BMO Macro Regime Model – Strategy Report (Q2 2026)

All prices, returns and portfolio weights are as of market close on March 31, 2026, unless otherwise indicated.

In this report:

Table 1 – Macro Regime Portfolio for Q2 2026

| Ticker | ETF Name | Sector Positioning | Management Fee | Weight (%) | Volatility Contribution | |

| Fixed Income | ||||||

| ZDB | BMO Discount Bond Index ETF | Fixed Income | Core | 0.09% | 8.00% | 2.75% |

| ZUAG | BMO US Aggregate Bond Index ETF | Fixed Income | Core | 0.08% | 5.00% | 2.74% |

| ZTIP | BMO Short-Term US TIPS Index | Fixed Income | Tactical | 0.15% | 5.00% | 1.96% |

| ZBI | BMO Canadian Bank Income Index ETF | Fixed Income | Tactical | 0.25% | 7.00% | 1.50% |

| Total Fixed Income | 25.00% | 8.96% | ||||

| Equities | ||||||

| ZUQ | BMO MSCI USA High Quality Index ETF | Equity | Core | 0.30% | 23.00% | 21.84% |

| ZCN | BMO S&P/TSX Capped Composite Index ETF | Equity | Core | 0.05% | 20.00% | 23.85% |

| ZEA | BMO MSCI EAFE Index ETF | Equity | Core | 0.20% | 9.00% | 10.44% |

| ZEM | BMO MSCI Emerging Markets Index ETF | Equity | Tactical | 0.25% | 5.00% | 8.86% |

| ZLU | BMO Low Volatility US Equity ETF | Equity | Tactical | 0.30% | 4.00% | 3.16% |

| Total Equity | 61.00% | 68.16% | ||||

| Non-Traditional Hybrids | ||||||

| ZWGD | BMO Covered Call Spread Gold Bullion ETF | Hybrid/Alt | Tactical | 0.65% | 4.00% | 9.61% |

| ZGIF | BMO Global Infrastructure Fund ETF | Hybrid/Alt | Tactical | 1.05% | 4.00% | 3.12% |

| ZCOM | BMO Broad Commodity ETF | Hybrid/Alt | Tactical | 0.65% | 6.00% | 10.16% |

| Total Alternatives | 14.00% | 22.88% | ||||

| Total Cash | 0.00% | 0.00% | ||||

| Portfolio | 0.26% | 100.00% | 100.00% | |||

BMO Global Asset Management, as of March 31, 2026. Model portfolio for illustrative purposes only. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. These are not recommendations to buy or sell any particular security. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

Lessons from Tuchman

Upon reflecting on the current state of markets, we’re reminded of the lessons from Barbara Tuchman’s The Guns of August, which illustrates how hubris and rigid systems can override rational decision-making. While we are not drawing direct parallels to the current situation in the Middle East, the book offers important lessons for investors as they navigate portfolio construction in the months ahead.

As an example, periods of higher inflation generally increase the co-movement between U.S. stocks and interest rates, requiring a more pragmatic approach to diversification. This often leads to greater interest in real assets like gold, as we’ve seen in recent years. But what happens when even gold fails to provide adequate diversification during a geopolitical shock? Tuchman’s work reminds us of the importance of stress-testing assumptions before a crisis unfolds. When correlation1 structures break down and traditional hedges falter, investors who have considered tail risks in advance are better positioned.

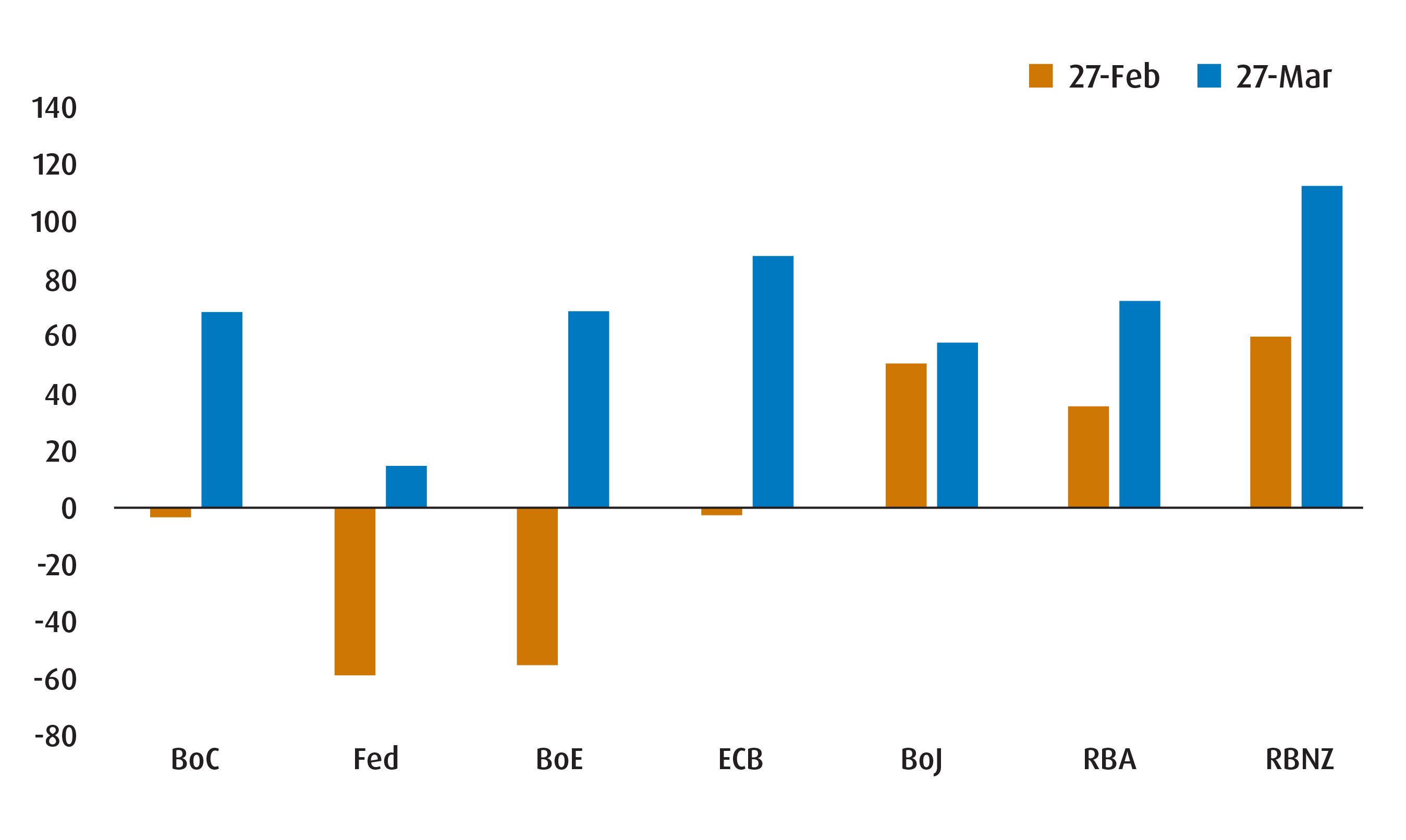

With that in mind, let’s consider the present environment. Even if the Middle East conflict is resolved quickly, the economic and market consequences will likely persist. Inflation risks are no longer symmetrically distributed, and price pressures appear likely to rise. Damage to energy-related infrastructure points to a prolonged period of crude oil and LNG supply disruption, pushing prices higher for longer. This affects refined products (such as gasoline, jet fuel, and kerosene), fertilizer production, and the supply of helium — complicating central bank messaging. Markets have responded by pricing out expected Federal Reserve rate cuts and pricing in aggressive hikes for other developed-market central banks (Chart 1).

Chart 1 – Markets Have Priced in Tighter Central Bank Policy by End-2026.

At the same time, growth risks are shifting in the opposite direction. Higher input costs act as a tax on consumers and weigh on corporate margins. The speed at which rising energy prices feed into slower growth depends largely on a country’s economic slack, which explains why some central banks have recently acknowledged growth risks more explicitly than they did in early 2022.

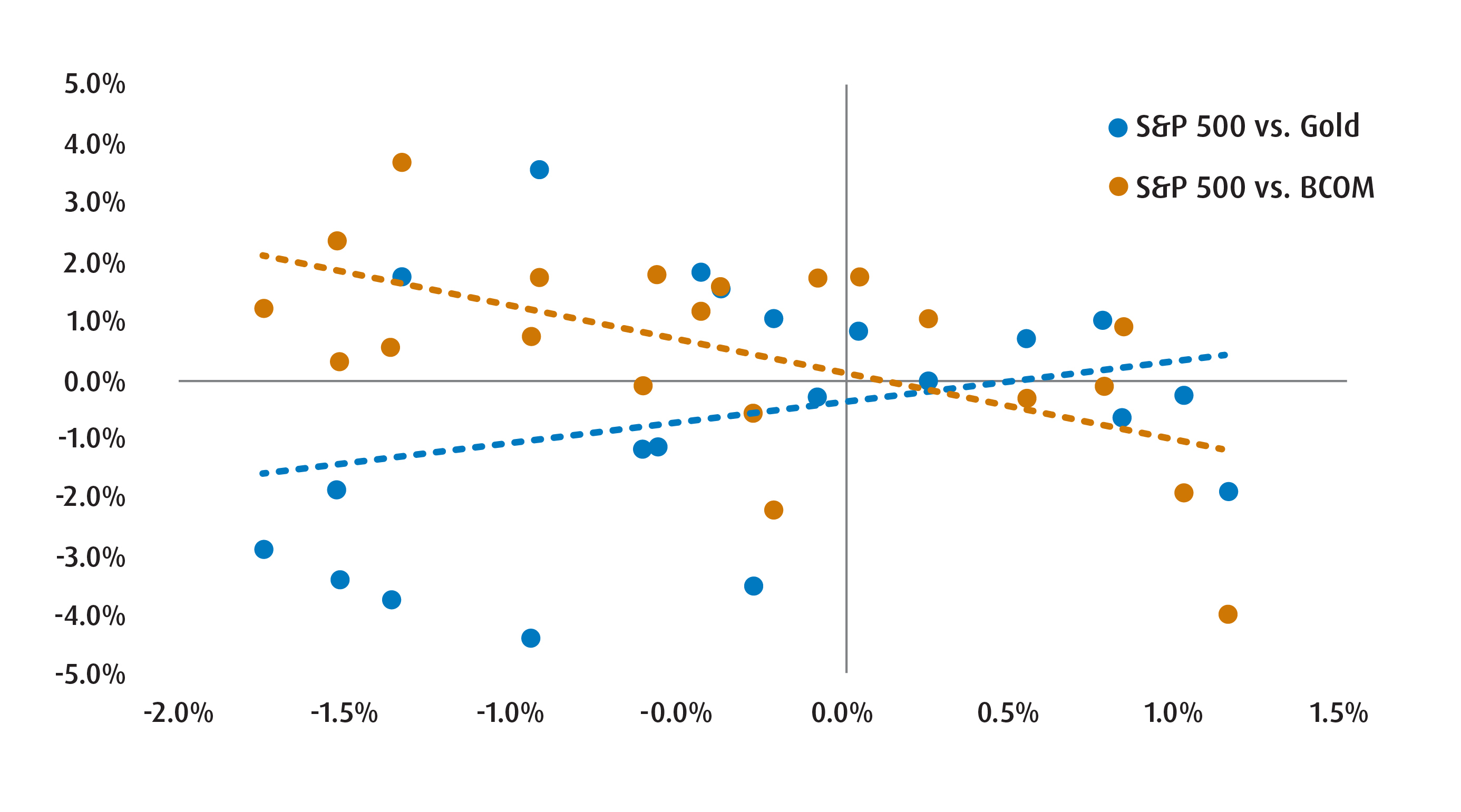

Indeed, our own proprietary macro regime model is signaling that we are transitioning from a ‘reflation’ backdrop to a more stagflation-like regime (Chart 2). This emerging stagflation regime need not mirror the 1970s, but we are still positioning our portfolios to be more robust and resilient. We’re broadening our commodity exposure to provide a more direct hedge against supply shocks. In an environment where inflation surprises are more likely to be positive, this type of convexity is valuable.

We are also allocating to front-end Treasury Inflation-Protected Securities (TIPS) as a hedge against inflation pressures. While breakevens have moderated with recent disinflation progress, they do not fully reflect a sustained energy shock. TIPS offer a cleaner way to express inflation risk without requiring a strong view on nominal growth.

Within equities, we are tilting toward quality and low volatility. If growth slows while cost pressures persist, companies with strong balance sheets, durable margins, and stable cash flows should outperform more cyclical or highly leveraged peers. Low-volatility exposures can also help reduce drawdowns during headline-driven market swings.

History teaches us that conflict does not guarantee crisis. But periods of stress often reveal underlying fragilities. Our role as stewards of capital is not to forecast every geopolitical development, but to recognize that the distribution of macro outcomes is tilting toward a stagflation-like environment — and to position portfolios accordingly.

Chart 2 – Broad Commodity Exposure Is Now a Better Diversification Strategy than Just Relying on Metals

Portfolio Changes

Table 2 – Changes to the Macro Regime Portfolio (from Q1 to Q2 2026)

Sell/Trim | Ticker | Old Weight | (%) | New weight |

| BMO US Aggregate Bond Index ETF (Hedged) | ZUAG.F | 6.15% | -6.15% | 0.00% |

| BMO Canadian Bank Income Index ETF | ZBI | 10.00% | -3.00% | 7.00% |

| BMO MSCI USA High Quality Index ETF | ZUQ | 25.00% | -2.00% | 23.00% |

| BMO MSCI EAFE Index ETF | ZEA | 10.00% | -1.00% | 9.00% |

| BMO MSCI Emerging Markets Index ETF | ZEM | 6.00% | -1.00% | 5.00% |

| BMO Equal Weight Global Base Metals (Hedged) | ZMT | 3.00% | -3.00% | 0.00% |

| BMO Covered Call Spread Gold Bullion ETF | ZWGD | 10.00% | -6.00% | 4.00% |

| BMO Long Short Canadian Equity ETF | ZLSC | 4.00% | -4.00% | 0.00% |

Buy/Add | Ticker | Old Weight | (%) | New weight |

| BMO Discount Bond Index ETF | ZDB | 6.15% | 1.85% | 8.00% |

| BMO US Aggregate Bond Index ETF | ZUAG | 0.00% | 5.00% | 5.00% |

| BMO Short-Term US TIPS Index | ZTIP | 0.00% | 5.00% | 5.00% |

| BMO S&P/TSX Capped Composite Index ETF | ZCN | 18.00% | 2.00% | 20.00% |

| BMO Low Volatility US Equity ETF | ZLU | 0.00% | 4.00% | 4.00% |

| BMO Global Infrastructure Fund ETF | ZGIF | 2.00% | 2.00% | 4.00% |

| BMO Broad Commodity ETF | ZCOM | 0.00% | 6.00% | 6.00% |

BMO Global Asset Management, as of March 31, 2026. Model portfolio for illustrative purposes only. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. These are not recommendations to buy or sell any particular security. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

Table 3 – Asset allocation splits relative to benchmark

Current weight | Benchmark | ||

Fixed income | 25% | 30% |

Underweight |

| 10% | 15% | |

| 15% | 15% | |

Equities | 61% | 60% |

Neutral/overweight |

| 27% | 25% | |

| 20% | 25% | |

| 14% | 10% | |

Alts/hybrids | 14% | 10% |

Overweight |

Source: BMO Global Asset Management, as of March 31, 2026.

Asset Allocation

- Relative to the Q1 edition, we’re making some modest changes to our asset allocation splits. The most notable shifts are that we are paring our positions in the equity and alternative sleeves and reallocating them towards fixed income. Of course, these aren’t big changes – as we still remain underweight fixed income and overweight both equities (slightly) and alts.

- Our macro regime model suggests that we are in the midst of a transition from reflation to stagflation - characterized by low growth and high inflation. This is still consistent with the late cycle feel of the macroeconomic backdrop.

- Despite the challenging backdrop, the underlying fundamentals remain sound enough to maintain a neutral/slightly overweight broad equity position for now. Ahead of the conflict, we did see earnings growth across several sectors in the U.S. and Canada. At the same time, the situation in the Middle East remains fluid, which requires us to be nimbler and more flexible.

- In the fixed income sleeve, the increase in weight reflects our view that the Canadian dollar (CAD) curve provides better value and that we feel U.S. TIPS should outperform in the months ahead. For the alts sleeve, the reduction in weight reflects our shift away from gold and towards a broader set of diversifiers in the commodity and infrastructure spaces.

- Importantly, we are bullish U.S. dollar (USD)/CAD for the coming months. This means that our preference is to keep our US exposure unhedged on a tactical basis. The main reasons for this view are the following: We expect the CAD swaps market to price out rate hikes for the Bank of Canada in 2026; We expect USD upside as net long positioning remains relatively light.

Equities

- We are increasing our allocation to ZCN (BMO S&P/TSX Capped Composite Index ETF) as Canada remains well positioned as a commodity and energy producer. With energy prices supported by ongoing geopolitical uncertainty, the Canadian equity market should continue to benefit, though outcomes will remain sensitive to the duration of the conflict in the Middle East.

- For our U.S. position, we are adding ZLU (BMO Low Volatility US Equity ETF) to complement our existing exposure through ZUQ (BMO MSCI USA High Quality Index ETF). This combination reflects a preference for defensive characteristics and earnings resilience during a period whereby investors remain selective on valuation and fundamentals.

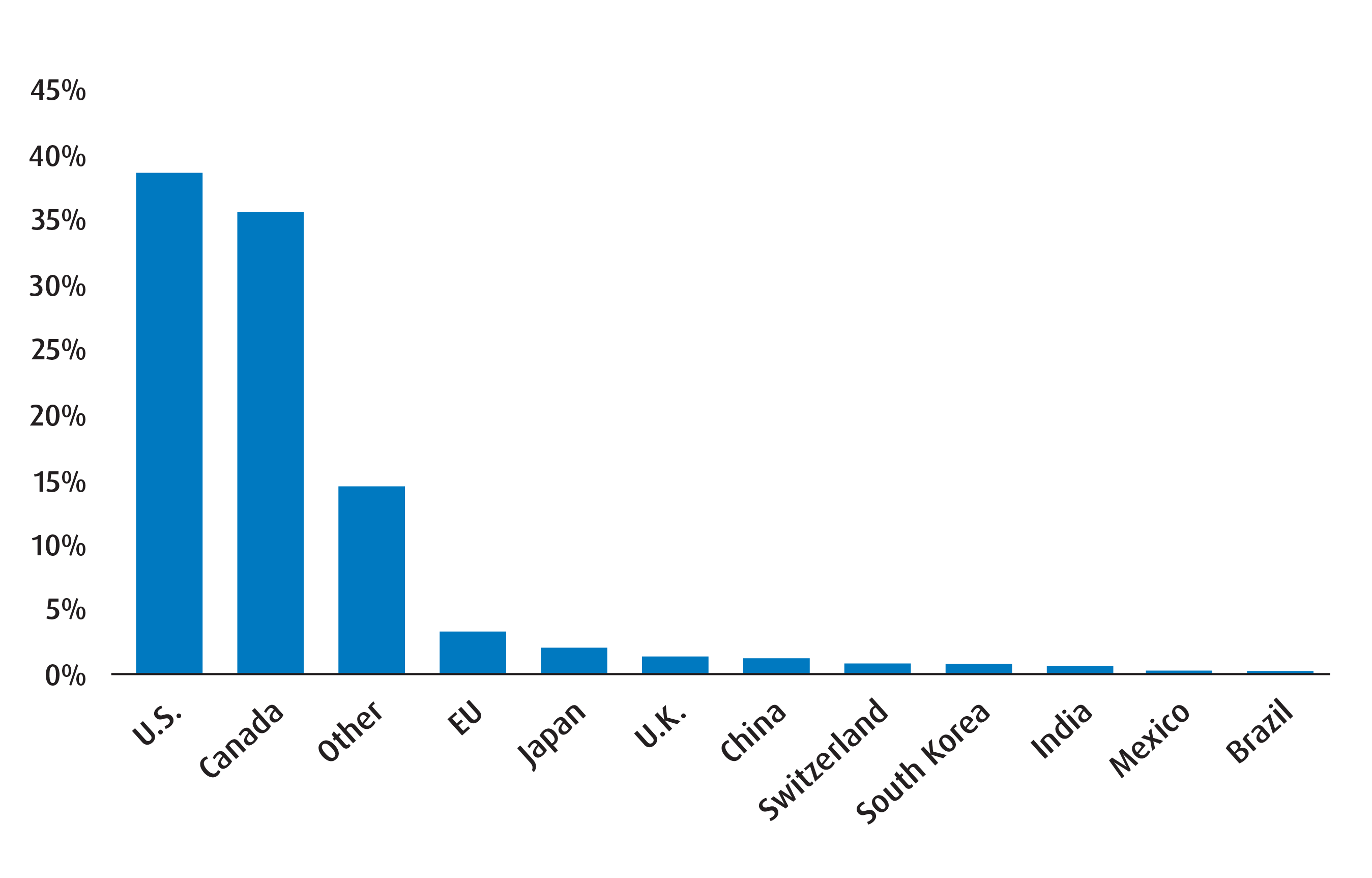

Chart 3 – Q2 2026 Regional Exposure

Fixed Income

- We’ve swapped out ZUAG.F (BMO US Aggregate Bond Index ETF – Hedged Units) and added ZUAG (BMO US Aggregate Bond Index ETF) to reintroduce USD exposure in the FI sleeve. Our view on the USD is the main reason for this change.

- We’ve also added ZTIP (BMO Short‑Term US TIPS Index ETF) as a tactical position as we expect inflation risks to stay firm given energy and broader commodity pressures.

Alts/Hybrids

- The most notable change we’ve made in Alts/Hybrids is adding a tactical allocation to ZCOM (BMO Broad Commodity ETF) to broaden our inflation and geopolitical hedge. Energy has led performance on a year‑to‑date basis, but a persistent risk premium can support a wider set of commodities, which improves diversification if equity volatility picks up.

- We’ve also upgraded the weight for ZGIF (BMO Global Infrastructure Fund ETF) as we continue to constructive on infrastructure, including electric grids, and engineering/construction projects.

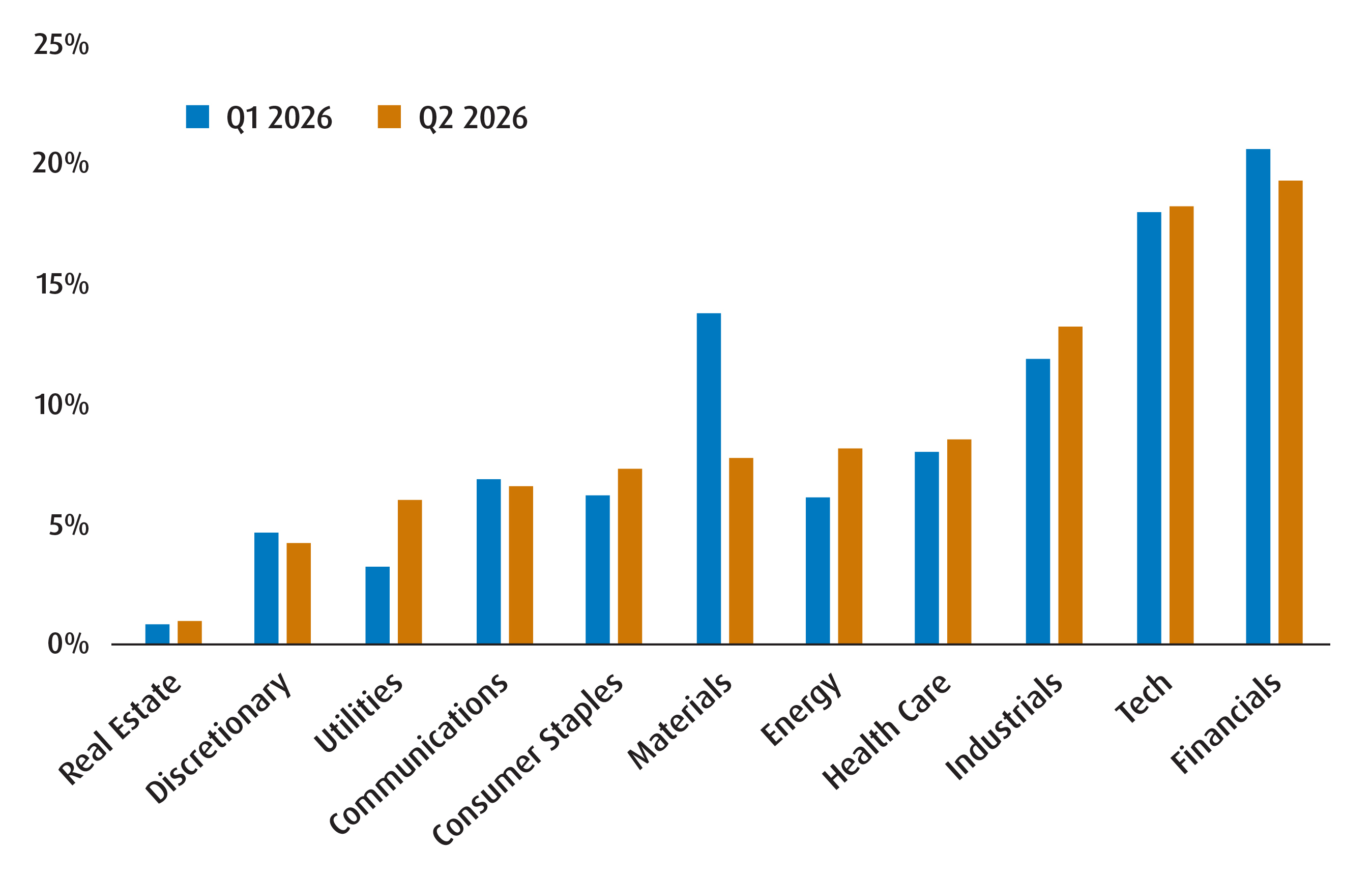

Chart 4 – Global Equity Sector Breakdown

Table 4 – Fixed Income Breakdown

Q2 2026 |

Q1 2026 |

|

Weighted Average Term |

5.11 |

3.43 |

Weighted Average Duration |

4.41 |

2.76 |

Weighted Average Coupon (%) |

2.49 |

2.77 |

Annualized Dist. Yield (%) |

3.02 |

2.66 |

Weighted Average Yield to Maturity (%) |

3.98 |

2.59 |

Source: BMO Global Asset Management, as of April 1, 2026.

Performance Data

Table 5 – Standard Performance Data of Holdings

Fund Name |

Ticker |

Year-to-Date |

1-month |

3-month |

6-month |

1-Year |

3-Year |

5-Year |

10-Year |

Since Inception |

Inception Date |

8.62% |

7.71% |

10.03% |

21.59% |

38.66% |

22.79% |

17.02% |

13.64% |

10.06% |

2009-05-29 |

||

9.35% |

4.92% |

10.25% |

16.40% |

25.61% |

18.50% |

12.08% |

10.27% |

9.07% |

2014-02-10 |

||

13.85% |

5.56% |

14.36% |

26.87% |

41.82% |

20.62% |

7.20% |

10.42% |

6.70% |

2009-10-20 |

||

11.14% |

7.41% |

7.58% |

12.95% |

10.42% |

12.59% |

13.40% |

10.45% |

13.95% |

2013-03-19 |

||

1.56% |

1.51% |

1.15% |

3.06% |

4.35% |

3.64% |

— |

— |

2.68% |

2023-01-23 |

||

2.14% |

1.61% |

0.75% |

3.52% |

2.10% |

4.72% |

0.61% |

1.89% |

2.42% |

2014-02-10 |

||

— |

— |

— |

— |

— |

— |

— |

— |

— |

2025-10-21 |

||

2.21% |

1.26% |

0.59% |

9.80% |

8.94% |

24.36% |

15.88% |

16.29% |

16.36% |

2014-11-05 |

||

1.20% |

0.43% |

1.46% |

3.16% |

5.41% |

7.85% |

— |

— |

4.32% |

2022-02-07 |

||

— |

— |

— |

— |

— |

— |

— |

— |

— |

2025-05-22 |

||

0.29% |

0.56% |

-1.48% |

0.47% |

-1.30% |

5.22% |

4.96% |

— |

5.01% |

2021-01-20 |

||

1.18% |

1.81% |

-0.84% |

3.25% |

0.13% |

4.96% |

— |

— |

4.65% |

2023-01-23 |

||

11.07% |

7.72% |

7.48% |

14.11% |

23.21% |

— |

— |

— |

19.72% |

2023-06-27 |

Source: BMO Global Asset Management. As of March 31, 2026. The portfolio holdings are subject to change without notice and only represent a percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

Disclaimers

For advisor use only.

The portfolio holdings and asset allocations are subject to change without notice and individual holdings only represent a small percentage of portfolio holdings. They are not recommendations to buy or sell any particular security.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

The viewpoints expressed by the author represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results.

This communication is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

Index returns do not reflect transactions costs or the deduction of other fees and expenses and it is not possible to invest directly in an Index. Past performance is not indicative of future results.

The ETFs referred to herein are not sponsored, endorsed, or promoted by MSCI and MSCI bear no liability with respect to an ETF or any index on which such ETF is based. The ETF’s prospectus contains a more detailed description of the limited relationship that MSCI has with the Manager and any related ETF.

The Index is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by the Manager. S&P®, S&P 500®, US 500, The 500, iBoxx®, iTraxx® and CDX® are trademarks of S&P Global, Inc. or its affiliates (“S&P”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”), and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by the Manager. The ETF is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the Index.

The Select Sector SPDR Trust consists of eleven separate investment portfolios (each a “Select Sector SPDR ETF” or an “ETF” and collectively the “Select Sector SPDR ETFs” or the “ETFs”). Each Select Sector SPDR ETF is an “index fund” that invests in a particular sector or group of industries represented by a specified Select Sector Index. The companies included in each Select Sector Index are selected on the basis of general industry classification from a universe of companies defined by the S&P 500®. The investment objective of each ETF is to provide investment results that, before expenses, correspond generally to the price and yield performance of publicly traded equity securities of companies in a particular sector or group of industries, as represented by a specified market sector index.

The S&P 500, SPDRs, and Select Sector SPDRs are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use. The stocks included in each Select Sector Index were selected by the compilation agent. Their composition and weighting can be expected to differ to that in any similar indexes that are published by S&P. The S&P 500 Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. The S&P 500 Index figures do not reflect any fees, expenses or taxes. An investor should consider investment objectives, risks, fees and expenses before investing.

You cannot invest directly in an index.

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

Distribution yields are calculated by using the most recent regular distribution, or expected distribution, (which may be based on income, dividends, return of capital, and option premiums, as applicable) and excluding additional year end distributions, and special reinvested distributions annualized for frequency, divided by current net asset value (NAV). The yield calculation does not include reinvested distributions. Distributions are not guaranteed, may fluctuate and are subject to change and/or elimination. Distribution rates may change without notice (up or down) depending on market conditions and NAV fluctuations. The payment of distributions should not be confused with the BMO ETF’s performance, rate of return or yield. If distributions paid by a BMO ETF are greater than the performance of the investment fund, your original investment will shrink. Distributions paid as a result of capital gains realized by a BMO ETF, and income and dividends earned by a BMO ETF, are taxable in your hands in the year they are paid. Your adjusted cost base will be reduced by the amount of any returns of capital. If your adjusted cost base goes below zero, you will have to pay capital gains tax on the amount below zero.

Cash distributions, if any, on units of a BMO ETF (other than accumulating units or units subject to a distribution reinvestment plan) are expected to be paid primarily out of dividends or distributions, and other income or gains, received by the BMO ETF less the expenses of the BMO ETF, but may also consist of non-taxable amounts including returns of capital, which may be paid in the manager’s sole discretion. To the extent that the expenses of a BMO ETF exceed the income generated by such BMO ETF in any given month, quarter, or year, as the case may be, it is not expected that a monthly, quarterly, or annual distribution will be paid. Distributions, if any, in respect of the accumulating units of BMO Short Corporate Bond Index ETF, BMO Short Federal Bond Index ETF, BMO Short Provincial Bond Index ETF, BMO Ultra Short-Term Bond ETF and BMO Ultra Short-Term US Bond ETF will be automatically reinvested in additional accumulating units of the applicable BMO ETF. Following each distribution, the number of accumulating units of the applicable BMO ETF will be immediately consolidated so that the number of outstanding accumulating units of the applicable BMO ETF will be the same as the number of outstanding accumulating units before the distribution. Non-resident unitholders may have the number of securities reduced due to withholding tax. Certain BMO ETFs have adopted a distribution reinvestment plan, which provides that a unitholder may elect to automatically reinvest all cash distributions paid on units held by that unitholder in additional units of the applicable BMO ETF in accordance with the terms of the distribution reinvestment plan. For further information, see the distribution policy in the BMO ETFs’ prospectus.

BMO ETFs are managed and administered by BMO Asset Management Inc., an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.