What stagflation means for your portfolio

Here’s a question that is open to debate, but we’ll ask it anyway - what is the one economic backdrop that is most concerning for a central banker?

No, it’s not a recession or a depression. The solution to either of those is intuitive enough – stimulate the economy by lowering interest rates and/or by increasing the size of the central bank’s balance sheet. It’s also not periods of excess demand – which is characterized by strong growth and high inflation. The remedy there is to ensure that financial conditions remain tight enough to prevent elevated inflation from becoming embedded in expectations.

Instead, we suspect that if we polled enough central bankers, the vast majority would answer‘stagflation’. For those that may not be as familiar, this is a backdrop characterized by slower real activity, a rising unemployment rate and a general increase in consumer prices. For central bankers, a period of stagflation means the need to prioritize one of two competing issues – either stable prices or stable growth.

The path the central banker chooses matters for markets and investors.

If the central banker elects to prioritize economic growth, then this would mean loosening monetary policy conditions. For instance, in response to weak credit demand, the U.S. Federal Reserve (Fed) could cut rates to engender easier access to credit for firms which would help them invest and hire more. However, the pickup in activity would also portend a further rise in prices – compounding the issue of the lack of stability in inflation.

On the flip side, the central banker could elect to keep rates elevated or hike them further to address the issue of rising prices. But that would mean credit access becomes tighter, and that firms become more reluctant to invest and hire – which would (in turn) compound the issue of falling real activity and higher unemployment.

Why are we bringing this up? Because there are growing risks that the U.S. economy is about to enter a period of mild stagflation. For instance, recent Consumer Price Index (CPI) and Producer Price Index (PPI) prints suggest that the Fed’s progress on curbing inflationary pressures had stalled.1 At the same time, the more recent non-farms payroll numbers suggest that there are cracks appearing in the U.S. labour market.

Despite all this, markets are pricing the Fed to cut three more times in 2025 and a few more in 2026 to take the terminal rate2 to 3.00%. At the margin, this would imply that the market feels that the Fed will prioritize growth risks. Implicitly, that also corresponds to even less progress on its inflation mandate. As such, we’ve seen inflation expectations rise (yet again) in the Michigan survey.3

So then, how should our readers position their portfolios in advance of such an event?

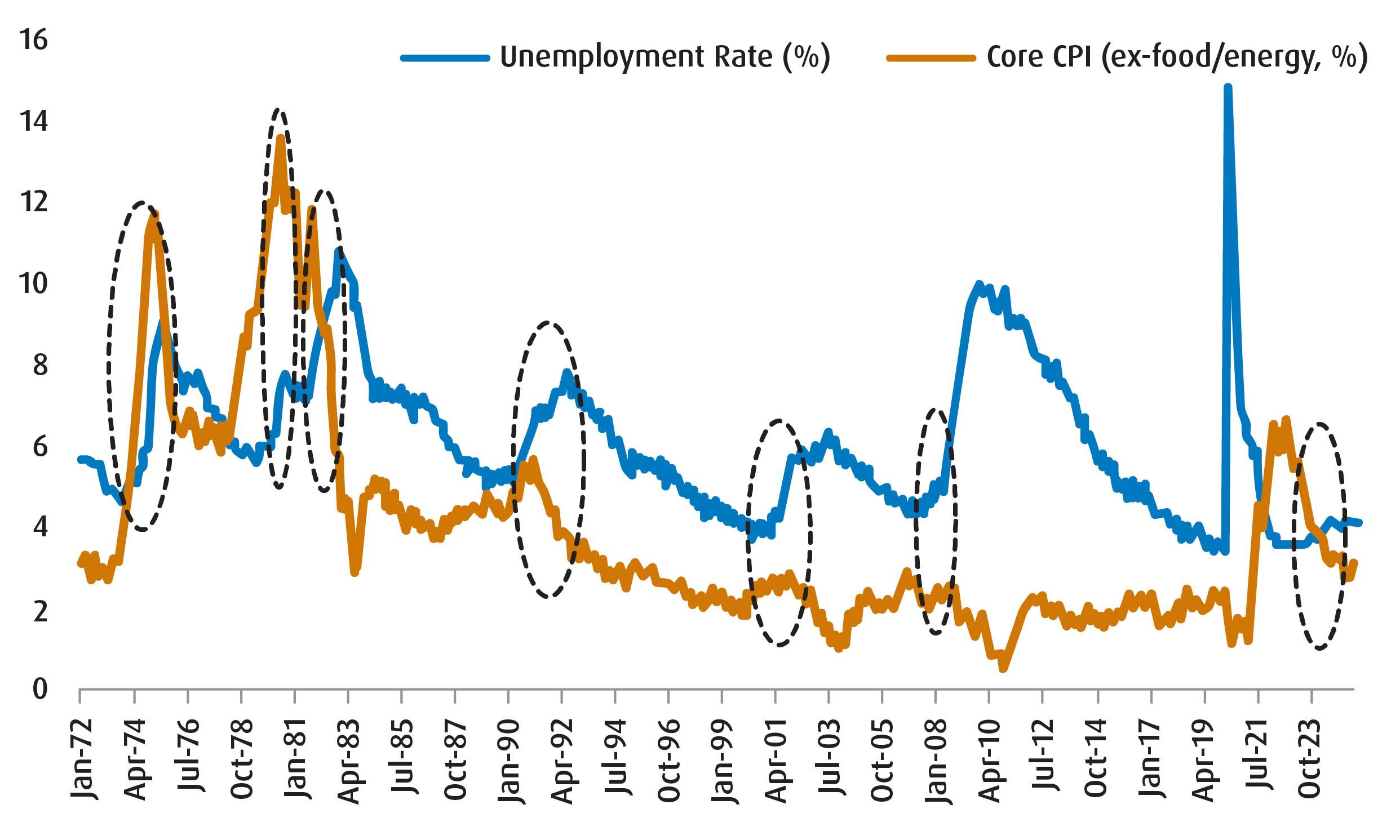

Luckily for us, we do have the benefit of hindsight. Indeed, we can look back at prior periods ofstagflation to gauge how each asset class behaved to come up with a gameplan. Of course, defining when a period of stagflation begins or ends is tricky, so we’ll rely on an easy-to-understand heuristic that is simple enough for our readers to understand. For instance, we’ll look back on prior periods when the unemployment rate rose by at least 0.5% over the prior 12 months and when core inflation (ex-food/energy) was above 2.5%. Chart 1 shows those periods overlaid on both the U.S. unemployment rate and core inflation going back 50 years.

Chart 1 – Prior periods of stagflation in the U.S.

In our analysis, we find that for each time the economy entered a period of stagflation the S&P 500 declined. The average drawdown corresponded to about 15.7% over an average 4.5 months. For most of those periods, over the time it took for the S&P 500 to bottom out, we found that Gold did a much better job of preserving its value, with an average of drawdown of about 4.8%.

Admittedly, the one observation that we were surprised to see was the outperformance of indices that tracked US Treasuries over those same periods. We’d chalk that up to structural factors (namely, the 40-year bullish market for bonds) that are far less of a tailwind these days. For example, the last observation period is 2024 – and bonds underperformed relative to Gold.

For US Treasuries, the other complication is where we are in terms of the monetary cycle. While the Fed is expected to ease rates (supportive for the front end of the yield curve4), the long-end is likely to remain pinned and/or defensive given the rise in inflation expectations.

Table 1 – Performance of the S&P 500 during prior periods of stagflation

Begins | S&P 500* | Time to bottom | Gold Performance** | UST Index Performance** | |

|---|---|---|---|---|---|

I | Apr-24 | -4.2% | 1 month | 2.5% | -2.3% |

II | May-08 | -16.7% | 9 months | -1.8% | 3.1% |

III | May-01 | -17.1% | 4 months | 10.3% | 6.1% |

IV | Aug-90 | -14.6% | 3 months | 1.9% | 1.1% |

V | Nov-81 | -15.2% | 8 months | -17.3% | 7.3% |

VI | Feb-80 | -10.1% | 1 month | -22.4% | 1.1% |

VII | Jun-74 | -27.2% | 4 months | -7.0% | 2.6% |

Average | -15.0% | 4.5 months | -4.8% | 2.7% |

Source: Bloomberg, BMO Global Asset Management.

*The above table looks at the performance of the S&P 500 from the start of prior periods that we identify as‘stagflation’ to where the index bottomed out.

**The performance of Gold and UST Index is also observed over that same timeframe.

What do we take away from this? A few things…

- Though periods of stagflation can differ in terms of intensity, they usually result in risk-off markets (lower U.S. equities).

- Gold does a better job of preserving its value relative to equities.

- Bonds have, surprisingly, held in relatively well – though we’d be less inclined to believe that this will be the case going forward.

However, this is just a risk to monitor for now. Even by the standards of our own heuristic we’d still need to see the unemployment rate rise by a bit more before the current backdrop would be consistent with a technical stagflation episode. Nevertheless, if we do start to see more signs of weakness in the U.S. labour market, it would be prudent to shift some allocation towards alts.

Indeed, this is consistent with our view that alternatives and hybrids are much better diversification instruments at this point than bonds.

Tactical Positioning

- New…

- Changes…

Portfolio strategy:

a.) We still continue to favour Equities and Alts over Fixed Income.

- Equities: While we are wary of near-term stagflation risks, we remain neutral in our balanced ETF portfolio. Indeed, our optimism on the fundamentals (earnings) is tempered to a degree by extant valuation and sentiment. Within this space, we continue to favour US large caps (tech, communications, financials and utilities) and like augmenting that with increased exposure to EM.

- Fixed Income: We’re underweight this asset class in our balanced portfolio. We continue to optimize for‘high yield + short duration’5 with preference for sub-sovereign exposure.

- Alts/Cash: We continue to like gold and infrastructure as diversifiers.

b.) Current holdings (balanced portfolio):

Fixed income

- BMO Discount Bond Index ETF (Ticker: ZDB)

- BMO Canadian Bank Income Index ETF (Ticker: ZBI)

- BMO Short-Term US Treasury Bond Index ETF (Ticker: ZTS)

Equities

- BMO MSCI USA High Quality Index ETF (Ticker: ZUQ)

- BMO Low Volatility Canadian Equity ETF (Ticker: ZLB)

- BMO Low Volatility International Equity ETF (Ticker: ZLI)

- BMO Equal Weight Industrials Index ETF (Ticker: ZIN)

- BMO MSCI Emerging Markets Index ETF (Ticker: ZEM)

Alts/Non-traditional hybrids

- BMO Long Short US Equity ETF (Ticker: ZLSU)

- BMO Long Short Canadian Equity ETF (Ticker: ZLSC)

- BMO Covered Call Spread Gold Bullion ETF (Ticker: ZWGD)

- BMO Global Infrastructure Index ETF (Ticker: ZGI)

c.) Views

Asset class | View | Notes |

Equities | Slightly bullish |

|

Fixed income | Slightly bearish |

|

Alternatives | Slightly bullish |

|

FX (CAD) | Neutral |

|

Region | View | Notes |

Canada | Neutral |

|

U.S. | Neutral |

|

EAFE | Neutral |

|

EM (China) | Neutral |

|

EM (ex-China) | Neutral |

|

1 The Consumer Price Index (CPI) and Producer Price Index (PPI) are both measures of inflation, but they track price changes from different perspectives. CPI measures the average change over time in the prices consumers pay for a basket of consumer goods and services, while PPI tracks changes in prices received by domestic producers for their output.

2 Terminal rate: refers to the peak or lowest interest rate that a central bank, like the Federal Reserve, is expected to reach during a specific interest rate cycle. It’s essentially the highest or lowest point the central bank’s key policy rate (like the federal funds rate) will reach before it potentially starts to decline/increase.

3 Refers to the University of Michigan’s Surveys of Consumers, specifically the Michigan Consumer Sentiment Index (MCSI). This is a monthly survey that measures consumer confidence in the US economy.

4 Yield curve: A line that plots the interest rates of bonds having equal credit quality but differing maturity dates. A normal or steep yield curve indicates that long-term interest rates are higher than short-term interest rates. A flat yield curve indicates that short-term rates are in line with long-term rates, whereas an inverted yield curve indicates that short-term rates are higher than long-term rates.

5 Duration: A measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as number of years. The price of a bond with a longer duration would be expected to rise (fall) more than the price of a bond with lower duration when interest rates fall (rise).

6 The breakeven inflation rate is calculated by subtracting the yield of an inflation-protected bond from the yield of a nominal bond during the same time period.

Performance (%)

Year-to-date |

1-month |

3-month |

6-month |

1-year |

3-year |

5-year |

10-year |

Since inception |

|

Returns are not available as there is less than one year’s performance data. |

|||||||||

7.96 |

4.57 |

24.50 |

3.86 |

25.72 |

34.17 |

- |

- |

19.98 |

|

0.56 |

-0.82 |

-0.77 |

-0.64 |

2.74 |

2.60 |

-0.86 |

1.52 |

2.21 |

|

3.01 |

0.55 |

2.12 |

2.23 |

6.74 |

6.03 |

- |

- |

3.97 |

|

-0.56 |

1.56 |

0.68 |

-2.11 |

4.53 |

5.43 |

1.26 |

- |

2.13 |

|

1.61 |

2.25 |

9.50 |

-3.09 |

9.73 |

21.00 |

15.45 |

15.04 |

16.17 |

|

15.10 |

1.15 |

5.80 |

13.37 |

18.93 |

13.52 |

13.96 |

9.86 |

12.50 |

|

11.10 |

-2.88 |

-0.86 |

5.64 |

14.10 |

12.00 |

7.08 |

- |

6.20 |

|

7.17 |

1.70 |

21.91 |

11.63 |

14.42 |

13.33 |

15.29 |

10.82 |

11.20 |

|

13.48 |

3.37 |

13.05 |

10.39 |

15.91 |

12.32 |

5.58 |

6.00 |

5.26 |

|

5.03 |

1.98 |

7.47 |

0.62 |

18.81 |

- |

- |

- |

23.35 |

|

11.27 |

0.72 |

9.77 |

10.28 |

19.78 |

- |

- |

- |

20.49 |

|

Returns are not available as there is less than one year’s performance data. |

|||||||||

2.62 |

0.72 |

-0.45 |

2.25 |

13.24 |

7.52 |

10.24 |

7.59 |

11.42 |

|

Bloomberg, as of July 31, 2025. Inception date for ZXLV = February 4, 2025, ZAAA = April 30, 2025, ZWT = January 20, 2021, ZDB = February 10, 2014, ZBI = February 7, 2022, ZTS = February 21, 2017, ZUQ = November 5,2014, ZLB = October 21, 2011, ZLI = September 2, 2015, ZIN = November 14, 2012, ZEM = October 20, 2009, ZLSU/ZLSC = September 27, 2023, ZWGD = May 22, 2025, ZGI = January 19, 2010.

Disclaimers:

Changes in rates of exchange may also reduce the value of your investment.

The communication is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

The viewpoints expressed by the authors represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

CLOs are floating- or fixed-rate debt securities issued in different tranches, with varying degrees of risk, by trusts or other special purpose vehicles (“CLO Issuers”) and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The BMO ETF pursues its investment objective by investing, under normal circumstances, at least 85% of its net assets in CLOs that, at the time of purchase, are rated AAA or the equivalent by a nationally recognized statistical rating organization.

AAA herein refers to the order of payments, should there be any defaults, and does not represent the ratings of the underlying loans within the CLO. If there are loan defaults or the CLO Issuer’s collateral otherwise underperforms, scheduled payments to senior tranches take precedence over those of mezzanine tranches (a tranche or tranches subordinated to the senior tranche), and scheduled payments to mezzanine tranches take precedence over those to subordinated/equity tranches. The riskiest portion is the“Equity” tranche, which bears the first losses and is expected to bear all or the bulk of defaults from the corporate loans held by the CLO Issuer serves to protect the other, more senior tranches from default.

The portfolio holdings are subject to change without notice and only represent a small percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

The ETF referred to herein is not sponsored, endorsed, or promoted by MSCI and MSCI bears no liability with respect to the ETF or any index on which such ETF is based. The ETF’s prospectus contains a more detailed description of the limited relationship MSCI has with the Manager and any related ETF.

The Select Sector SPDR Trust consists of eleven separate investment portfolios (each a “Select Sector SPDR ETF” or an “ETF” and collectively the “Select Sector SPDR ETFs” or the “ETFs”). Each Select Sector SPDR ETF is an “index fund” that invests in a particular sector or group of industries represented by a specified Select Sector Index. The companies included in each Select Sector Index are selected on the basis of general industry classification from a universe of companies defined by the S&P 500®. The investment objective of each ETF is to provide investment results that, before expenses, correspond generally to the price and yield performance of publicly traded equity securities of companies in a particular sector or group of industries, as represented by a specified market sector index.

The SPDRs, and Select Sector SPDRs are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use. The stocks included in each Select Sector Index were selected by the compilation agent. Their composition and weighting can be expected to differ to that in any similar indexes that are published by S&P.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

Distribution yields are calculated by using the most recent regular distribution, or expected distribution, (which may be based on income, dividends, return of capital, and option premiums, as applicable) and excluding additional year end distributions, and special reinvested distributions annualized for frequency, divided by current net asset value (NAV). The yield calculation does not include reinvested distributions.

Distributions are not guaranteed, may fluctuate and are subject to change and/or elimination. Distribution rates may change without notice (up or down) depending on market conditions and NAV fluctuations.

The payment of distributions should not be confused with the BMO ETF’s performance, rate of return or yield. If distributions paid by a BMO ETF are greater than the performance of the investment fund, your original investment will shrink. Distributions paid as a result of capital gains realized by a BMO ETF, and income and dividends earned by a BMO ETF, are taxable in your hands in the year they are paid.

Your adjusted cost base will be reduced by the amount of any returns of capital. If your adjusted cost base goes below zero, you will have to pay capital gains tax on the amount below zero.

Cash distributions, if any, on units of a BMO ETF (other than accumulating units or units subject to a distribution reinvestment plan) are expected to be paid primarily out of dividends or distributions, and other income or gains, received by the BMO ETF less the expenses of the BMO ETF, but may also consist of non-taxable amounts including returns of capital, which may be paid in the manager’s sole discretion. To the extent that the expenses of a BMO ETF exceed the income generated by such BMO ETF in any given month, quarter, or year, as the case may be, it is not expected that a monthly, quarterly, or annual distribution will be paid. Distributions, if any, in respect of the accumulating units of BMO Short Corporate Bond Index ETF, BMO Short Federal Bond Index ETF, BMO Short Provincial Bond Index ETF, BMO Ultra Short-Term Bond ETF and BMO Ultra Short-Term US Bond ETF will be automatically reinvested in additional accumulating units of the applicable BMO ETF. Following each distribution, the number of accumulating units of the applicable BMO ETF will be immediately consolidated so that the number of outstanding accumulating units of the applicable BMO ETF will be the same as the number of outstanding accumulating units before the distribution. Non-resident unitholders may have the number of securities reduced due to withholding tax. Certain BMO ETFs have adopted a distribution reinvestment plan, which provides that a unitholder may elect to automatically reinvest all cash distributions paid on units held by that unitholder in additional units of the applicable BMO ETF in accordance with the terms of the distribution reinvestment plan. For further information, see the distribution policy in the BMO ETFs’ prospectus.

Past Performance is not indicative of future results.

Commissions, management fees and expenses all may be associated with investments in exchange traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., which is an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.