Weekly Basis Points - Yes, Gold Can Still Go Higher from Here

September 29, 2025

- There are several reasons for why investors should look to maintain or increase allocation to Gold in the quarters ahead including its utility as a store of value, inflation hedge and diversification properties.

- However, there is another bullish tailwind that has emerged which should take Gold towards our target of $4500 by mid-2026 – increased retail/institutional demand.

- Investors could look at several different options off the shelf here at BMO GAM – including ZJG, ZGD, ZGLD and ZWGD.

We’re kicking things off with a rather bold title for our weekly. Indeed, this reflects our conviction in the direction for Gold in the coming quarters – which in turn is based on a number of bullish reasons that we’ve covered in prior notes and should be familiar with most readers.

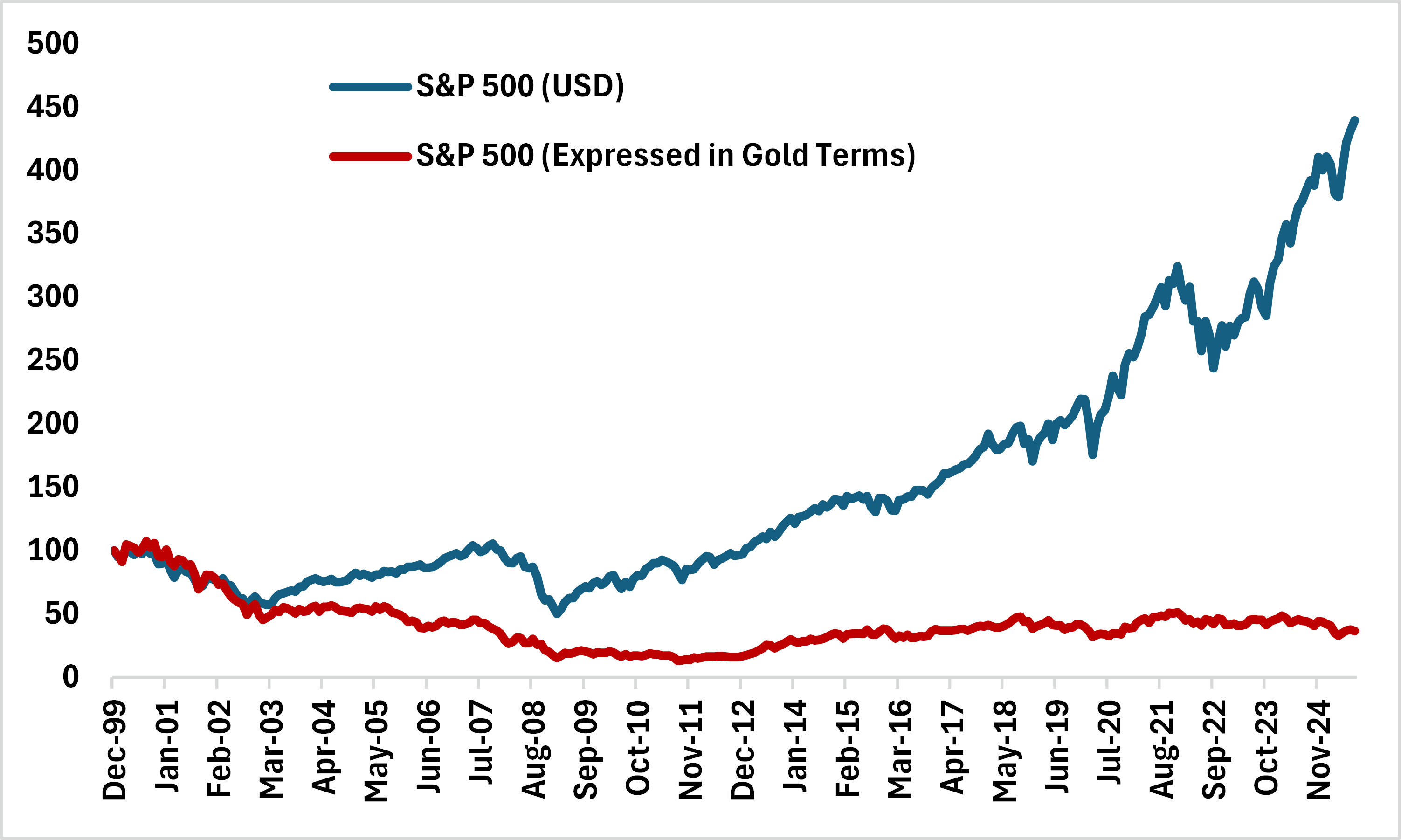

For instance, we could go over its utility as a store of value. But all you have to do is to consider Chart 1, which shows the performance of the S&P 500 in US dollar terms and when expressed against Gold since the turn of the century. For the former, the S&P 500 is up over 600% in total return. But against Gold? The S&P 500 is lower by over 60%.

Chart 1 – The S&P 500 has Underperformed Relative to Gold Over the Past Decades

Of course, we could also look at Gold’s utility as an inflation hedge. There is already a considerable amount of literature out there that shows how well Gold outperforms during periods of high inflation. But if you need more convincing, it’s relatively easy to replicate a study that shows that Gold will average a 1% m/m gain during periods when US CPI is above 3% (going back 50 years). That’s much better than equities or US Treasuries under similar conditions over that time.

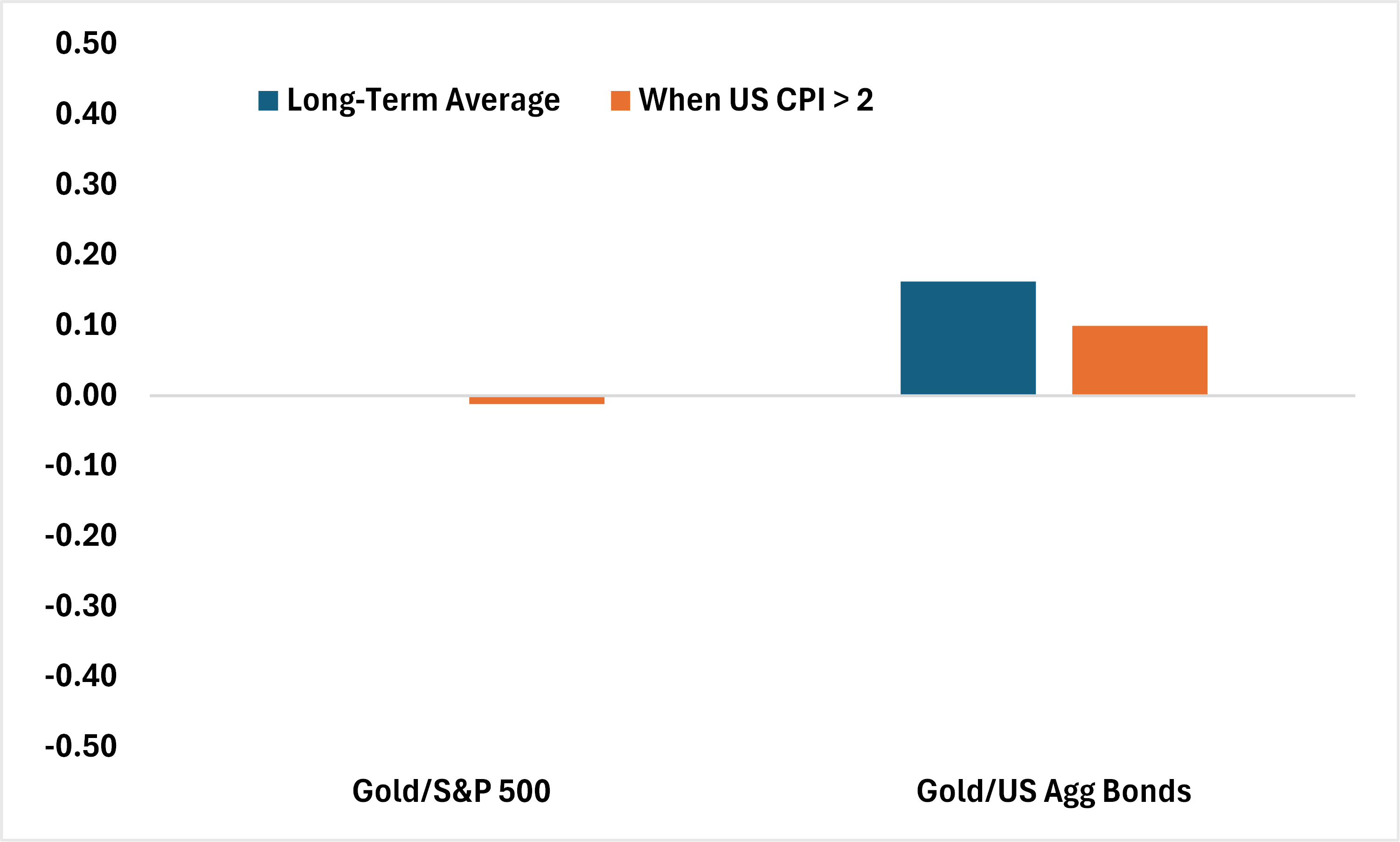

Additionally, the benefits of holding Gold as a diversification instrument are also well understood by now. Consider Chart 2 which shows that regardless of whether we’re in a period of high inflation not, the degree of correlation between Gold and stocks/bonds tends to be low. This means that increased allocation to Gold will usually result in lower overall volatility for the portfolio.

Chart 2 – Gold is Always a Great Diversifier

Source: BMO GAM, Bloomberg

Naturally, all of the above benefits tend to drive flow into the precious metal during bouts of increased uncertainty and volatility. And to be sure, you can make a fairly simple case that the recent rise in Gold is a direct result of concerns related to inflation and a general erosion of trust in key US institutions.

However, looking past all of the above reasons, there is another important reason for why our readers should consider increasing their allocation to Gold going forward.

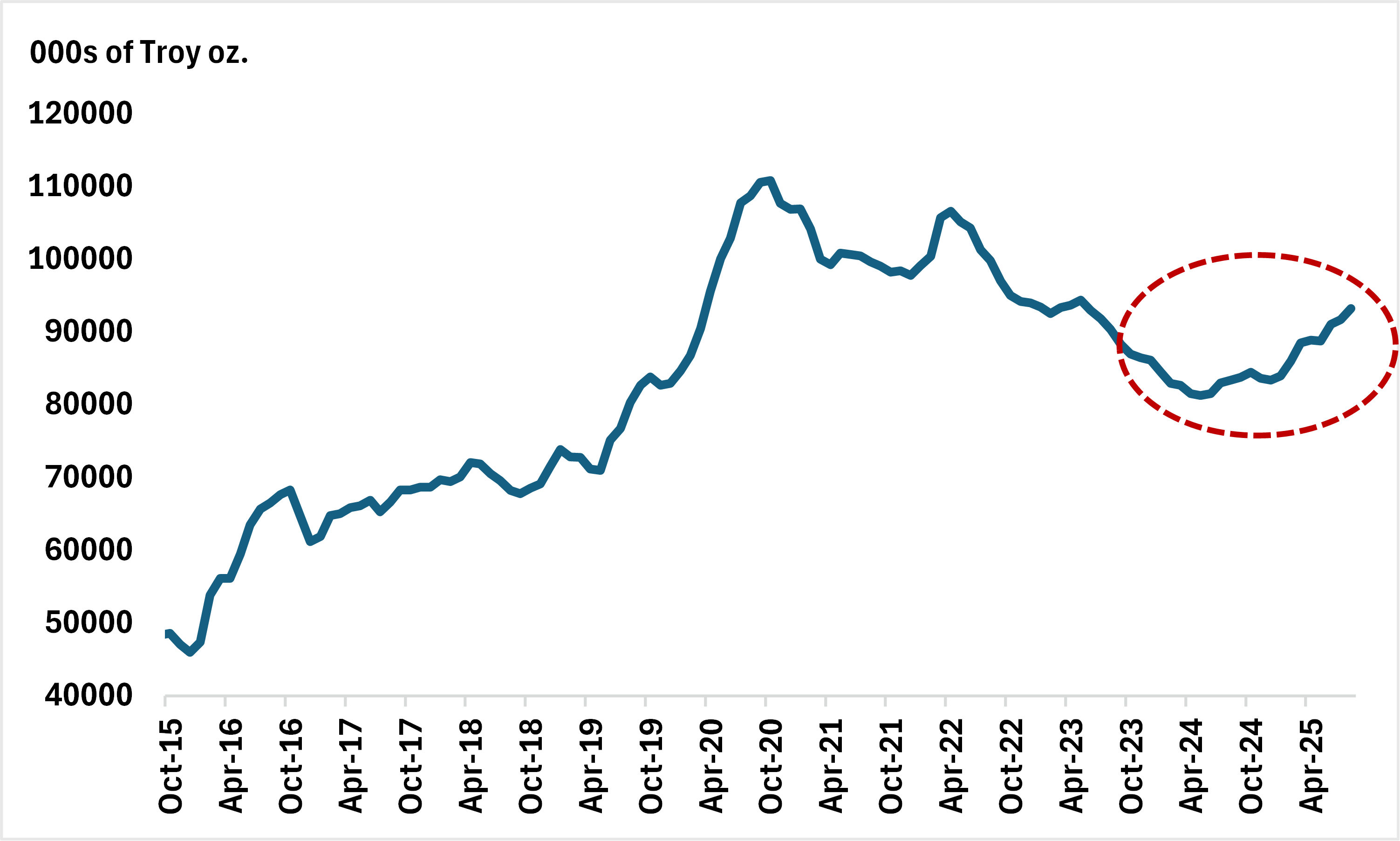

Remember that over the past few years, central banks have been massive buyers of the precious metal – while the retail/institutional flow (via ETFs) haven’t participated as much. While we still expect central bank buying to remain strong, the latest ETF flow data also indicates that the retail/institutional crowd will be buying as well. The increased flow via ETFs likely reflects concern over the trajectory of global inflation as well as a stronger sense of ‘FOMO’ (or the fear of missing out).

Chart 3 – Total Known ETF Holdings of Gold are Tracking Higher Now

That flow adds another bullish tailwind to an already constructive story when it comes to Gold. While many will be concerned on how fast prices have risen of late, that doesn’t obviate the facts that i) long-term fundamentals have shifted, and ii) that a significant amount of flow is now playing catch-up. It is for those reasons, that we’re now expecting Gold prices to reach $4500 by mid-2026.

There are many ways to play this out going forward. For example, among the top performing ETFs this year have been two that focus on Gold miners – including ZGD (or the BMO Equal Weight Global Gold Index ETF) and ZJG (or the BMO Junior Gold Index). As of the end of last week, both of those ETFs are up by over 100% since the end of last year.

Alternatively, for those that want to minimize the risks associated with mining companies and focus on Gold itself, the ZGLD (BMO Gold Bullion ETF) is up by close to 40% since end-2024. Of course, one of the more frequent criticisms of owning Gold is the lack of yield – especially when storage costs are taken into consideration. However, the ZWGD (or the BMO Covered Call Spread Gold Bullion ETF) has addressed this to a meaningful degree. Indeed, this ETF allows investors to gain exposure to Gold prices while also earning premiums through a covered call spread strategy.

For now, we’re long Gold via both ZGLD and ZWGD in our tactical portfolio. In our updated ‘Balanced Portfolio’ for Q4, we will be bumping up our allocation to ZWGD.

Tactical Positioning

Existing

- ZUCM (BMO USD Cash Management ETF)

- ZUQ (BMO MSCI USA High Quality Index ETF)

- ZGLD (BMO Gold Bullion ETF)

- ZWGD (BMO Covered Call Spread Gold Bullion ETF)

- ZWT (BMO Covered Call Technology ETF)

- ZAAA (BMO AAA CLO ETF)

Portfolio Strategy

After talking about it for weeks, we’re now finally starting to see the backup in US yields as markets reassess the trajectory for the Fed going forward. This is passing through to other asset classes as well, as equities stumbled a bit last week while the USD gained some momentum.

Of course, the catalyst for these moves has been the stronger data out of the US – with the final estimate of Q2 GDP coming in at 3.8%. Also, durable goods orders and personal income/outlays both suggest that demand is picking up and that price pressures could be a bit too sticky for the Fed’s comfort. Indeed, early estimates of growth for this quarter have the US economy expanding by over 3%(!) – which is another indication that the Fed may not be as quick to ease policy.

The above tells us that the risks to US yields are still marginally higher, but we’ll likely need fresh impetus from the data. This week brings the release of both ADP and Nonfarms, both of which will be important inputs in the market’s read from here.

Also, keep an eye on government shutdown risks into Tuesday evening.

Asset Class |

View |

Notes |

Equities |

Slightly bullish |

|

Fixed Income |

Slightly bearish |

|

Alternatives |

Bullish |

|

FX |

Slightly bearish USD/CAD |

|