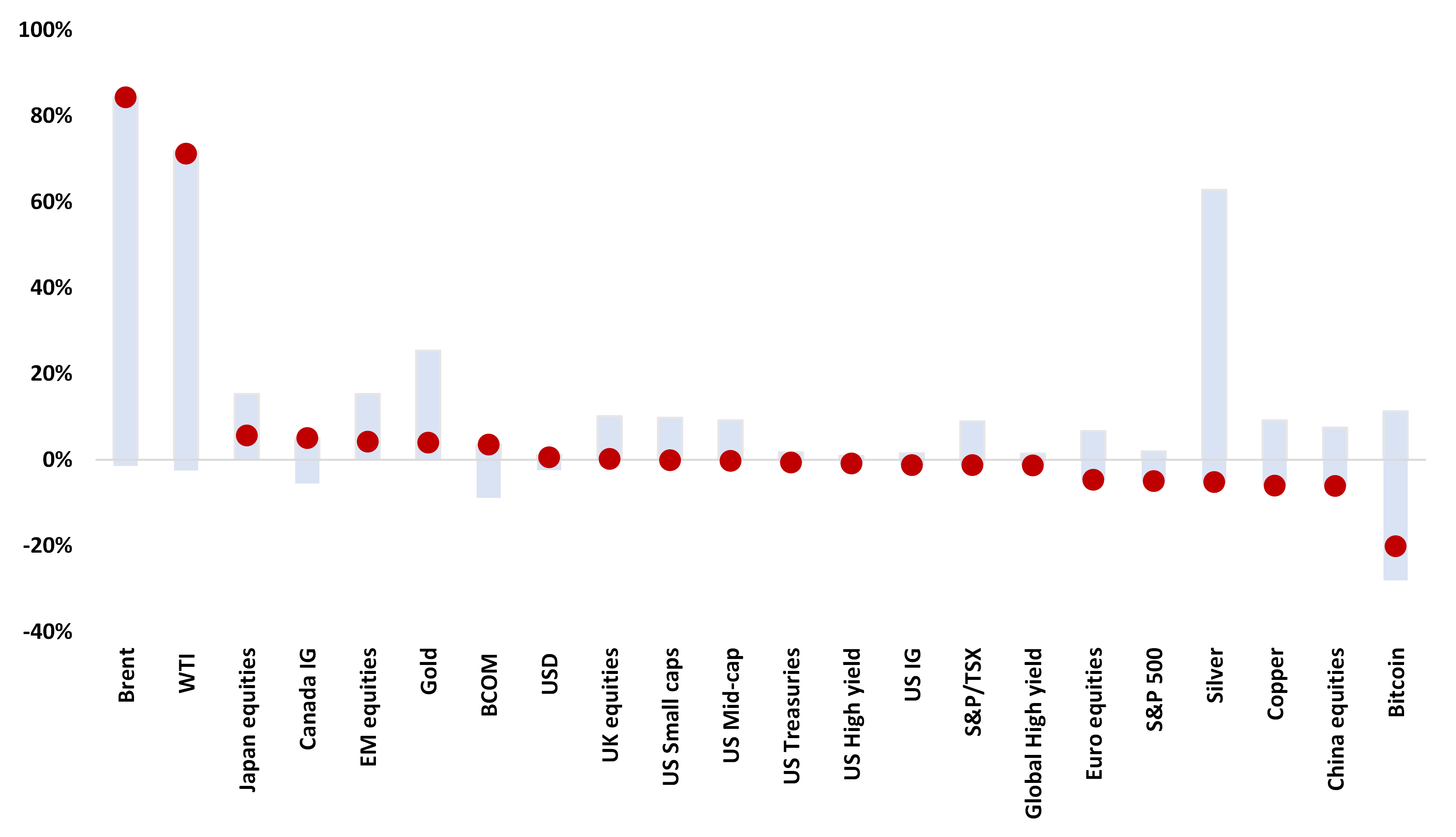

Asset Performance (Year-to-Date)

Source: Bloomberg, BMO GAM