Macro Notes - There is Still a Lot of Money in GICs…But Why?

August 08, 2025

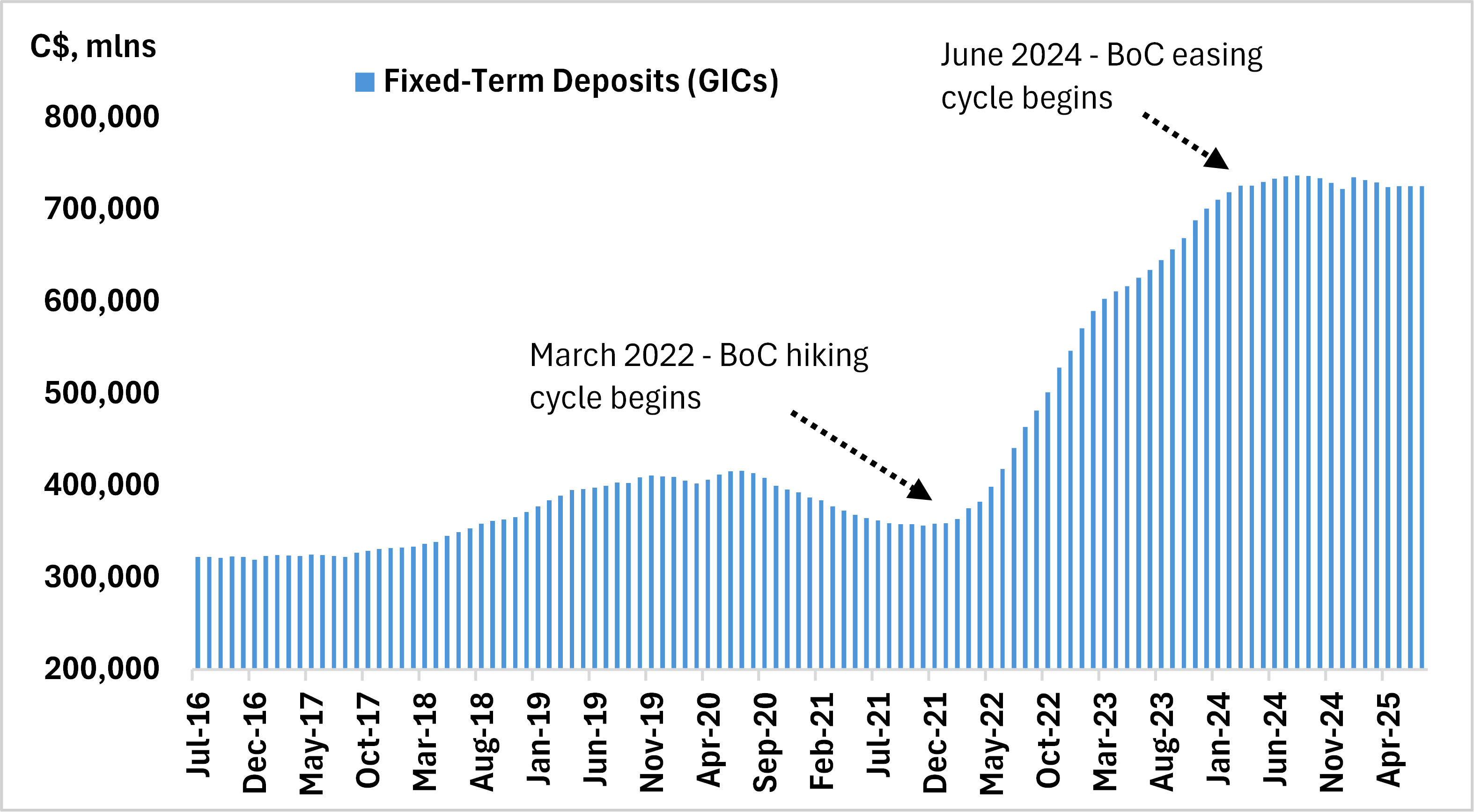

When the Bank of Canada began its hiking cycle in March 2022, money flowed into fixed-term deposits (namely, GICs) offered by chartered banks In Canada.

It’s curious then that since the BoC began easing policy rates in June 2024, that we haven’t seen a corresponding shift out of GICs into other higher yielding products.

Instead, the stock of assets held in GICs has remained steady, even as the 1-year GIC rate has moved from just above 5.00% in late 2023 to 2.62% now (using the BoC’s reference rate).

The most likely reasons for this include (but are not limited to):

- Firstly, it’s still too early. That could mean that a greater percentage of GICs are non-redeemable (i.e – investors are holding them to term to earn full interest) than we originally believed.

- Second, market participants are still too cautious about venturing too far out the risk spectrum.

- Third, households are keeping cash in GICs in advance of mortgage resets.

We covered the looming mortgage refinancing cliff in a prior post. Long story short, a significant number of Canadian households will be facing higher monthly payments (relative to end-2024) in the quarters ahead.

In our minds, this is likely the primary reason why money in GICs hasn’t exhibited the same degree of yield sensitivity that we’d have expected by now. If true, we should see this series decline as mortgages reset in the coming quarters – with residual flow shifting into yield enhancement products.

Chart 1 – Total Money Held in Fixed-Term Deposits in Canada

Source: BoC, BMO GAM