Weekly Basis Points - Unpacking a Very Busy Macro Week

May 04, 2026

- In Canada, growth stabilized in February, but the underlying trend remains soft. Goods production provided a temporary lift, while persistent slack and rising energy costs point to weaker demand ahead.

- In the US, growth is increasingly unbalanced. Q1 GDP was supported by a rebound in government spending and a surge in AI‑driven business investment, but risks are building around consumption.

- Tech earnings remain strong, but leadership is fragmenting. The AI investment cycle continues to support earnings, but wider dispersion within the Magnificent Seven shows markets are rewarding execution over broad exposure.

There was a lot of macroeconomic data and events to chew on last week. Alongside GDP prints for both Canada and the US, we also had a busy run of earnings, and central bank meetings – with lots of important information likely getting missed by our readers. In this week’s write-up, we’ll strip away some of the noise and focus on the most meaningful takeaways. Given that we covered the important messages from the BoC and the Fed in our ‘Macro Note’ from Thursday, we’ll focus on data, earnings and other relevant macro bits.

1.) Canada GDP – Stable for Now: February GDP print came in at +0.2% m/m while the advance estimate for March was flat. That leaves Q1 GDP growth tracking at 1.7%, which is slightly above the Bank of Canada’s estimate from the April Monetary Policy Report.

The growth in February was driven almost entirely by goods production for the second consecutive month. Manufacturing surged +1.8% m/m, led by a sharp auto rebound as plants ramped up production after January shutdowns. Easing supply-chain frictions also lifted wholesale trade and transportation.

Despite the solid result for February, there are still question marks about domestic growth looking ahead. For one, the rise in gas prices is likely to weigh on household spending. In addition to that, the employment backdrop still looks mixed as the SEPH survey of employment fell 60K, leaving job gains broadly flat versus last year.

All told, Canada’s economy regained some footing in Q1, but the economy is far from running hot. With slack persisting and consumer demand likely to soften under higher energy costs, the BoC is expected to keep rates on hold for this year. While March’s advance estimate aligns with official projections, the flat quarter‑end reading weakens the handoff into Q2.

2.) Canada Spring Fiscal Update – Some Tinkering but No Change to the Overall Strategy

In terms of fiscal policy – it was a big week in Canada. Prime Minister Mark Carney’s Liberal government published the Spring Fiscal/Economic update. The notable takeaways here was that the current fiscal year deficit was revised lower (due to a better economic backdrop and delayed spending). Also, the government will be issuing fewer bills this year than expected as part of its debt management strategy.

While the focus remains on infrastructure and defense spending, the Carney government is using any additional fiscal space to support the private sector amidst an unpredictable trade/geopolitical backdrop.

3.) US GDP – AI-Related Investment is Still Doing the Heavy Lifting

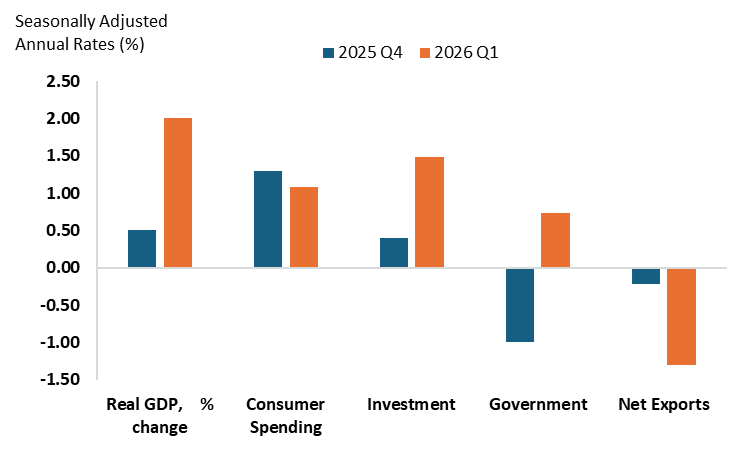

South of the border, Q1 GDP rebounded to a 2.0% annualized pace, recovering from the government shutdown-induced weakness in Q4 2025. However, the composition of growth reveals a critical shift. Chart 1 shows the rebound was driven by increased government spending and a big jump in business investment (largely driven by AI).

However, there are risks mounting for a key driver of US growth – consumption. The contribution of consumer spending to overall GDP growth was close to 1%. That isn’t a bad number per se, but with household savings already stretched and higher gasoline prices representing risks to the consumption profile, there’s limited room for that figure to increase in the coming quarters. Compounding the issue is the uncertain nature of the labor market backdrop.

The AI story showed up in two meaningful places. First, it affected net trade as the US imports of AI-related capital goods increased substantially from Q4 (representing a drag on net growth). Second, non-residential investment was boosted by strong contributions from AI proxies that we use (especially IP).

All told, there are signs here that US growth is cooling. At the same time, we’re not seeing signs that inflation is – which implies that the US might be tipping into a mild stagflation-like backdrop.

Chart 1: Contributions to Percent Change in Real Gross Domestic Product

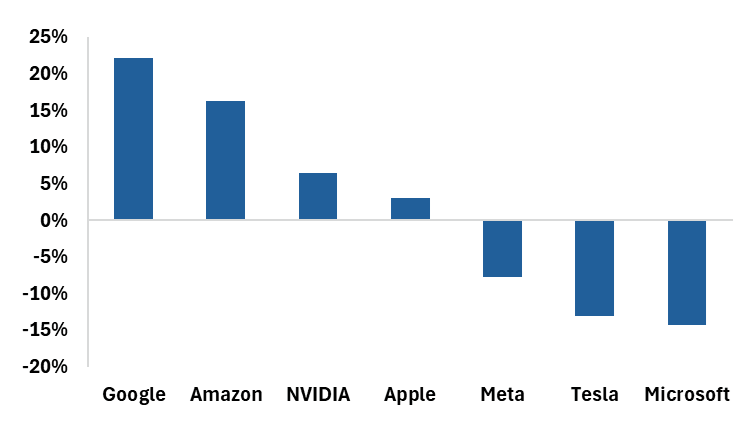

4.) US Earnings: Tech Performs, but With Dispersion

Lastly, it was also a big week for earnings with five of the Magnificent Seven reporting. While all the major tech firms that reported beat earnings expectations, we’re seeing greater signs of price dispersion - a shift that will be critically important going forward.

Technology remains the earnings engine because the AI investment cycle continues to accelerate, driving both revenue growth and capital deployment across the sector. However, Chart 2 shows the stark difference between the best and the worst performers year-to-date within the Magnificent Seven – with Google leading at +22%, while Microsoft is down roughly -13%. When all stocks in a theme move together, we can reasonably conclude that the market is pricing the story. However, when they diverge, the market is likely saturated on the beta and focusing more on the alpha plays (which are heavily dependent on clear AI monetization and overall strategy on capital expenditures).

Going forward, investors should focus on companies demonstrating visible AI monetization, pricing power, and cash flow delivery - not just those making the largest AI investments.

Chart 2: Magnificent Seven Year-to-Date Performance (%)

Source: BMO GAM, Bloomberg

Putting it All Together

The macro signals appear to be aligned. While not breaking, growth in the US and Canada is becoming more uneven with more reliance on investment and government spending as consumers lose momentum. At the same time, inflation is still elevated enough to keep policymakers cautious. In this backdrop, quality is the factor that should anchor portfolios, particularly in the US. The cleanest expression is through ZUQ (BMO MSCI USA High Quality Index ETF).

Within technology, leadership persists but dispersion argues for discipline rather than concentration. ZWT (BMO Covered Call Technology ETF) is well-positioned to generate attractive risk-adjusted returns, capturing income while cushioning volatility. At this stage of the cycle, resilience and cash generation matter far more than chasing growth at any price.

Portfolio Strategy

a.) Labor Market Takes Center Stage: There are a lot of employment reports this week.

- US JOLTS (March) + ISM services (April) on Tuesday: Both will provide critical labor market context ahead of Friday’s payrolls. Keep an eye on the ISM Services Employment Index in particular - if it stays soft, it reinforces the idea that firms are turning more cautious on hiring ahead of Friday’s jobs report.

- US Nonfarm payrolls for April (Fri): The April employment report is the marquee release. Consensus estimates look subdued (roughly between 60k – 70k), signaling a slowdown since March. The unemployment rate is expected to stay unchanged at 4.3%.

- Canada unemployment rate (Fri): Given the decent Q1 GDP growth tracking, labor market data will be important to determine whether the risks are tilted towards BoC hikes from here.

b.) Earnings Beyond Mega-Cap Tech: With mega-cap tech having already reported, the market needs to see strength spreading to cyclicals to justify current valuations. Indeed, narrow leadership would be a warning sign.

What to watch by sector:

- Technology (Palantir, AMD): These test whether AI-driven demand strength extends beyond the mega-caps.

- Consumer Discretionary (McDonald’s) & Communication Services (Disney): Critical tests of consumer resilience. With household spending momentum slowing in real terms and gasoline prices elevated, any signs of demand weakness or margin pressure will be closely scrutinized.

- Energy (Shell): The key will be guidance, particularly around capital allocation and whether firms see current prices as sustainable.

- Other sectors: Financials (PayPal), Healthcare (CVS, Pfizer)

c.) Central Banks & Policy: With the major central markets now behind us, attention shifts to secondary policy catalysts and how markets digest last week’s guidance through fresh data.

The Reserve Bank of Australia (RBA) headlines the week on the policy front, with the cash-rate decision due Tuesday. RBA is expected to hike it cash rate by 25bps to 4.35%, reflecting Australia’s response to rising inflation pressures. This will be the third consecutive hike, so the focus will be on how sticky inflation looks and how willing the RBA is to keep tightening.

Other rate decisions: Sweden (Riksbank), Norway (Norges Bank), and Mexico (Banxico) are also on deck (Thursday).

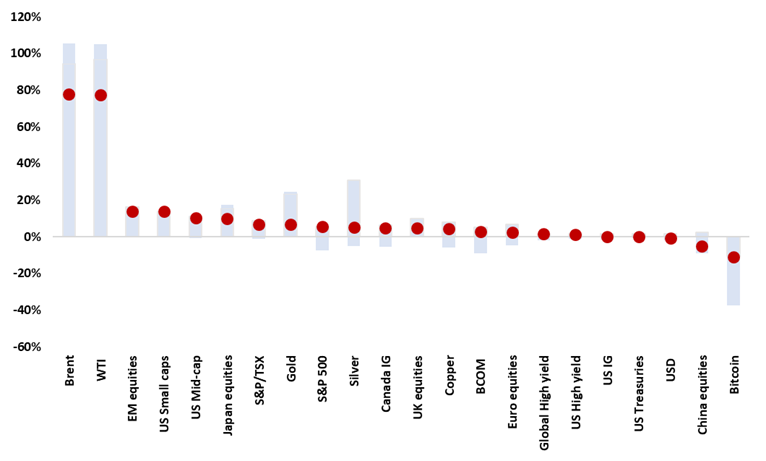

Chart - Asset Performance (Year-to-Date)

Data as of May 1, 2026

Source: Bloomberg, BMO GAM